Should Axon Enterprise’s (AXON) Record Backlog and AI Bundle Adoption Prompt a Closer Look by Investors?

- In the past week, Axon Enterprise reported a strong Q2 2025, highlighting a record backlog of US$10.7 billion and a raised full-year revenue outlook as its public safety SaaS platform gains traction.

- A key insight is that agencies are accelerating adoption of Axon's premium, AI-powered Officer Safety Plan bundles, significantly increasing monetization per user and supporting multi-year revenue visibility.

- We'll explore how rising adoption of AI-enhanced bundles and a record backlog influence Axon's future growth outlook and investment narrative.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Axon Enterprise Investment Narrative Recap

To be a shareholder in Axon Enterprise, you have to believe in the company’s ongoing transition from hardware provider to a leading public safety SaaS platform with durable, recurring revenues. The recent news of a record US$10.7 billion backlog and stronger revenue guidance offers more confidence in multi-year growth, adding weight to the current catalyst: accelerating adoption of AI-powered bundles, while the biggest risk, government budget volatility, remains unchanged following this update.

The company’s recent announcement of higher 2025 revenue guidance (now US$2.65 billion to US$2.73 billion) aligns with surging demand for premium SaaS solutions, directly supporting Axon’s upsell strategy and providing a short-term lift to investor optimism around recurring revenue streams. This strengthens faith in Axon’s ability to increase revenue per user despite competitive and regulatory pressures that could impact future growth.

By contrast, investors should pay close attention to the ongoing risk that public sector funding cycles and political shifts could suddenly put...

Read the full narrative on Axon Enterprise (it's free!)

Axon Enterprise's outlook anticipates $4.5 billion in revenue and $555.1 million in earnings by 2028. This is based on a projected annual revenue growth rate of 23.7% and a $228.8 million increase in earnings from the current $326.3 million.

Uncover how Axon Enterprise's forecasts yield a $868.94 fair value, a 11% upside to its current price.

Exploring Other Perspectives

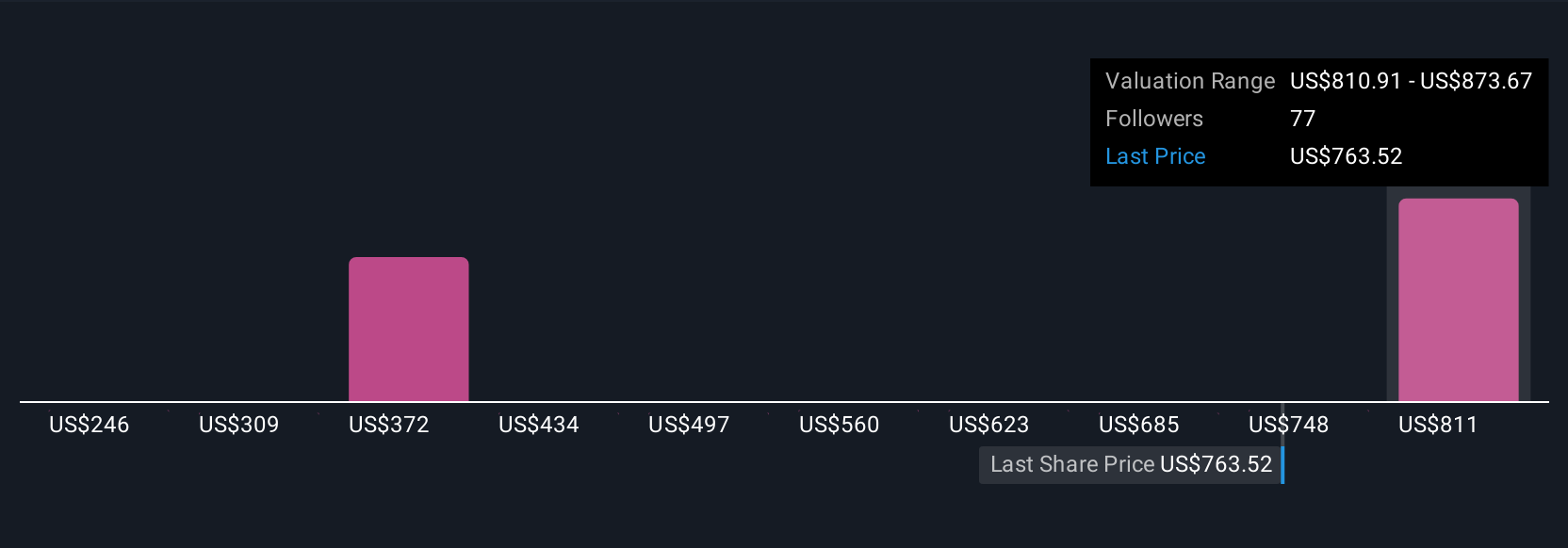

Seven fair value estimates from the Simply Wall St Community range widely, from US$246 to US$869 per share, spotlighting sharply contrasting investor opinions. With agencies rapidly adopting AI-powered bundles, it is worth seeing how these diverse perspectives weigh on Axon’s potential for sustained recurring revenue and long-term growth.

Explore 7 other fair value estimates on Axon Enterprise - why the stock might be worth less than half the current price!

Build Your Own Axon Enterprise Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Axon Enterprise research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Axon Enterprise research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Axon Enterprise's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com