Does Exxon Mobil’s Trinidad Expansion Signal a New Opportunity for Investors in 2025?

If you are watching Exxon Mobil right now, you are not alone. Many investors are weighing whether its recent moves signal a breakout opportunity or just another round of oil sector drama. With so much chatter about energy prices and the economy, it is worth asking: what is really happening with Exxon’s stock, and is now a smart time to act?

After a fairly flat start to the year, Exxon Mobil shares have started to pick up steam, gaining over 5% in the last three months. While the one-year total return sits just under break-even, you cannot ignore Exxon’s strong bounce over the past three and five years, with total returns topping 21% and 236% respectively. Some of the recent movement can be linked to upbeat news about potential investments, such as the possible $21.7 billion expansion if major reserves are found in Trinidad and Tobago. This kind of headline adds a layer of optimism among investors eager for new growth stories and less worried about ongoing debates around tariffs or industry risks.

But the real story for many is valuation. Out of six measures analysts look at to decide if Exxon is undervalued, the company checks four of the boxes. That gives it a valuation score of 4, a result that makes people sit up and take note when weighing risk versus reward. In the next section, I am going to dig into what these valuation checks mean, and why they might still not tell the whole story about value when it comes to Exxon Mobil.

Exxon Mobil delivered -1.2% returns over the last year. See how this stacks up to the rest of the Oil and Gas industry.Approach 1: Exxon Mobil Cash Flows

The Discounted Cash Flow (DCF) model is a key approach used to estimate a company’s true worth by projecting its future cash flows and discounting them back to today’s value. For Exxon Mobil, this involves evaluating how much cash the business is expected to generate over time and determining what that is worth in today’s dollars.

Currently, Exxon Mobil reports a strong Last Twelve Months Free Cash Flow of $32.4 billion. According to analyst projections and modeled estimates, this figure is expected to climb steadily, reaching nearly $51.6 billion by 2035. These forward-looking estimates reflect the company’s robust position in oil and gas operations and a positive outlook for free cash flow growth over the next decade.

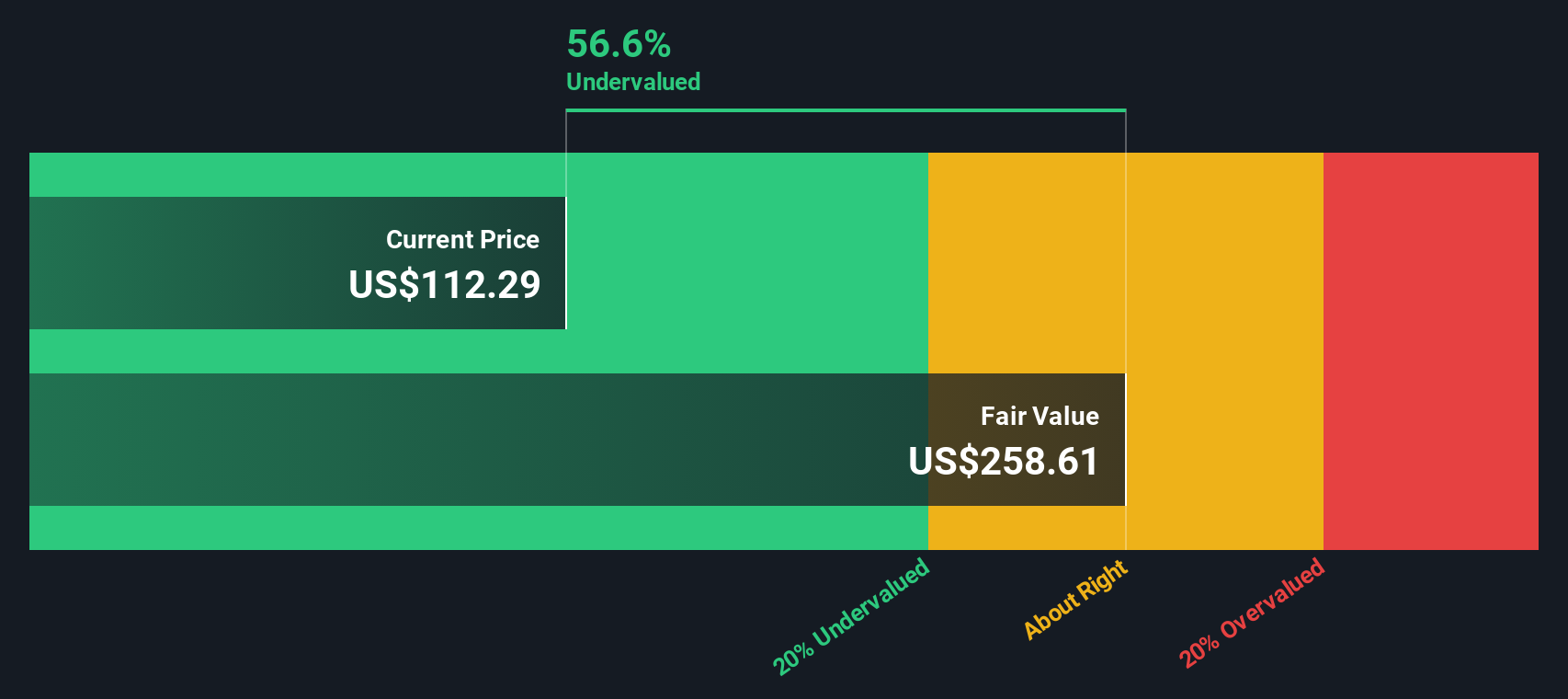

Based on these projections, Exxon’s estimated intrinsic value using a Two-Stage Free Cash Flow to Equity model is $245.30 per share. This is considerably higher than its present price, suggesting the stock is trading at a 55.8% discount to its intrinsic valuation. In other words, the analysis indicates Exxon Mobil may be significantly undervalued by the market at this time.

Result: UNDERVALUED

Approach 2: Exxon Mobil Price vs Earnings

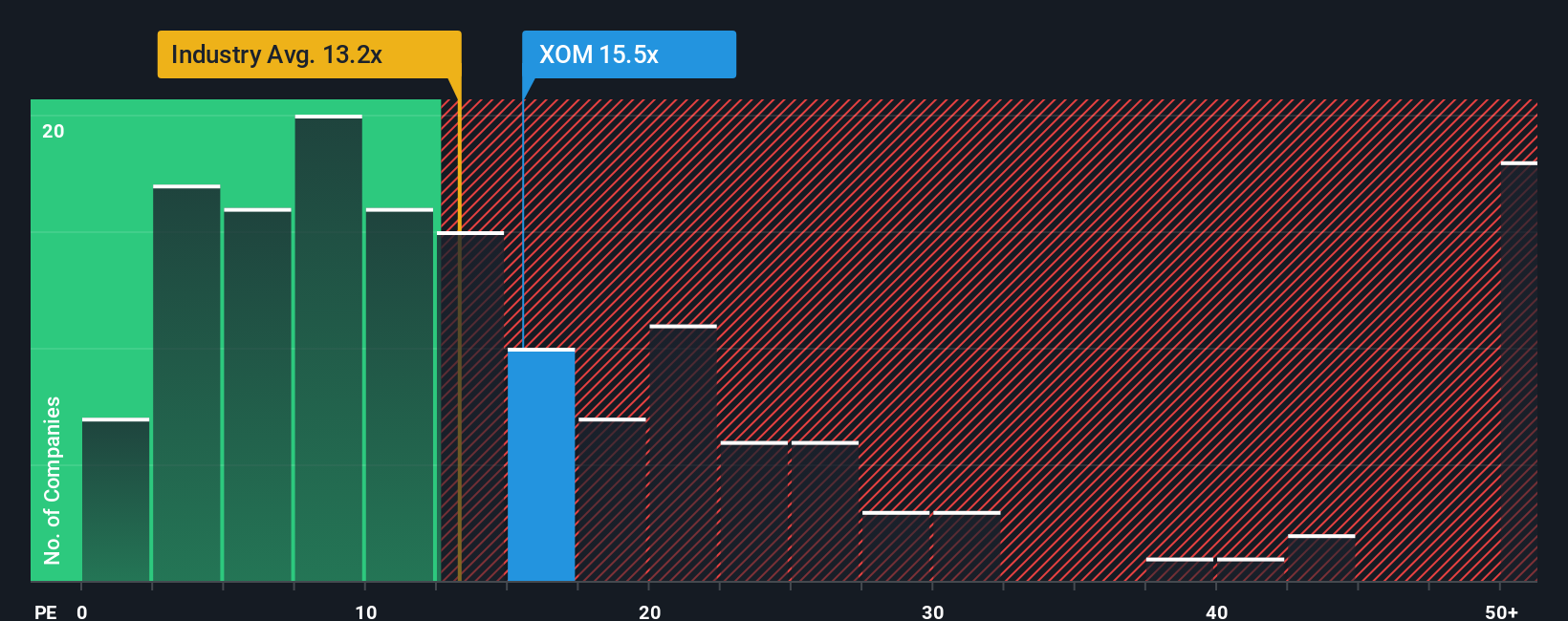

The Price-to-Earnings (PE) ratio is one of the most common ways to value profitable companies like Exxon Mobil, because it connects a company’s share price directly to its underlying earnings. This metric is popular with investors because it quickly reveals how much you are paying for a dollar of current profits. It also makes it easy to compare companies across peers and industries.

Growth expectations and risk play important roles in determining what a typical or “fair” PE ratio should be. Companies with strong prospects and lower risks typically trade at a higher PE ratio, while slower-growing or riskier firms are often valued at a lower ratio. At the moment, Exxon Mobil’s PE ratio stands at 14.9x, which is above the Oil and Gas industry average of 12.6x but below the average of its closest large-cap peers at 22.4x.

The Fair Ratio, as calculated by Simply Wall St, provides an objective benchmark that reflects expected earnings growth, profit margins, and risk factors specific to Exxon Mobil. For Exxon, the Fair Ratio is 18.7x. Comparing this to the current PE of 14.9x suggests that Exxon Mobil shares are trading below what would be considered a fair valuation given its risk and growth profile.

Result: UNDERVALUED

Upgrade Your Decision Making: Choose your Exxon Mobil Narrative

While valuation models like DCF and PE are powerful, they do not capture the story behind the numbers. This is where Narratives come in. A Narrative is simply a way to express your view or "story" about a company, connecting your expectations such as where revenue, earnings, and margins could head with a concrete fair value based on those beliefs.

Narratives link together everything from financial forecasts to industry trends, helping you see not just what a company is worth today, but why. On Simply Wall St, millions of investors can easily create, refine, and compare Narratives. This makes complex investment ideas feel more accessible and personal.

This approach lets you spot opportunities. When your Narrative-derived Fair Value is much higher than the current share price, it suggests a possible buy. If it is lower, it may be time to reconsider. The strength of Narratives is that they update automatically whenever new facts such as news, earnings, or forecasts arise, keeping your view current with the market.

For example, some Exxon Mobil Narratives estimate fair value as high as $174 by forecasting significant low-cost production growth in Guyana, while others see a fair value closer to $124, reflecting more modest earnings growth and sector risks. Which Narrative resonates with you?

Do you think there's more to the story for Exxon Mobil? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com