How dentalcorp Holdings' Profit Turnaround and Upbeat Outlook Will Impact TSX:DNTL Investors

- dentalcorp Holdings Ltd. recently announced its second quarter 2025 results, reporting sales of CA$435.2 million and turning from a net loss of CA$11.9 million last year to a net income of CA$0.9 million this quarter, while also reducing its six-month net loss to CA$9.3 million from CA$23.6 million a year earlier.

- The company also issued new guidance for the third quarter of 2025, projecting a 10% to 12% increase in revenue and growth in SPRG1, signaling continued positive momentum in its operations compared to the prior year.

- We'll explore how dentalcorp Holdings' improved profitability and upbeat outlook may reinforce analysts' views on its growth trajectory.

AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

dentalcorp Holdings Investment Narrative Recap

To be a shareholder in dentalcorp Holdings, you need to have confidence in management's ability to convert the aging population and high recurring patient base into sustained revenue growth, even while the company manages integration and debt risks from an active acquisition strategy. The recent swing to profitability in Q2 and solid Q3 outlook support the key short-term catalyst of translating scale into improved margins. However, the single biggest risk remains the company’s high financial leverage, which could amplify future challenges if financial performance falters; the recent earnings improvement helps but does not eliminate this risk.

The company’s latest guidance for Q3 2025, projecting revenue growth of 10% to 12% and 3% to 5% SPRG, is the most pertinent recent announcement, reinforcing near-term positive sentiment. This guidance aligns with continued patient growth and revenue expansion, key facets for supporting the company’s acquisition-driven thesis and offsetting pressure from recent cost and regulatory risks.

By contrast, investors should be aware that even with positive momentum in revenue, the company's reliance on debt means any shift in cash flows or interest rates could...

Read the full narrative on dentalcorp Holdings (it's free!)

dentalcorp Holdings' outlook projects CA$2.1 billion in revenue and CA$116.6 million in earnings by 2028. This assumes an 8.6% annual revenue growth rate and a CA$161.7 million increase in earnings from the current CA$-45.1 million.

Uncover how dentalcorp Holdings' forecasts yield a CA$12.66 fair value, a 56% upside to its current price.

Exploring Other Perspectives

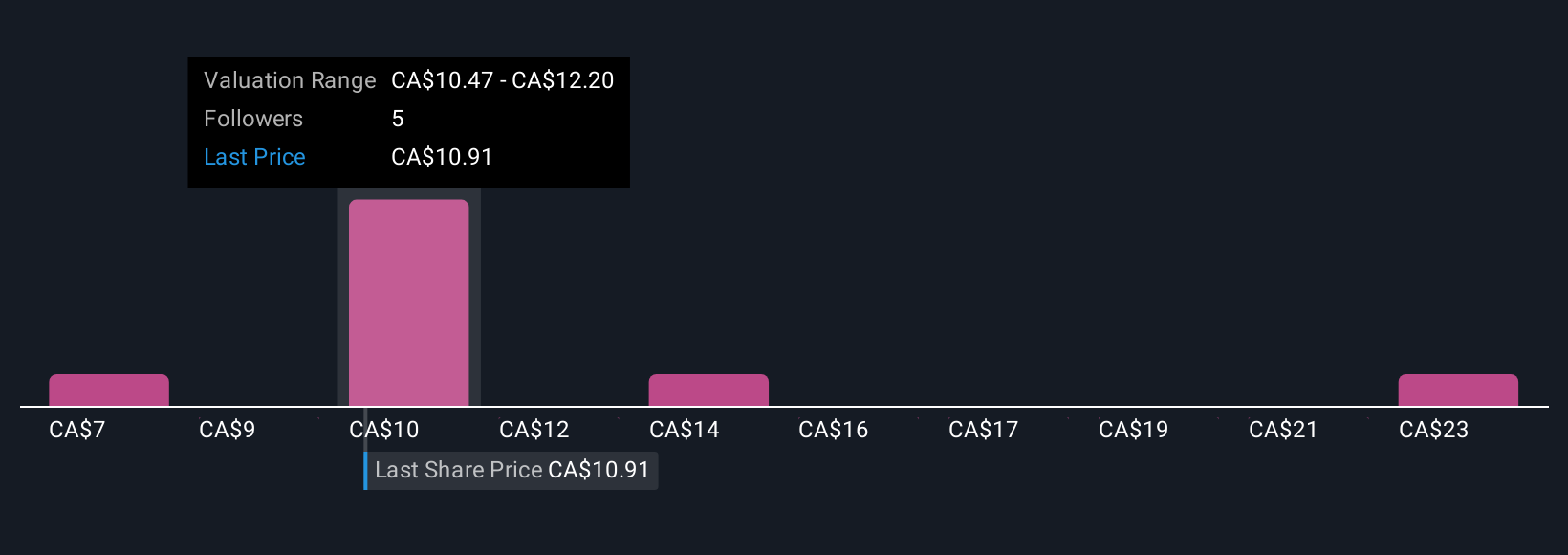

Retail investors in the Simply Wall St Community posted fair value estimates for dentalcorp Holdings from CA$7.00 to CA$24.40, with four distinct perspectives considered. Many see attractive valuation, yet acquisition risks remain a key consideration for the company’s performance outlook, so you may want to compare these viewpoints before making up your mind.

Explore 4 other fair value estimates on dentalcorp Holdings - why the stock might be worth over 3x more than the current price!

Build Your Own dentalcorp Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your dentalcorp Holdings research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free dentalcorp Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate dentalcorp Holdings' overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com