Alnylam Raises 2025 Revenue Guidance as Losses Widen Might Change The Case For Investing In ALNY

- Alnylam Pharmaceuticals raised its full-year 2025 net product revenue guidance to between US$2.65 billion and US$2.8 billion following the release of its second-quarter results, which showed revenue growth to US$773.69 million and an increased net loss to US$66.28 million for the quarter ended June 30, 2025.

- While overall revenues saw substantial gains year-over-year, the company also reported a larger net loss and higher basic loss per share from continuing operations compared to the prior period.

- With Alnylam's significantly raised revenue guidance, we'll assess how this outlook update may influence the company’s future growth trajectory.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam Pharmaceuticals, you need to believe in the long-term potential of its RNAi therapeutics and the ability of its flagship drug, AMVUTTRA, to unlock significant global markets. The recent sharp increase in revenue guidance signals confidence in demand and supports optimism around Alnylam’s commercial trajectory, but the higher net loss highlights that sustained profitability remains an important short-term hurdle; this shift does not fundamentally alter the key risk of margin pressure from ongoing commercialization costs.

The raised full-year revenue forecast, increased by roughly US$600 million compared to previous guidance, stands out as the most relevant development, underscoring how fast AMVUTTRA’s adoption may be scaling alongside international launches. While this reinforces revenue growth as a near-term catalyst, it also places greater scrutiny on whether revenues can outpace rising expenses and offset concentration risks as Alnylam pushes toward profitability.

Yet against these positives, investors should be alert to the impact of rising commercialization and R&D expenses, as there is...

Read the full narrative on Alnylam Pharmaceuticals (it's free!)

Alnylam Pharmaceuticals' outlook anticipates $7.0 billion in revenue and $1.9 billion in earnings by 2028. This scenario depends on a 41.7% annual revenue growth rate and a $2.2 billion earnings increase from current earnings of -$319.1 million.

Uncover how Alnylam Pharmaceuticals' forecasts yield a $424.64 fair value, in line with its current price.

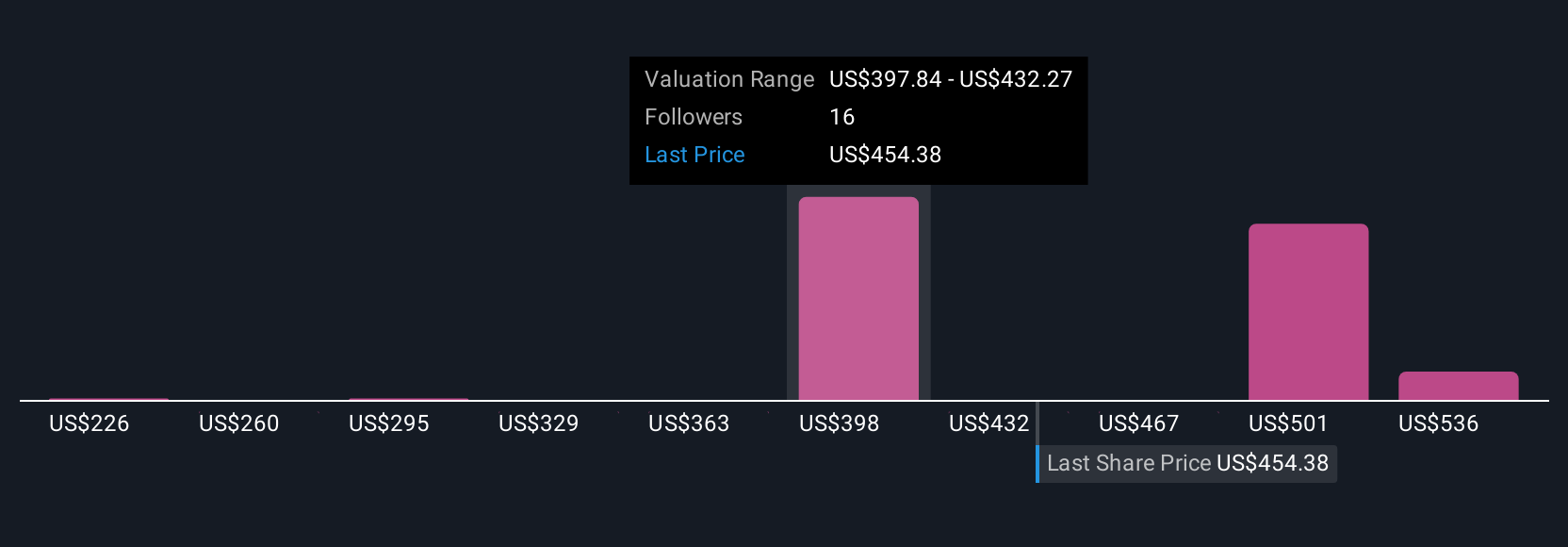

Exploring Other Perspectives

Five members of the Simply Wall St Community valued Alnylam between US$225.68 and US$1,924.18 per share. Revenue acceleration remains at the heart of the discussion and highlights how opinions on future performance can differ widely.

Explore 5 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth 48% less than the current price!

Build Your Own Alnylam Pharmaceuticals Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 1 key reward that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com