How Should Investors View HCA Healthcare Shares After Recent 15% Surge?

If you are considering what to do with HCA Healthcare stock right now, you are not alone. The stock has sparked plenty of interest lately, and for good reason, as its recent price movements have left investors debating whether to buy, sell, or simply hold tight. Over just the past month, HCA shares have soared by more than 15%, and year-to-date the stock is up a striking 35.8%. This momentum stands out in the healthcare sector. Longer-term gains are also notable, with HCA delivering a total return of 213% over the last five years. These figures highlight not just recent optimism but also an ongoing re-evaluation of the company's growth potential and risk profile as market conditions evolve.

With HCA closing recently at $404.26, which is just a bit above some analyst price targets but still trading at a hefty 50.4% discount to intrinsic value, questions about how undervalued or overvalued the stock might be are more relevant than ever. Looking at a range of standard valuation checks, HCA scores 5 out of 6 for being undervalued. This may be a strong signal for investors who care about getting in at the right price. Of course, each method of valuing a company has its own strengths and weaknesses. In the next section, we will break down these approaches to see how HCA stacks up. And if you want to know about the most insightful way to really understand HCA's value, stay tuned for the ending because it is something you will not want to miss.

HCA Healthcare delivered 6.4% returns over the last year. See how this stacks up to the rest of the Healthcare industry.Approach 1: HCA Healthcare Cash Flows

A Discounted Cash Flow (DCF) model estimates what a company is really worth by projecting its future cash flows and discounting them back to today’s dollars. This approach helps investors gauge whether a stock is trading below or above its intrinsic value.

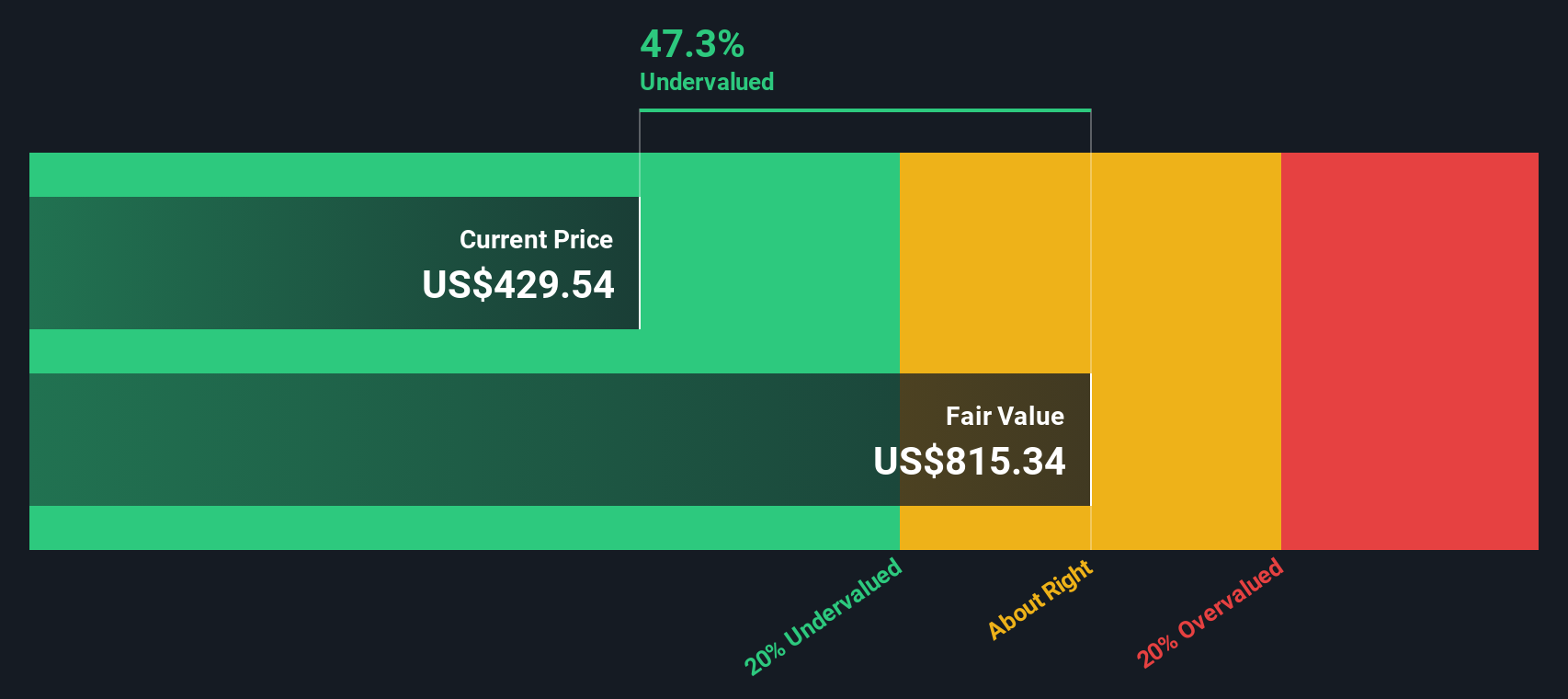

HCA Healthcare generated $6.83 billion in Free Cash Flow over the last twelve months, signaling strong underlying financial performance. Analysts forecast a steady upward trajectory, with projected annual cash flows reaching $9.26 billion by 2035. Using a two-stage Free Cash Flow to Equity model, these projections place HCA’s estimated intrinsic value at $815.34 per share.

Given HCA’s latest closing price of $404.26, the DCF model suggests the stock is trading at a significant 50.4% discount to its fair value. In other words, it appears 50.4% undervalued by this measure. For those interested in value opportunities, this points to a notable gap between market price and estimated intrinsic worth.

Result: UNDERVALUED

Approach 2: HCA Healthcare Price vs Earnings

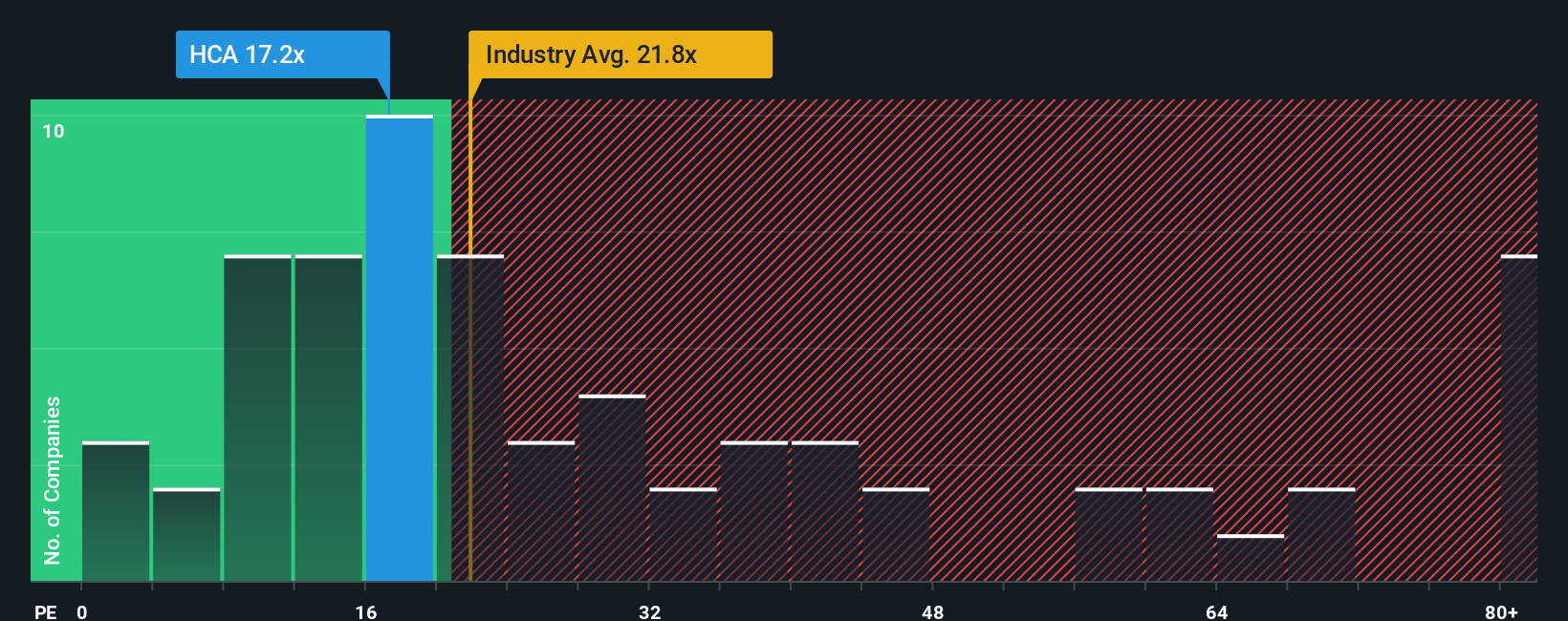

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies because it directly connects a company's share price to its earnings, offering an easy way to compare value across similar businesses. For growing companies with stable profits like HCA Healthcare, the PE ratio remains a central tool for understanding how the market values potential future earnings and the risks that may come with them.

HCA currently trades at a PE ratio of 15.8x. This is noticeably below the Healthcare industry average of 21.3x and its peer average of 18.4x. This suggests HCA is priced more conservatively than many comparable companies. However, when assessing fair value, it is important to go further than just these raw comparisons. The proprietary Fair Ratio from Simply Wall St considers multiple factors unique to HCA, including its earnings growth outlook, profitability, and industry landscape. It estimates that a fair PE for HCA would be 25.6x.

With HCA's current PE sitting well below the Fair Ratio, the stock appears to be undervalued using this multiple. This gap hints that the market may be underestimating HCA's future earnings potential or overestimating its risks relative to its peers and industry norms.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your HCA Healthcare Narrative

Narratives are a simple yet powerful investing tool that let you define the story behind the numbers for a company like HCA Healthcare, tying together your views on future revenue, earnings, profit margins, and what you believe the business is truly worth.

Instead of just looking at ratios or price charts, Narratives allow you to connect HCA’s business story to a financial forecast, and from there, to your personal fair value, making it much easier to see if now is a good time to buy or sell.

With the Simply Wall St platform, creating a Narrative is intuitive and accessible for everyone, whether you are a new investor or an experienced one. You can instantly compare your assumptions with millions of others in the community.

The real advantage of Narratives lies in their ability to update automatically as new developments emerge, such as a fresh earnings release or major headlines. This provides a dynamic way to refine your outlook and investment decision.

For example, some investors believe that HCA's strong growth and tech investments justify a price as high as $444, while others, concerned about regulatory risks and rising costs, see fair value at $333. Your Narrative can reflect whichever story aligns with your own research.

Do you think there's more to the story for HCA Healthcare? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com