Is Fast Retailing (TSE:9983) Overvalued? A Fresh Look at Its Valuation After Recent Share Price Shifts

Fast Retailing (TSE:9983) might not have made headlines with any major event today, but the recent movements in its share price are certainly giving investors reason to pause. Whether you are a long-term holder or just starting to track the stock, shifts like this tend to spark questions. Is there something happening under the surface that the market is beginning to recognize?

Looking over the past year, Fast Retailing’s shares have moved higher by 12%, even as this year has seen a 6% dip. Short-term trading has been mixed, with a slight uptick of 4% in the past month. The company continues to post steady sales and income growth, but recent performance suggests momentum may be more cautious compared to previous booming stretches.

After this period of volatility, some investors may wonder whether the current price represents an opportunity for Fast Retailing or if the market is already accounting for future growth in the share price.

Price-to-Earnings of 37.3x: Is it justified?

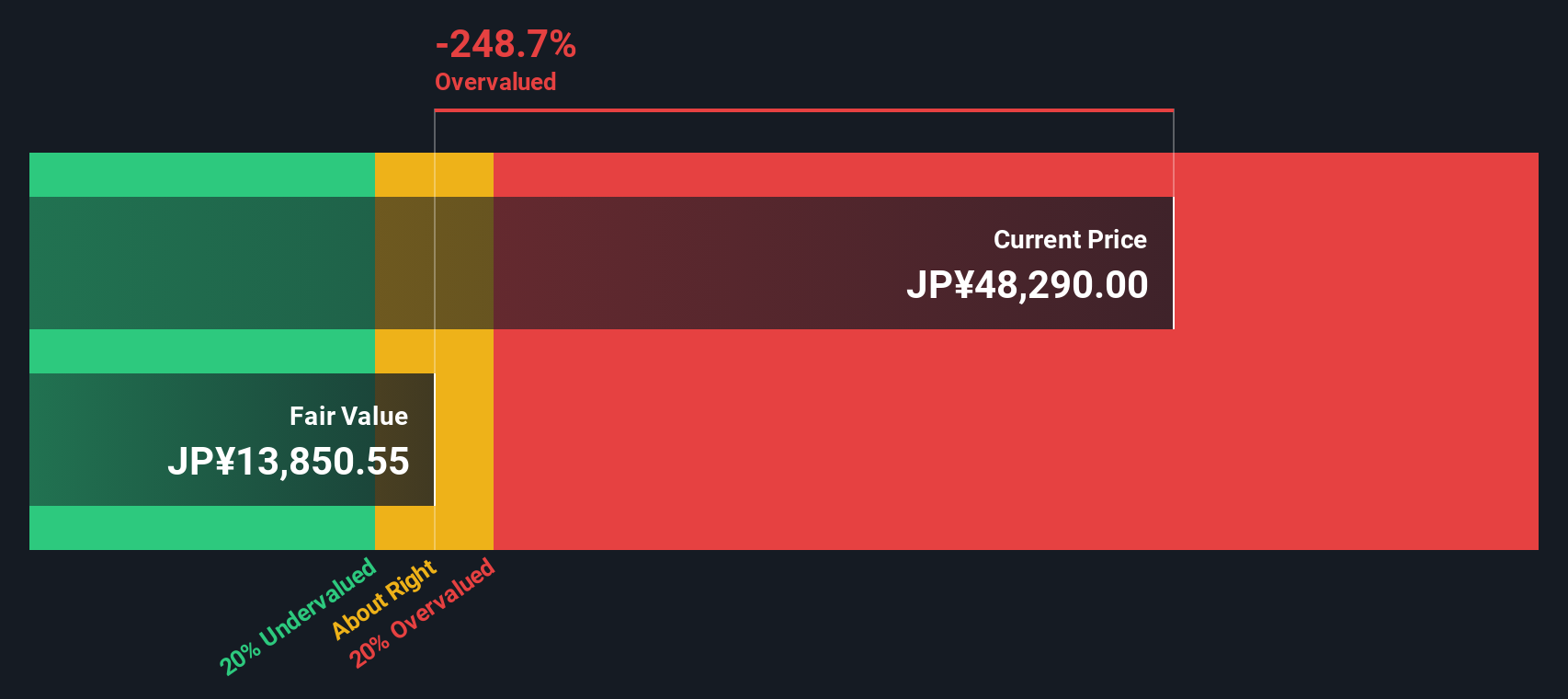

Based on its current price-to-earnings (P/E) ratio of 37.3x, Fast Retailing appears to be trading at a premium relative to both the Japanese specialty retail industry average of 14.5x and the average of its peer group at 25.6x.

The P/E ratio compares a company's share price to its earnings per share. For a retailer like Fast Retailing, this multiple reflects how much investors are willing to pay for each unit of recent profits. A P/E ratio well above industry and peer averages usually suggests that the market is pricing in strong future earnings growth or sees the company as having superior business quality or defensibility.

Given this premium valuation, the implication is clear: the market is demanding more from Fast Retailing than from its sector peers. Whether this expectation is justified depends on the company's future growth and ability to continue outperforming the competition.

Result: Fair Value of ¥14,655.14 (OVERVALUED)

See our latest analysis for Fast Retailing.However, slower annual revenue and income growth rates, combined with recent price volatility, could challenge the market's expectations for sustained premium performance.

Find out about the key risks to this Fast Retailing narrative.Another View: What Does the DCF Model Say?

Taking a step back from ratios and market comparisons, our DCF model offers a value grounded in future cash flows. This approach also finds Fast Retailing overvalued. Could these methods be pointing to the same risk?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Fast Retailing Narrative

If you have a different perspective or want to dig deeper into the numbers yourself, assembling your own Fast Retailing story is quick and straightforward. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Fast Retailing.

Looking for more investment ideas?

Don’t let opportunity pass you by. There are stocks rewriting the playbook in every corner of the market. Use the Simply Wall Street Screener to spot the next big stories before everyone else:

- Unearth undervalued gems based on future cash flows by checking out undervalued stocks based on cash flows.

- Tap into the AI-driven future with companies at the forefront of innovation through AI penny stocks.

- Capture income potential with top picks boasting reliable payouts using dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com