Should You Reconsider Rocket Lab After Shares Surge More Than 50% in 2025?

If you have been eyeing Rocket Lab's stock and wondering whether now is the right time to make your move, you are not alone. Investors everywhere are weighing recent surges and pullbacks, trying to piece together what is next for this innovative space company. In just the past three months, shares have climbed nearly 59%, which is an impressive rebound that follows months of volatility and shifting risk appetite across growth stocks. Year-to-date, Rocket Lab has notched a 64% return, while over the past year, the gains have cooled to under 5% as cautious optimism returns to the market.

Rocket Lab's growth story is impossible to ignore, with annual revenue expanding by 26% and net income growing by an eye-popping 68%. Yet, mixed signals persist. The company's price currently sits about 11% below analysts' consensus targets, and its intrinsic valuation shows a deep discount of over 161%. These numbers might catch any value hunter's eye. Still, when it comes to classic value screens, Rocket Lab earns a score of 0 out of 6, indicating the stock does not pass any of the traditional undervaluation hurdles.

So, how do these figures stack up? In the next section, we will walk through the main valuation methods analysts use to assess Rocket Lab. But stay tuned, because after breaking down these models, we will explore an even smarter, bigger picture approach to figuring out what the company is really worth.

Rocket Lab delivered 484.6% returns over the last year. See how this stacks up to the rest of the Aerospace & Defense industry.Approach 1: Rocket Lab Cash Flows

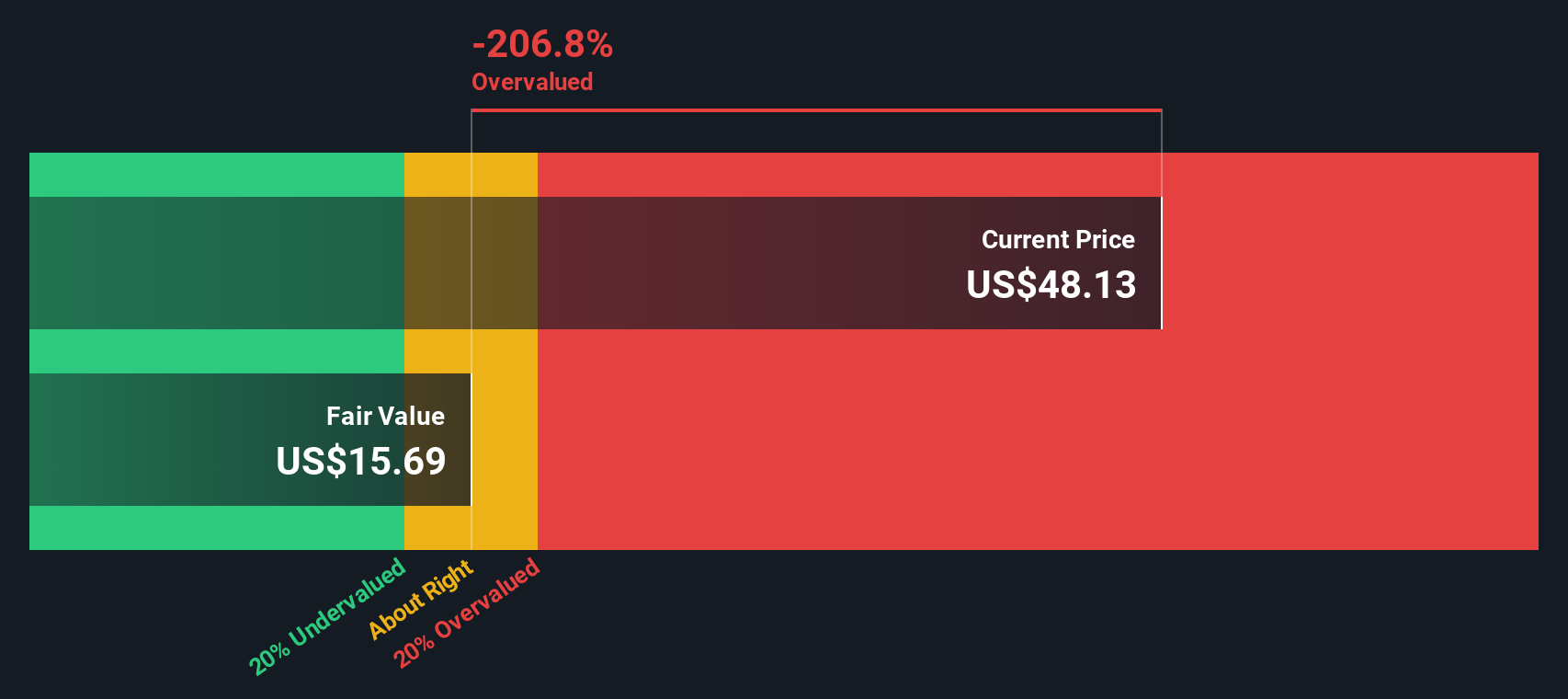

The Discounted Cash Flow (DCF) model is a classic way to estimate what a stock should be worth by projecting a company’s future cash flows and then discounting them back to today to reflect their present value. For Rocket Lab, the latest twelve months' Free Cash Flow sits at negative $208 million, reflecting ongoing investments and the early growth stage of the business.

Despite starting in the red, analysts expect Rocket Lab’s Free Cash Flow to turn positive and increase sharply over time. By 2027, projections show Free Cash Flow reaching $74 million, and in a decade, it could climb to more than $537 million. This marks a dramatic improvement and supports the growth narrative that has fueled market interest.

Using these projections, the DCF calculation produces an intrinsic fair value of $15.67 per share. Compared to Rocket Lab's current share price, this means the stock is 161.1% overvalued according to this model. In other words, shares trade well above what these future cash flows might justify based on the typical DCF approach.

Result: OVERVALUED

Approach 2: Rocket Lab Price vs Sales

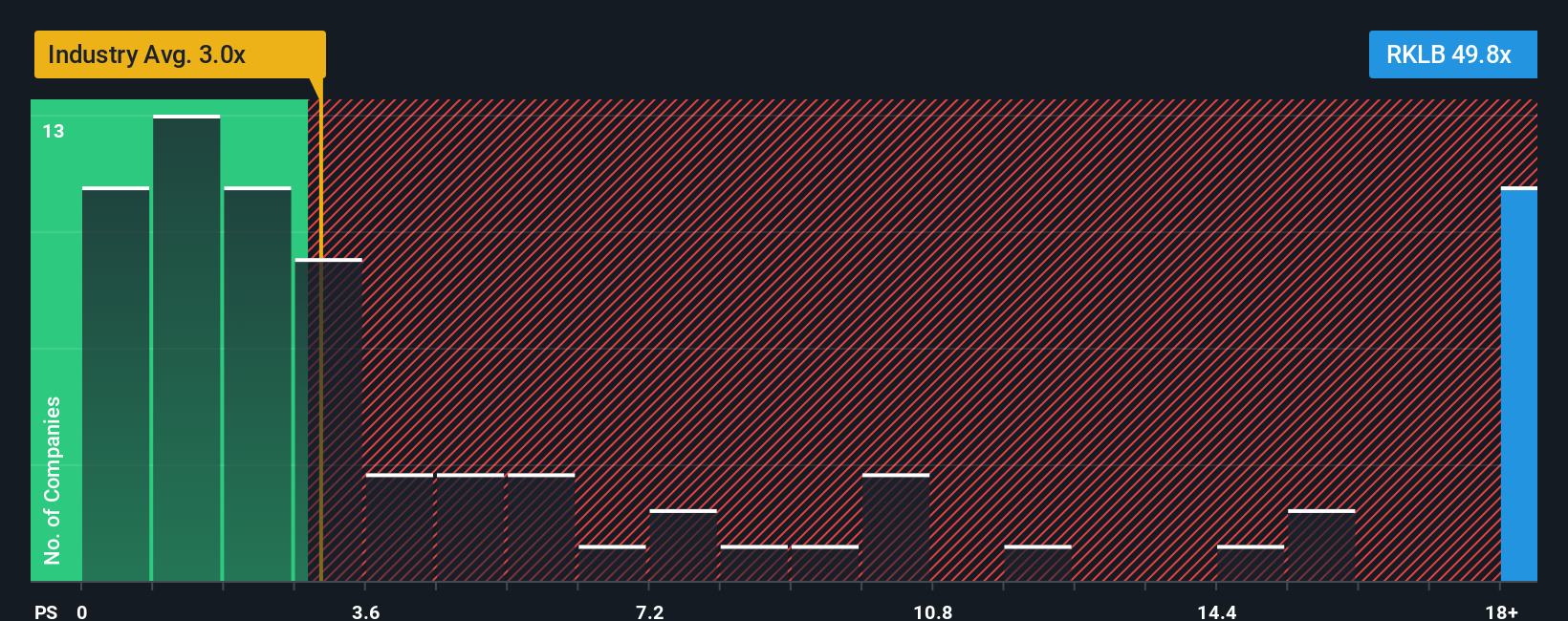

For many growing companies, the Price-to-Sales (PS) ratio is a popular valuation tool, especially when profitability is still on the horizon. This ratio allows investors to compare a company’s market value directly to its sales, making it easier to assess early-stage businesses with limited or negative earnings, such as Rocket Lab. Growth prospects and perceived risk both play important roles. Fast-growing firms with strong future potential can command higher PS ratios compared to the market average, while riskier or less certain outlooks tend to result in lower ratios.

Rocket Lab is currently trading at a PS ratio of 39.1x, which is well above the Aerospace and Defense industry average of 3.0x and its peer average of 8.6x. This premium highlights the market’s enthusiasm for Rocket Lab’s revenue growth and innovation, but also raises questions about the price investors are willing to pay for future potential. Simply Wall St’s Fair Ratio for Rocket Lab, which factors in growth rates, margins, and market dynamics, is 6.2x. This suggests that the current market price places a sizable premium relative to underlying fundamentals.

With Rocket Lab’s actual PS ratio substantially higher than its Fair Ratio, the stock appears significantly overvalued on this metric, even when accounting for strong growth expectations.

Result: OVERVALUED

Upgrade Your Decision Making: Choose your Rocket Lab Narrative

Instead of relying solely on numbers or ratios, Narratives let you define the story behind a company's future by combining your personal perspective on what Rocket Lab will achieve with forecasts for its revenue, earnings, and margins to reach your own fair value estimate.

A Narrative connects what you believe about Rocket Lab’s business, such as its competitive edge, risk factors, or big upcoming launches, directly to a financial model. This approach blends facts with your outlook to create a forecast that feels meaningful and actionable.

On Simply Wall St, Narratives are easy to create or adopt from the community. This allows millions of investors to test different assumptions, see how new information impacts fair value, and keep their approach current as news or results arrive.

This means Narratives not only help you spot when a stock’s price moves above or below your own fair value, indicating a potential buy or sell, but also enable you to adapt to fresh data as the market evolves, so your decisions remain informed and flexible.

- For example, the most optimistic Narrative for Rocket Lab sees a fair value of $55 per share, reflecting strong revenue growth and margin expansion, while the most cautious sets it at just $20 and focuses on execution risk and industry headwinds.

For Rocket Lab, we’ll make it really easy for you with previews of two leading Rocket Lab Narratives:

Fair value: $45.40

Undervalued by: 9.9%

Revenue growth: 37.5%

- Expanding end-to-end space solutions and vertical integration position Rocket Lab to win major national security and defense contracts, which could drive future margin and revenue growth.

- High launch frequency, satellite manufacturing, and reusable rocket development create a foundation for sustained multi-year revenue and backlog expansion in a rapidly growing industry.

- Profitability may be achieved as R&D investment shifts to production. However, ongoing risks include heavy reliance on large contracts, competition (especially from SpaceX), and the efficient integration of acquisitions.

Fair value: $31.72

Overvalued by: 29.0%

Revenue growth: 30.0%

- Rocket Lab’s ambitious $6 billion revenue target for 2035 depends on scaling its new Neutron rocket and maintaining a high launch frequency, all while competing against established heavyweights like SpaceX.

- Low-cost launches and expanding ‘Space Systems’ services are strengths, but achieving sustainable net margins is critical for funding growth and transitioning from cash burn to cash generation.

- Risks include technical and financial hurdles in scaling operations, dependence on successful Neutron launches, and a need for prudent capital management to navigate industry challenges and competition.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com