Cigna (CI): Exploring the Stock's Valuation as Shares Move Past $300

If you have been following Cigna Group (CI) lately, you’ve probably noticed the stock’s share price drifting higher. The increase has been subtle, but just enough to catch the eye. There hasn’t been a single major announcement sparking this move; however, with a share price now sitting above $300 and a year-to-date gain over 10%, many investors are wondering whether the recent momentum is revealing something about sentiment or simply reflects the normal ebb and flow of a maturing company. With healthcare in the spotlight for cost and innovation challenges, Cigna’s valuation merits a closer look.

Over the past year, shares of Cigna have declined nearly 9%. Even so, recent months showed some recovery from the lows, including a 6% jump in the past week alone. The stock’s three-year return just above 11% and a five-year gain close to 90% underscore its ability to generate long-term value, but the near-term picture is mixed. Cigna has also seen both annual revenue and net income climb in the mid-single digits, against a backdrop of large-scale sector competition and shifting U.S. healthcare policies.

After this combination of muted one-year performance and renewed upward momentum, is Cigna trading at a compelling value, or is the market already factoring in prospects for further growth?

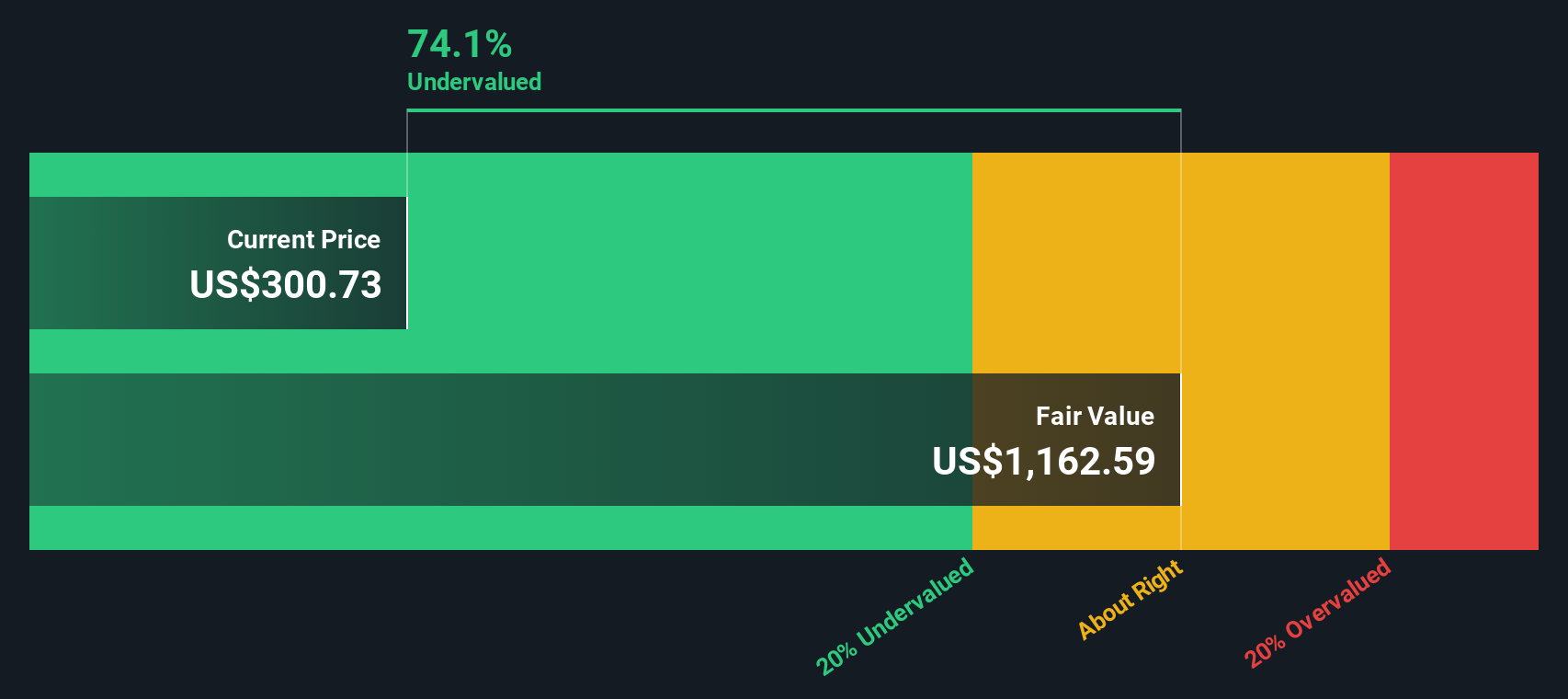

Most Popular Narrative: 17.2% Undervalued

According to community narrative, Cigna Group is seen as undervalued by analysts, with its fair value estimated well above the current share price. This view reflects optimism regarding future revenue and profit margins, underpinned by expansion in high-margin segments and continued innovation.

Cigna is capitalizing on the growing demand for specialty pharmacy and care services, particularly as chronic diseases and complex treatments become more prevalent. The double-digit revenue growth in CuraScript and Accredo positions the company to capture an expanding portion of the high-growth $400B+ specialty space, supporting long-term revenue and earnings growth.

There is more to this valuation than meets the eye. Behind the bullish analyst outlook are some surprising growth levers and financial assumptions that point to a transformation in Cigna’s core business. Want to find out what is powering that double-digit upside projection? You will want to see what the analysts are forecasting for the company’s future earnings, revenues, and profit margins. These are numbers that could shake up your view of the sector.

Result: Fair Value of $367.87 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, there are still significant risks, such as regulatory threats to pharmacy benefit margins and growing pressure on healthcare affordability, that could challenge this positive thesis.

Find out about the key risks to this Cigna Group narrative.Another View: Discounted Cash Flow Perspective

Taking a look from a different angle, our DCF model also points toward undervaluation for Cigna. This method considers future cash flows, rather than focusing only on what the market pays for sector peers. Which valuation approach gives the clearer picture?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Cigna Group Narrative

If these conclusions do not quite line up with your own research style or you prefer hands-on exploration, you can pull your own numbers and craft a different story in just a few minutes, or simply do it your way.

A great starting point for your Cigna Group research is our analysis highlighting 6 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Compelling Stock Ideas?

Don’t stop at Cigna. Some of the most exciting investment opportunities are just a click away. Give yourself an edge by checking out specialized lists designed to save you time and highlight companies that stand out. Join other smart investors by exploring these themes today:

- Capture steady income potential by reviewing dividend stocks with yields above 3% through dividend stocks with yields > 3% and find businesses that consistently reward shareholders.

- Discover undervalued companies with growth potential by scanning the latest picks based on strong cash flows and attractive valuations with undervalued stocks based on cash flows.

- Explore the momentum in artificial intelligence by looking into AI-driven companies shaping the future with AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com