Can Masimo’s New Leadership Drive Sustainable Growth After Strong Q2 and Upbeat Outlook for MASI?

- Masimo Corporation recently reported second quarter 2025 results, with sales rising to US$370.9 million and net income increasing to US$51.3 million, alongside several key executive appointments and the rollout of new leadership roles in commercial, quality, regulatory, and information technology functions.

- In addition to a strong quarterly performance, Masimo’s updated full-year guidance projects GAAP revenue between US$1.51 billion and US$1.54 billion, reflecting anticipated revenue growth of 8% to 10% for 2025.

- We’ll examine how Masimo’s improved full-year revenue outlook and new leadership hires impact the broader investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Masimo Investment Narrative Recap

Owning Masimo stock often reflects a belief in the company’s ability to drive innovation in patient monitoring, capitalize on expanding specialty markets, and execute amid industry risks. The latest Q2 results, showing strong revenue and profit growth, support the case for improved execution, but do not materially shift the key short-term catalyst: the need to gain greater market share in underpenetrated areas, nor does it diminish the continued risk around exposure to shifting global tariffs and unpredictable hospital purchasing patterns.

Of the recent company announcements, the appointment of Greg Meehan as Chief Commercial Officer is particularly relevant, as building out commercial capabilities is directly tied to the top-line growth highlighted in Masimo’s guidance. Meehan’s tenure in the medical technology sector will be watched closely for its impact on accelerating adoption in next-generation monitoring and increasing success with hospital contracts, which remains central to Masimo’s near-term growth ambitions.

But despite this commercial expansion, investors should watch closely for signals that rising tariff pressures could undermine...

Read the full narrative on Masimo (it's free!)

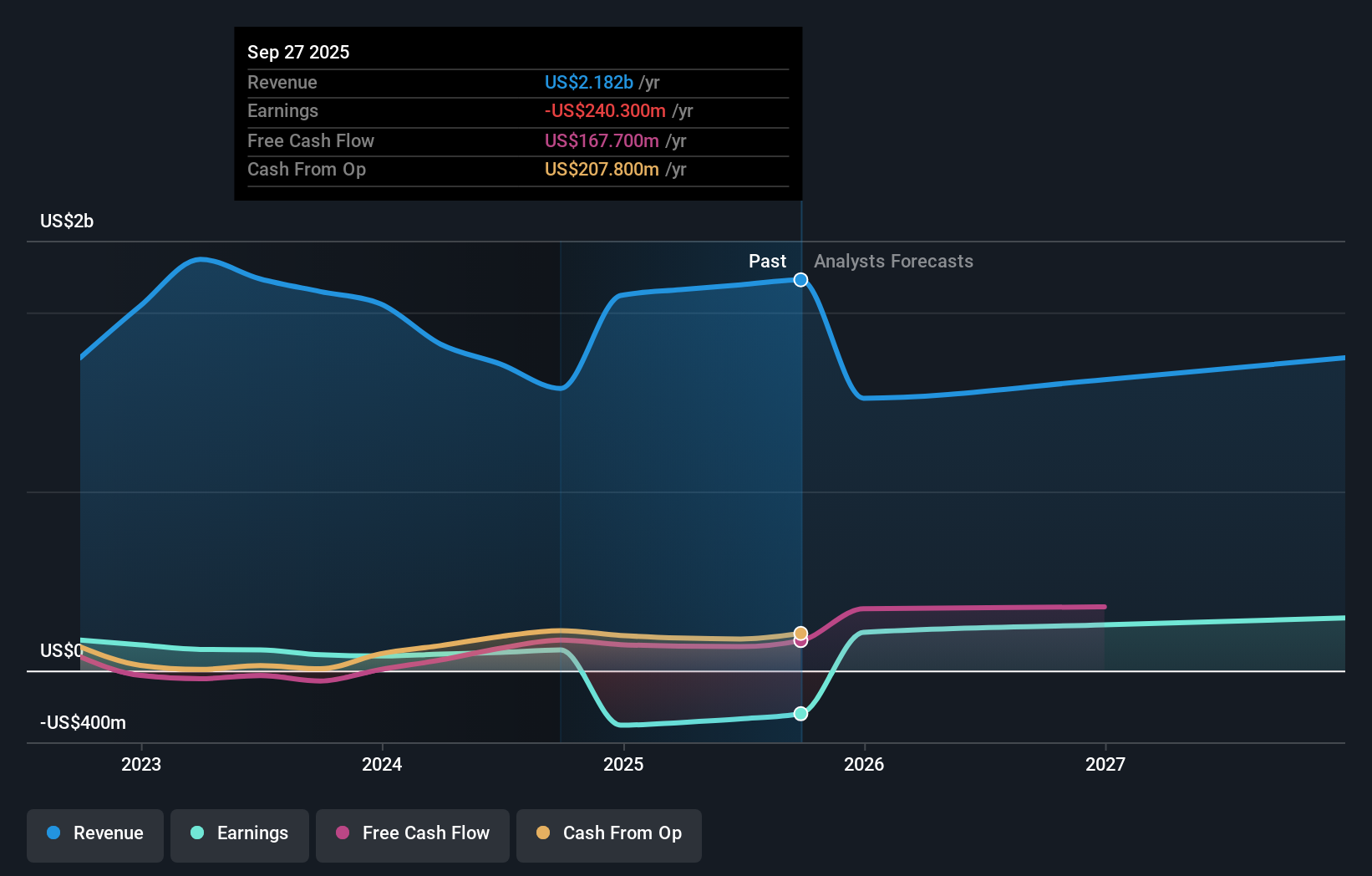

Masimo's outlook anticipates $1.8 billion in revenue and $293.5 million in earnings by 2028. This reflects a projected 5.0% annual decline in revenue and a $563.2 million increase in earnings from the current -$269.7 million.

Uncover how Masimo's forecasts yield a $187.57 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members project Masimo’s fair value estimates from US$137.02 to US$187.57, reflecting a wide spectrum of three individual analyses. While opinions vary greatly, ongoing exposure to new and fluctuating global tariffs may influence longer-term margin prospects and could be pivotal in shaping future investor sentiment.

Explore 3 other fair value estimates on Masimo - why the stock might be worth 7% less than the current price!

Build Your Own Masimo Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Masimo research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Masimo research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Masimo's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com