- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalWhat ResMed (RMD)'s VirtuOx Acquisition and Q4 Growth Reveal About Its Evolving Strategy

- ResMed Inc. recently presented at the World Sleep Congress in Singapore and has reported fourth quarter fiscal 2025 growth, driven by strong performance in its Mask business and a rebound in Device sales.

- The company's acquisition of VirtuOx in May, a leading diagnostic testing facility, highlights ResMed's efforts to strengthen its position across the sleep, respiratory, and cardiac care continuum.

- We'll explore how the acquisition of VirtuOx could influence ResMed's investment narrative and long-term growth prospects.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

ResMed Investment Narrative Recap

To be a ResMed shareholder, you need to believe in the company’s ability to expand its leadership across sleep health, capitalize on long-term demand for treatment, and sustain technological and diagnostic innovation. The recent World Sleep Congress presentation and Q4 2025 results reaffirm management’s progress with product growth, but the most important short-term catalyst, device sales momentum, remains exposed to ongoing competitive pressures, which the latest news does not materially change as a risk.

ResMed’s acquisition of VirtuOx in May stands out as a directly relevant move, strengthening its diagnostics capabilities and supporting its ambition to capture a larger share of the diagnosis-to-therapy funnel. Improved access to at-home testing and digital screening with VirtuOx aligns with efforts to boost patient flow, but near-term execution risks tied to integration and competitive response will be important to watch. Despite solid product and earnings growth, investors should not overlook the threat posed by new therapies such as GLP-1 drugs that could reduce device demand if adoption accelerates...

Read the full narrative on ResMed (it's free!)

ResMed's outlook forecasts $6.4 billion in revenue and $1.9 billion in earnings by 2028. This is based on an expected annual revenue growth rate of 7.8% and an earnings increase of $0.5 billion from current earnings of $1.4 billion.

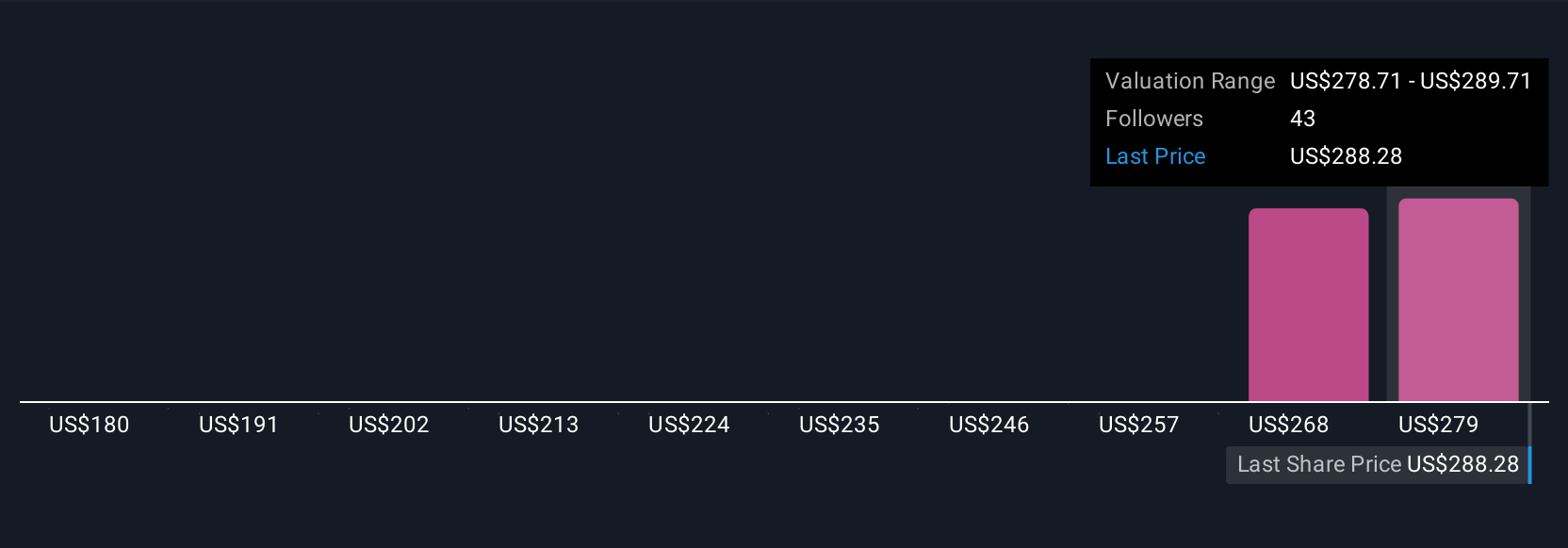

Uncover how ResMed's forecasts yield a $291.86 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Eight fair value estimates from the Simply Wall St Community span US$179.72 to US$291.86 per share, reflecting highly varied outlooks. Amid this range, many highlight the competitive threat from new device alternatives as a key factor that could reshape ResMed’s growth and margins, explore these differing perspectives for a fuller picture.

Explore 8 other fair value estimates on ResMed - why the stock might be worth 35% less than the current price!

Build Your Own ResMed Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ResMed research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free ResMed research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ResMed's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com