- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalWhat Brighthouse Financial (BHF)'s Jump in Profit and Share Buybacks Means for Shareholders

- Brighthouse Financial reported second quarter 2025 results, with revenue of US$871 million and net income of US$85 million, compared to US$1.43 billion and US$34 million respectively a year earlier, while also completing a major share buyback program repurchasing over 6.3 million shares for US$334.77 million.

- The company highlighted higher profitability despite lower revenue, robust annuity and life insurance sales, expense control, and revised hedging strategies, reinforcing its focus on capital efficiency and operational execution.

- We'll explore how the significant improvement in profitability and share buybacks influence Brighthouse Financial's longer-term investment outlook.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Brighthouse Financial Investment Narrative Recap

Owning shares in Brighthouse Financial means believing in the company’s ability to maintain strong annuity and life sales, manage complex product risks, and deliver profitable growth despite industry headwinds. The recent earnings report, with improved profitability but lower revenue, does not materially affect the key short-term catalyst, ongoing growth in annuity sales, or ease the main risk, which is persistent outflows and surrender rates in legacy blocks that may pressure future growth.

Among recent updates, completion of the share buyback program stands out, signaling significant capital returned to shareholders in the past year. While this effort reduces share count and can support earnings per share, it does not address the root challenges associated with Brighthouse's reliance on the variable annuity and Shield blocks, where elevated outflows and surrender rates remain a concern for top-line expansion.

Yet, despite this disciplined approach to capital return, investors should be aware that persistent product outflows could still...

Read the full narrative on Brighthouse Financial (it's free!)

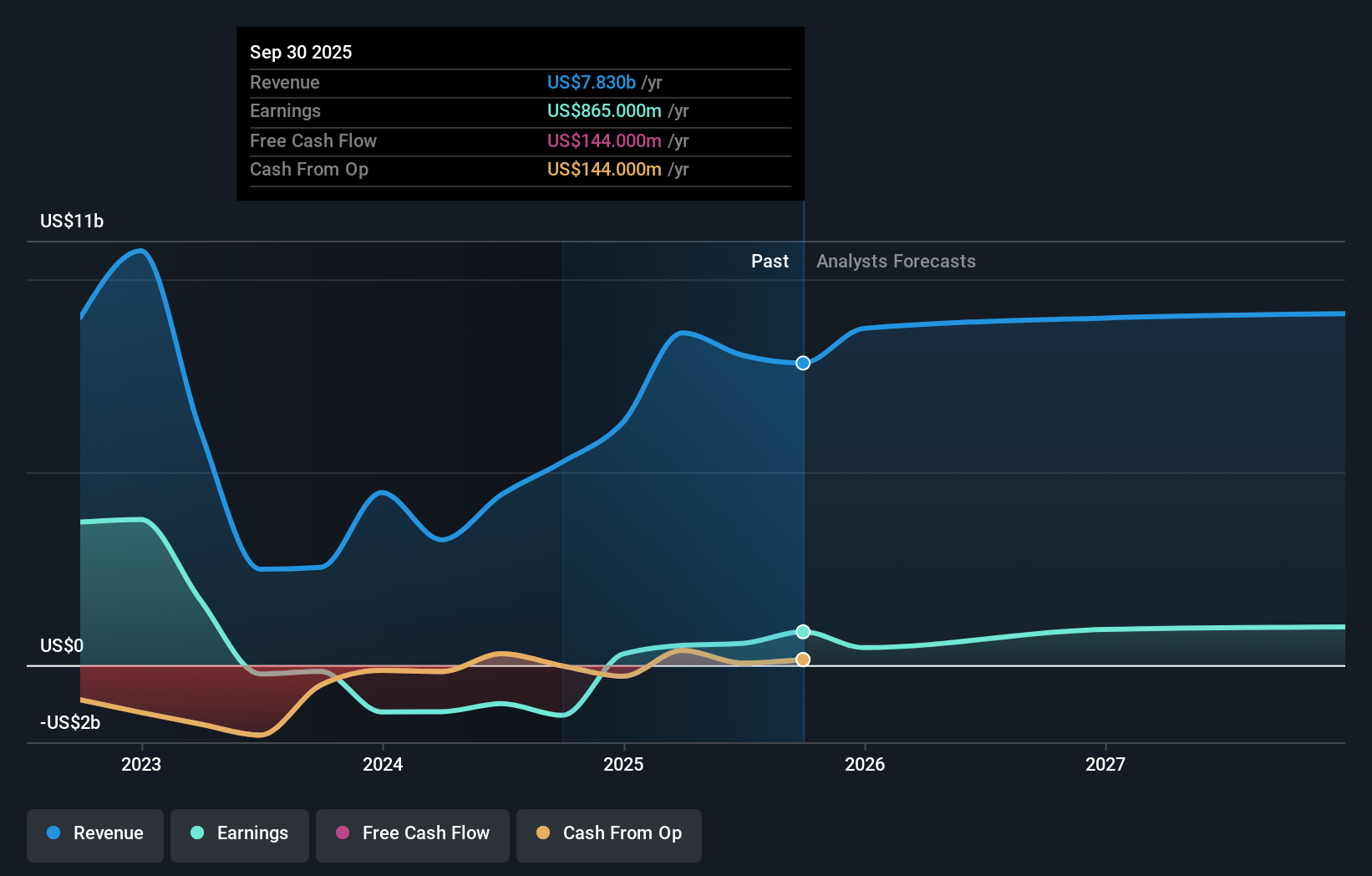

Brighthouse Financial's narrative projects $9.4 billion in revenue and $980.5 million in earnings by 2028. This requires 2.9% yearly revenue growth and a $469.5 million earnings increase from $511.0 million currently.

Uncover how Brighthouse Financial's forecasts yield a $59.44 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Private investor fair value estimates for Brighthouse Financial in the Simply Wall St Community span from US$59.44 to US$112.55, based on two distinct views. While these reflect wide-ranging opinions, the company’s reliance on legacy annuity products remains a concern for future revenue and profit trends, so consider how different viewpoints weigh these structural risks.

Explore 2 other fair value estimates on Brighthouse Financial - why the stock might be worth over 2x more than the current price!

Build Your Own Brighthouse Financial Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Brighthouse Financial research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Brighthouse Financial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Brighthouse Financial's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Outshine the giants: these 18 early-stage AI stocks could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com