Assessing AbbVie's Valuation After Rinvoq’s Positive Phase 3 Results in Severe Alopecia Areata

AbbVie (ABBV) has just announced positive topline results from the second pivotal Phase 3 study for upadacitinib, its immunology drug marketed as Rinvoq, in treating severe alopecia areata. Both the 15 mg and 30 mg doses achieved the primary endpoint, with patients seeing meaningful scalp hair regrowth compared to placebo. As the company works to reinforce its immunology portfolio while older drugs face competitive threats, this kind of data can attract investors’ attention and prompt a closer look at AbbVie’s next growth chapter.

Excitement from this clinical win follows a series of headline-grabbing moves by AbbVie, including broad pipeline expansion, strategic acquisitions, and a sizable manufacturing investment in Illinois. Over the past quarter, AbbVie’s shares have risen 13%, outpacing many peers and reflecting strong confidence in its new product launches and the company’s ability to pivot beyond aging blockbusters. For the full year, the stock is up 10%, and its momentum appears to be building as investors weigh these gains against the company’s history of steady performance and a notable 5-year return of 169%.

After this quarter’s rally and the latest breakthrough for Rinvoq, some may be considering whether AbbVie is trading at a discount that still leaves room for upside, or if the market has already captured the value of its future growth.

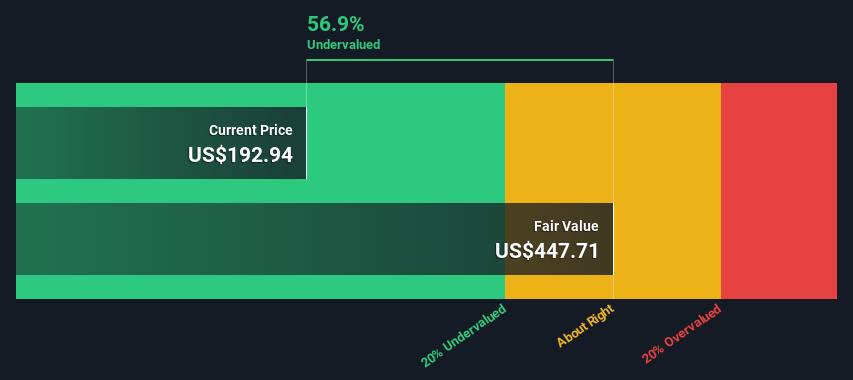

Most Popular Narrative: 1.9% Undervalued

According to community narrative, AbbVie is currently seen as trading just below its fair value, based on future earnings expectations, margin expansion, and a moderate analyst consensus price target. Opinions cluster around long-term growth potential driven by innovation and expanding indications for key therapies.

"AbbVie's diversified and expanding late-stage and early-stage pipeline, coupled with consistent business development activity (for example, Capstan in vivo CAR-T, Gubra amylin analog for obesity, next-generation siRNA platforms), positions the company to capitalize on the increasing adoption of biologics and specialty pharmaceuticals. This can reinforce premium pricing and protect net margins."

Curious how AbbVie’s future product launches fuel this bullish valuation? The real story is hidden in aggressive margin improvements, ambitious growth bets, and an analyst framework that banks on major earnings expansion. Want to know what makes analysts this confident? The numbers behind this valuation just might surprise you.

Result: Fair Value of $214.77 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, ongoing pricing pressure and over-reliance on key drugs mean that unforeseen regulatory changes or competitive threats could quickly shift AbbVie's outlook.

Find out about the key risks to this AbbVie narrative.Another View: DCF Model Offers a Dramatically Different Take

Looking beyond market-based multiples, the SWS DCF model shows a sharply different story for AbbVie. This approach suggests the stock could be much more undervalued than traditional measures imply. The question remains: which view truly reflects the opportunity?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own AbbVie Narrative

If you have a different perspective or prefer to dive deeper on your own, you can build a personalized view in just a few minutes. do it your way.

A great starting point for your AbbVie research is our analysis highlighting 2 key rewards and 6 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Why stop with just one opportunity? Expand your outlook and explore new possibilities by finding stocks that fit your investment style using our hand-picked screeners. You may find standout companies in areas you have not considered, and by acting now, you can stay ahead of the curve.

- Capture reliable income by targeting dividend stocks with yields > 3% that consistently pay strong yields above 3%.

- Benefit from the growth of AI by exploring AI penny stocks that are transforming industries with advanced technology.

- Strengthen your portfolio with healthcare AI stocks which are shaping the future of medical innovation and patient care.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com