Top Undervalued Small Caps With Insider Action In August 2025

As the U.S. stock market reaches new heights with the S&P 500 and Nasdaq hitting record highs, optimism is fueled by expectations of potential interest rate cuts following steady inflation numbers. In this buoyant environment, small-cap stocks can offer unique opportunities for investors seeking growth potential, particularly when insider actions suggest confidence in a company's prospects.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Angel Oak Mortgage REIT | 5.8x | 3.8x | 41.78% | ★★★★★★ |

| PCB Bancorp | 10.1x | 3.0x | 31.56% | ★★★★★☆ |

| First United | 9.5x | 2.8x | 45.66% | ★★★★★☆ |

| S&T Bancorp | 11.1x | 3.7x | 39.47% | ★★★★☆☆ |

| GEN Restaurant Group | NA | 0.1x | -640.12% | ★★★★☆☆ |

| Lindblad Expeditions Holdings | NA | 1.0x | 12.99% | ★★★★☆☆ |

| Citizens & Northern | 11.3x | 2.8x | 42.89% | ★★★☆☆☆ |

| Shore Bancshares | 9.9x | 2.5x | -74.91% | ★★★☆☆☆ |

| Blue Bird | 15.5x | 1.3x | -15.79% | ★★★☆☆☆ |

| Farmland Partners | 7.1x | 8.6x | -42.31% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

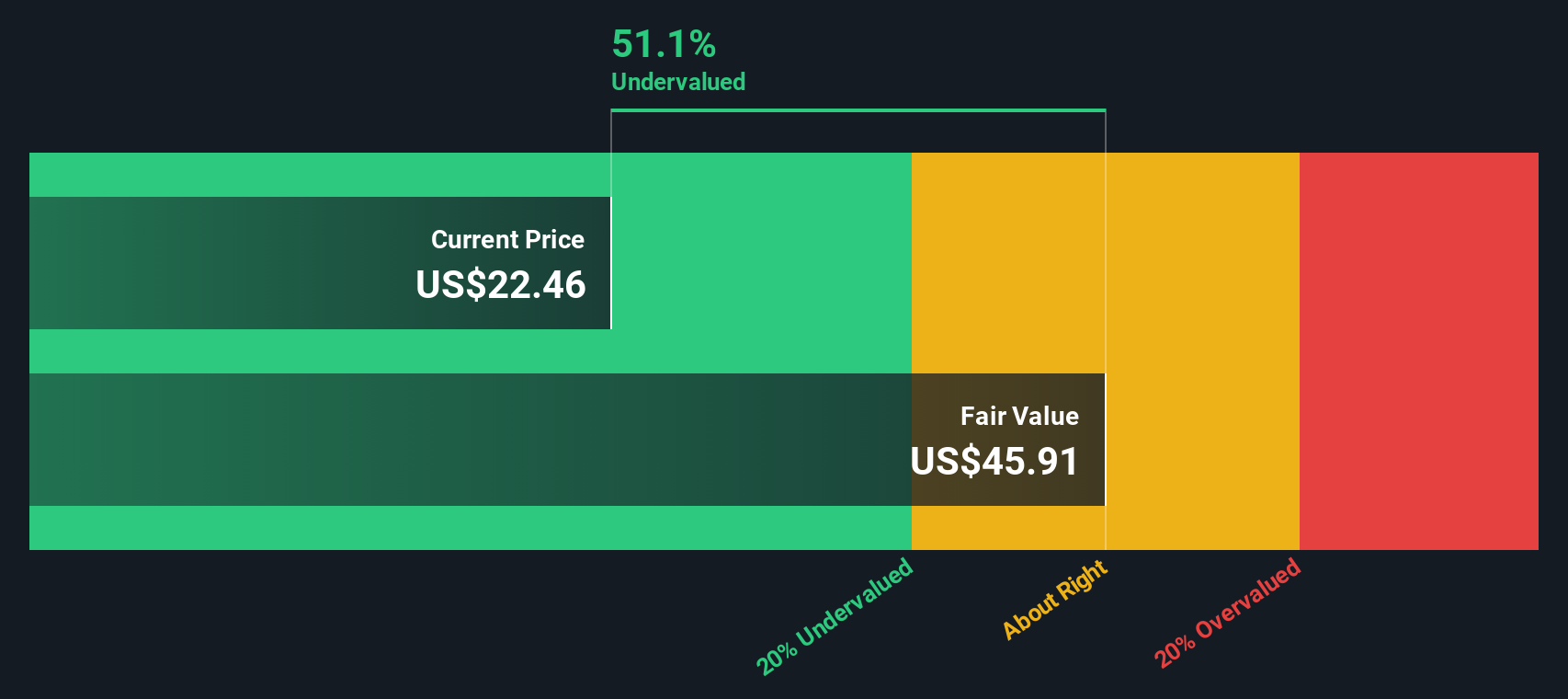

First Busey (BUSE)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: First Busey is a financial holding company that provides banking, wealth management, and technology services with a market capitalization of approximately $1.48 billion.

Operations: The company's primary revenue streams are derived from Banking, Firs Tech, and Wealth Management segments, with the Banking segment contributing significantly at $435.30 million. Operating expenses have shown a notable increase over time, reaching $332.61 million in 2025-06-30. The net income margin has fluctuated across periods, peaking at 31.78% in 2021-03-31 before declining to 15.52% by mid-2025.

PE: 26.8x

First Busey, a company with insider confidence shown through recent share repurchases, has seen its net interest income rise significantly, hitting US$153.18 million in Q2 2025 from US$82.53 million the previous year. Despite a dip in profit margins from 25.8% to 15.5%, earnings per share improved slightly over the same period. The company also declared dividends on both common and preferred stocks recently, reflecting its commitment to shareholder returns amidst ongoing financial adjustments and growth forecasts of 71% annually in earnings.

- Click here to discover the nuances of First Busey with our detailed analytical valuation report.

Evaluate First Busey's historical performance by accessing our past performance report.

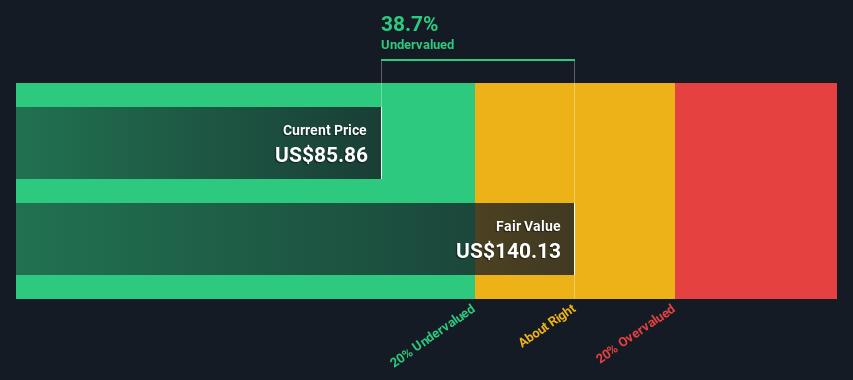

ICF International (ICFI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: ICF International provides professional services to a broad array of clients and has a market capitalization of approximately $2.4 billion.

Operations: ICFI generates revenue primarily through professional services, with a gross profit margin that fluctuated from 37.26% to 37.12% over the observed periods. The company's cost structure is heavily influenced by COGS and operating expenses, which include general and administrative costs, consistently accounting for a significant portion of its expenditures. Net income margins have shown variability, ranging between approximately 3.59% and 5.45%, reflecting changes in non-operating expenses and other financial factors over time.

PE: 16.4x

ICF International, a smaller company in the U.S., is navigating a challenging financial landscape with declining earnings and high debt levels. Despite this, they are expanding their AI offerings for federal agencies through ICF Fathom™, aiming to boost efficiency and productivity. The company's strategic focus includes acquisitions and organic growth while managing debt. Recently added to several value indices, ICF's potential lies in its adaptability and innovation within government services despite anticipated revenue declines this year.

- Click here and access our complete valuation analysis report to understand the dynamics of ICF International.

Assess ICF International's past performance with our detailed historical performance reports.

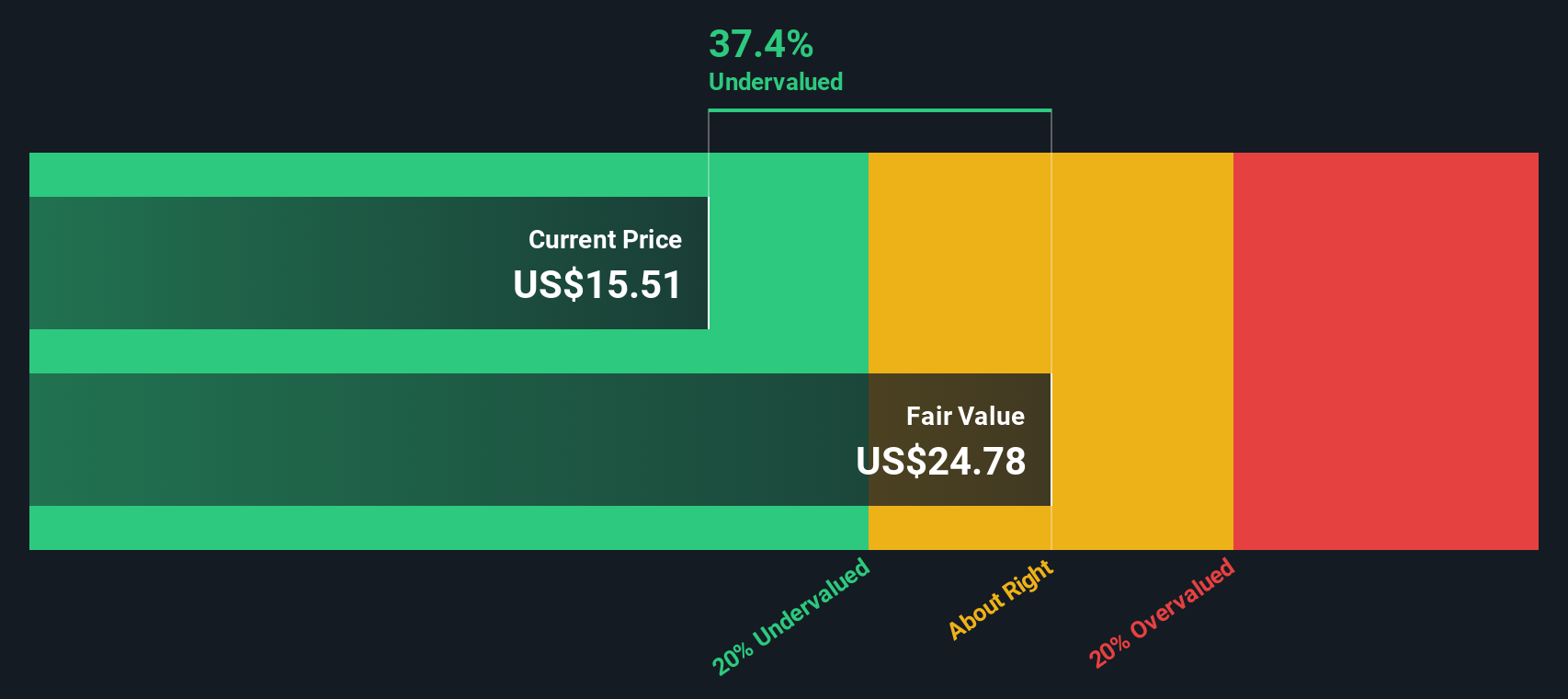

Sally Beauty Holdings (SBH)

Simply Wall St Value Rating: ★★★★★☆

Overview: Sally Beauty Holdings operates as a specialty retailer and distributor of professional beauty supplies through its Sally Beauty Supply and Beauty Systems Group segments, with a market cap of approximately $1.24 billion.

Operations: SBS and BSG contribute significantly to the company's revenue, with SBS generating $2.09 billion and BSG contributing $1.60 billion. The gross profit margin has shown a gradual increase from 49.56% in late 2014 to 51.39% by mid-2025, indicating an improvement in cost management relative to sales growth over this period. Operating expenses consistently form a substantial part of the cost structure, with general and administrative expenses being the largest component within operating costs across multiple periods.

PE: 6.4x

Sally Beauty Holdings, a company with significant insider confidence demonstrated through recent share purchases, is navigating the challenges of high debt levels and external borrowing. Despite these hurdles, the company's Q3 2025 earnings showed positive growth in net income to US$45.72 million from US$37.72 million a year ago. The company repurchased 1.5 million shares for US$13 million between April and June 2025, indicating strategic financial maneuvers amid flat sales projections for the year due to fewer stores and foreign exchange impacts.

Make It Happen

- Click this link to deep-dive into the 89 companies within our Undervalued US Small Caps With Insider Buying screener.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com