How Teleflex’s (TFX) BIOTRONIK Acquisition and Raised Guidance May Shape Its 2025 Growth Path

- Earlier this month, Teleflex Incorporated’s Board of Directors declared a quarterly dividend of US$0.34 per share, and the company reported second quarter sales of US$780.89 million with net income of US$122.58 million, alongside raised full-year guidance following the acquisition of BIOTRONIK’s Vascular Intervention business.

- Teleflex’s updated outlook now reflects expected higher 2025 revenues and earnings, citing acquisition-related expansion and a positive impact from recent foreign exchange movements.

- Let’s examine how Teleflex’s improved revenue guidance, driven by the BIOTRONIK acquisition, reshapes its growth and earnings outlook going forward.

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Teleflex Investment Narrative Recap

To be a shareholder in Teleflex, you’d want confidence in the company’s ability to grow steadily by innovating in advanced surgical and interventional products, while successfully integrating acquisitions to drive both near- and long-term profits. The recent raised revenue and earnings guidance following the BIOTRONIK acquisition is now the primary short-term catalyst, but the complexity of integrating this business remains the greatest risk and could meaningfully affect the benefits investors expect if challenges emerge.

Teleflex’s update to its full-year guidance is particularly significant. The company is now projecting 9.00% to 10.00% GAAP revenue growth for 2025, up sharply from prior guidance, primarily reflecting expected contributions from BIOTRONIK’s Vascular Intervention business as well as a foreign exchange boost, meaning the acquisition’s near-term impact is substantial for both sales and earnings outlooks.

Yet, despite improved financial forecasts, investors should consider the integration risks that could arise with such a large acquisition, particularly since...

Read the full narrative on Teleflex (it's free!)

Teleflex's narrative projects $3.8 billion in revenue and $544.4 million in earnings by 2028. This requires 8.1% yearly revenue growth and a $352.5 million increase in earnings from $191.9 million today.

Uncover how Teleflex's forecasts yield a $140.11 fair value, a 17% upside to its current price.

Exploring Other Perspectives

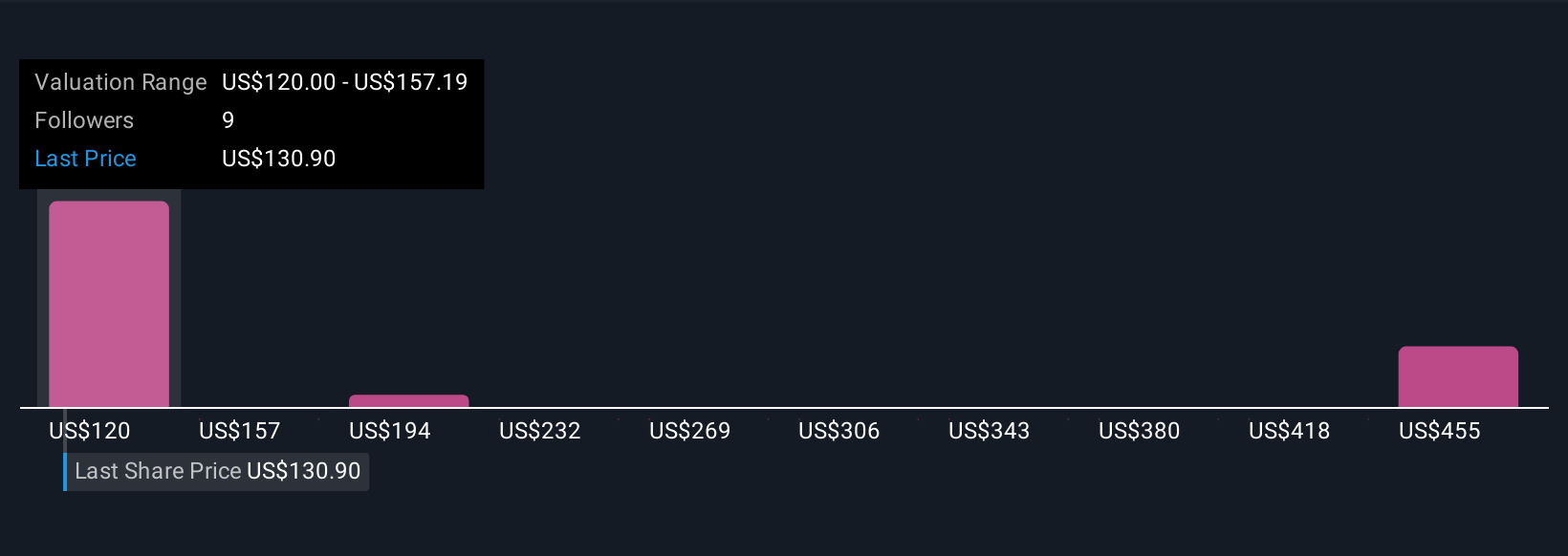

Simply Wall St Community members offered four fair value estimates for Teleflex ranging from US$120 to nearly US$470 per share. While the BIOTRONIK deal has boosted official guidance, integration challenges may weigh on the company’s ability to meet new targets, giving you several opinions to weigh as you form your own view.

Explore 4 other fair value estimates on Teleflex - why the stock might be worth just $120.00!

Build Your Own Teleflex Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Teleflex research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Teleflex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Teleflex's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com