UnitedHealth Group (UNH) Valuation in Focus as Buffett Takes Stake and Amedisys Deal Expands Growth Potential

UnitedHealth Group (UNH) is back in the spotlight after Warren Buffett’s Berkshire Hathaway revealed it now holds a sizable position in the health insurance giant. Investors tend to pay close attention whenever Buffett becomes involved, and this situation is no different, especially as UnitedHealth adds the recent Amedisys acquisition to its portfolio. Both moves appear to have boosted confidence in the company’s growth story, even though there have been some bumps along the way with analysts adjusting their earnings forecasts downward.

Taking a broader view, the share price has not shown a dramatic shift upward, hovering near $307 at last close. Over the past month, the stock gained around 9%, recovering some earlier weakness, but remains significantly down for the year. Dividend affirmations and ongoing buybacks highlight management’s efforts to reassure investors. However, the overall trend has been sideways to negative, with three- and five-year returns now lagging the wider market.

The question now is whether the market has fully digested the impact of these new developments, or if UnitedHealth Group is quietly trading at a discount to its true value while growth potential builds beneath the surface.

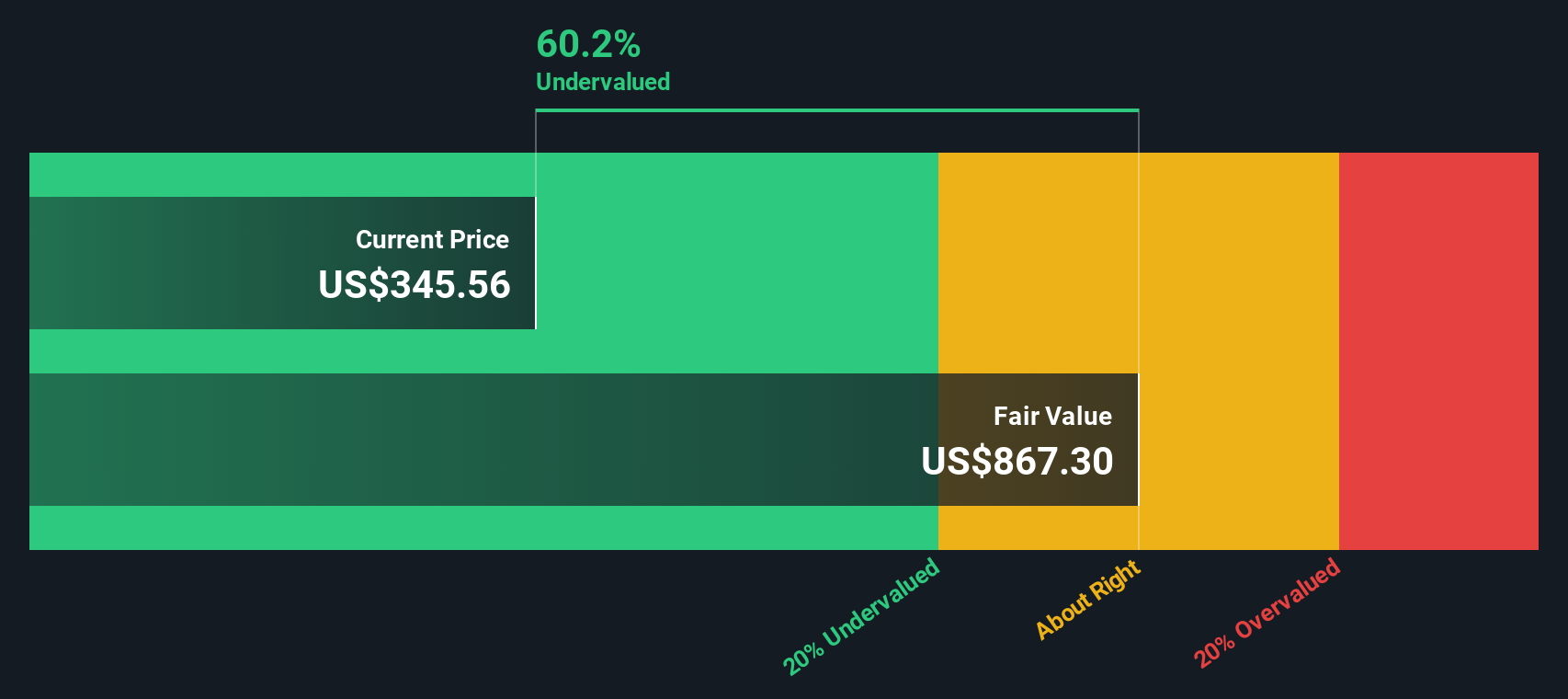

Most Popular Narrative: 6.1% Undervalued

According to the community narrative, UnitedHealth Group is currently trading at a discount to its analyst-determined fair value. This is based on projections that consider forward-looking earnings potential, margins, and sector-related risk factors.

"The company is addressing unanticipated changes in Medicare membership profiles which impacted 2025 revenue. They are taking measures to ensure complex patients engage in clinical and value-based programs, which should help stabilize and potentially increase future revenue."

Ever wondered what market-moving assumptions are fueling this fair value estimate? The key factors include future earnings, margin compression, and a profit multiple typically seen in stronger sectors. The full story behind these analyst expectations, and the consensus that informed this calculation, is only a click away.

Result: Fair Value of $327.29 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, ongoing challenges in Medicare strategies or missteps in adapting to new regulatory models could quickly undermine the current outlook for UnitedHealth Group.

Find out about the key risks to this UnitedHealth Group narrative.Another View: Discounted Cash Flow Model

While analyst price targets suggest UnitedHealth Group is trading below its fair value, our DCF model tells a very similar story. Both methods currently point to undervaluation. However, could upcoming events alter this?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own UnitedHealth Group Narrative

Of course, if you see things differently or want to dig deeper into the numbers yourself, it only takes a few minutes to develop your own assessment. do it your way.

A great starting point for your UnitedHealth Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never settle for just one opportunity. Shake up your portfolio and stay ahead of the pack by tapping into powerful stock ideas you might be missing. Make your next move count with these handpicked investment angles that could help you capture fresh market wins:

- Unlock higher passive income by targeting dividend stocks with yields > 3% that offer consistent yields above 3%, positioning your portfolio to benefit from robust dividends.

- Gain a tech edge by analyzing AI penny stocks involved in AI-driven breakthroughs and shaping tomorrow’s industries.

- Explore healthcare innovation with healthcare AI stocks to uncover companies leading the next wave of medical advancements with artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com