Does IREN’s 135% Rally Signal More Upside After Recent Bitcoin Rebound?

Are you eyeing IREN stock and wondering whether now is the right moment to make your move? You are definitely not alone. After a stunning 135% rise over the past three months, with a year-to-date return north of 100%, IREN has landed squarely on the watchlists of both growth seekers and cautious optimists. That kind of momentum, especially following months of volatility across tech and crypto-adjacent sectors, sends a clear message that the market is reconsidering IREN’s risk and reward proposition.

So, what is really going on here? Much of IREN’s recent price surge seems tied to broader renewals of interest in Bitcoin mining stocks, plus solid revenue and net income growth rates that cannot be ignored. With last week’s 9% price uptick and analysts’ targets pointing about 3.5% higher from here, there is optimism, but also lots of eyes on whether this party can keep going, or if it is just another fleeting moment.

Valuation, of course, becomes center stage when a stock runs this far, this fast. IREN currently earns a value score of 3 out of 6, meaning the company looks undervalued on half the common checks analysts use—solid, but not spectacular. Over the next sections, we will break down what these valuation checks really indicate, and how each one might sharpen your decision process. And if you are looking for a more insightful way to think about IREN’s true worth, stick around for the conclusion, as you will not want to miss it.

IREN delivered 148.6% returns over the last year. See how this stacks up to the rest of the Software industry.Approach 1: IREN Cash Flows

Discounted Cash Flow (DCF) models estimate what a company is really worth by projecting its future cash flows and then adjusting those back to today’s value, factoring in the time value of money. For investors, this method helps cut through market hype to reveal underlying value.

IREN’s latest twelve-month Free Cash Flow (FCF) stands at -$1,261.6 million, signaling heavy investment or recent operational challenges. Analysts forecast a steady recovery, with FCF expected to swing positive and reach about $365.7 million by 2035. This recovery trajectory is largely based on projections that show FCF reaching $396 million by 2027 and then leveling off in the years that follow, with minor annual adjustments.

Based on these projections, IREN’s intrinsic value works out to $24.63 per share using a 2 Stage Free Cash Flow to Equity model. Compared to the current market price, this valuation means IREN is 13.0% undervalued according to the DCF calculation.

For investors, that 13.0% undervalued mark suggests there may still be room for upside if IREN can deliver on its FCF turnaround story.

Result: UNDERVALUED

Approach 2: IREN Price vs Sales

For companies like IREN that are still moving toward sustained profitability, the Price-to-Sales (P/S) ratio is often a more insightful valuation tool than earnings-based multiples. The P/S ratio helps investors gauge how much they are paying for every dollar of a company’s revenue, which can be a helpful perspective when profits are irregular or negative.

Growth expectations and overall risk profile play a big role in what counts as a "normal" P/S ratio. Fast-growing tech firms or those with large addressable markets often command higher P/S ratios, while higher risk or slower growth tends to bring this number down. The key question is whether investors believe today's sales can turn into substantial future profits.

Currently, IREN trades at a P/S ratio of 13.7x. This is well ahead of the Software industry average of 5.2x, but below the peer group’s average of 19.0x. Notably, Simply Wall St calculates a “Fair Ratio” for IREN of 45.3x, which reflects its specific combination of growth potential, profit margins, market cap, and risks. Since the Fair Ratio is substantially higher than IREN’s actual P/S ratio, the data points to IREN being undervalued based on this metric, even after the stock’s recent strong run.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your IREN Narrative

A Narrative is your own perspective on a company’s story. It is a simple way to combine your beliefs about IREN’s future with the numbers, letting you describe not just what you think will happen but why.

Instead of just relying on rigid metrics, Narratives connect the dots between IREN’s real-world progress, your estimates for future revenue, profits, and margins, and the resulting fair value. This approach can make your investment decision feel more grounded and personal.

On Simply Wall St, Narratives are easy to create and use. You can view how a whole community of investors, each with their own unique assumptions, value the same company. This turns complex financial forecasting into an accessible, interactive tool.

This makes it much simpler to decide whether to buy or sell by directly comparing your Narrative’s Fair Value to the current price. Since Narratives automatically update whenever news or fresh results arrive, you are always making decisions based on the latest picture.

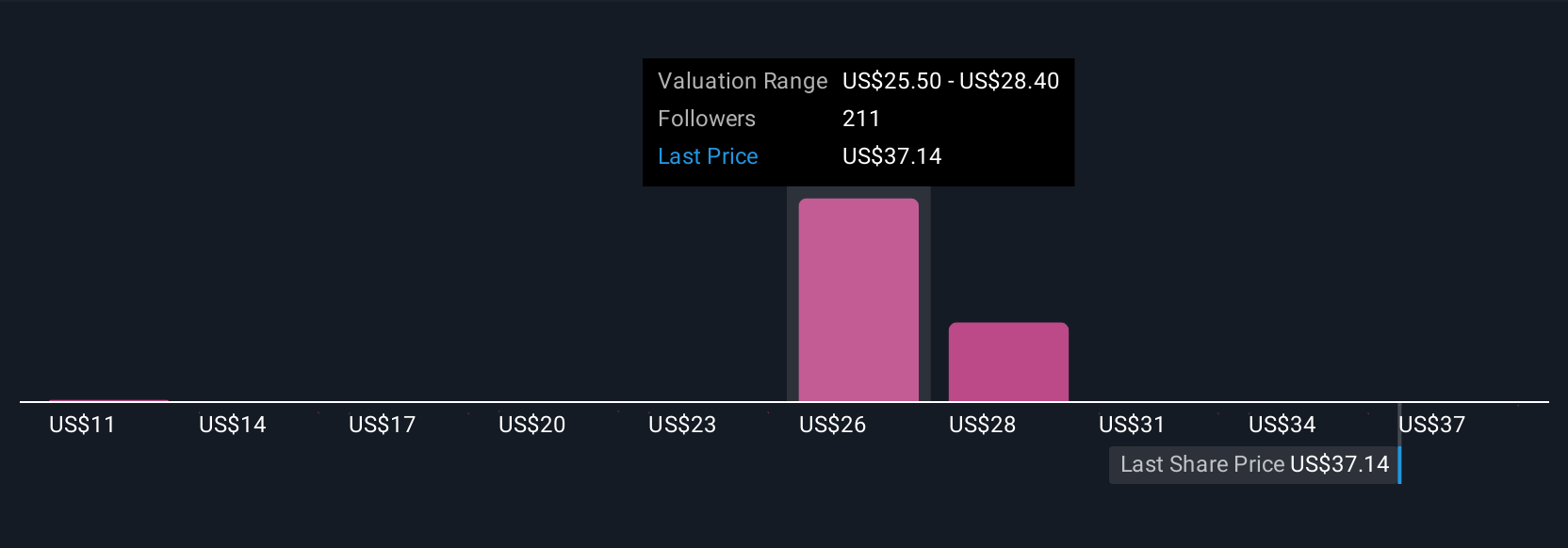

For example, with IREN, one Narrative sees potential for a fair value of $27 per share if future AI infrastructure growth materializes. A more conservative Narrative expects just $11 a share if revenue and margins rise cautiously, demonstrating how your outlook and insights truly shape valuation.

For IREN, however, we'll make it really easy for you with previews of two leading IREN Narratives:

Fair value: $26.54

Current price is 19.2% below this fair value

Projected revenue growth: 30%

- IREN aims to lead sustainable Bitcoin mining using 100% renewable energy, with operations in North America and a focus on energy efficiency and innovative partnerships with power producers.

- The company is diversifying into AI data center services and high-performance computing to add new revenue streams, while maintaining strong financial health and expanding mining capacity.

- Main risks include Bitcoin price volatility, the need for further capital raising (dilution), evolving regulatory landscapes, and competition both in mining and tech infrastructure.

Fair value: $11.00

Current price is 94.8% above this fair value

Projected revenue growth: 35.83%

- Using conservative assumptions, the narrative projects moderate revenue growth (25% annually) and improved but still modest profit margins for IREN over the next five years.

- A higher discount rate is assigned to reflect ongoing business risks, including dependence on Bitcoin prices and risk from continued shareholder dilution.

- Even with some improvements, the analysis finds that IREN’s current share price is likely overvalued compared to intrinsic value calculated with more cautious outlooks and risk adjustments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com