Is PureCycle's Widening Q2 Loss Reshaping the Investment Case for PCT?

- PureCycle Technologies announced its second quarter 2025 financial results, reporting US$1.65 million in sales and a net loss of US$144.24 million, a substantial increase compared to the same period last year.

- Despite marginal sales growth, the company saw its net loss grow considerably year-on-year, highlighting mounting challenges in achieving profitability.

- With the second quarter revealing widening losses, we'll explore what this means for PureCycle Technologies' investment narrative and future direction.

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

What Is PureCycle Technologies' Investment Narrative?

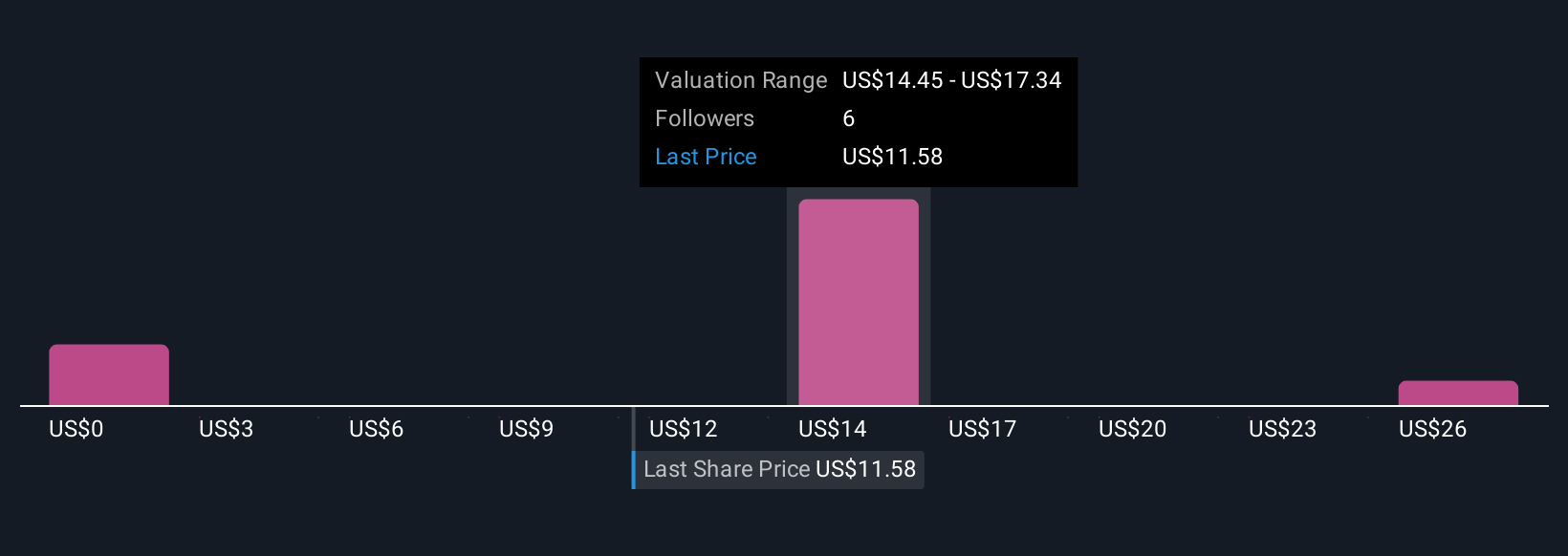

To own PureCycle Technologies stock, you have to believe in the company's vision to deliver scalable, sustainable polypropylene recycling despite ongoing financial and operational hurdles. The Q2 2025 results, revealed on August 7, spotlight a steepening net loss of US$144.24 million despite scant sales growth, which could put an even brighter spotlight on PureCycle’s path toward commercial traction and profitability. Previously, investors were focused on operational milestones like scaling production at Ironton, major commercialization wins, and the pace of cost reduction as the key near-term catalysts. However, the jump in quarterly net loss and only negligible top-line growth suggest higher short-term cash burn risk, raising questions about capital needs and funding sources, particularly after recent index removals and fresh preferred stock issuances. For the moment, the latest results make PureCycle’s urgency to prove consistent revenue growth and cost discipline even more central to its investment case.

But there’s a growing risk that capital requirements could intensify, something investors need to keep an eye on.

Exploring Other Perspectives

Explore 5 other fair value estimates on PureCycle Technologies - why the stock might be worth over 2x more than the current price!

Build Your Own PureCycle Technologies Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your PureCycle Technologies research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

- Our free PureCycle Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PureCycle Technologies' overall financial health at a glance.

Ready For A Different Approach?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 20 early-stage AI stocks could fund your retirement.

- We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com