EchoStar (SATS) Is Down 17.8% After Widening Q2 Losses and Lower Revenue—Has the Bull Case Changed?

- EchoStar Corporation recently announced its second quarter 2025 earnings, reporting revenues of US$3.72 billion and a net loss of US$306.13 million, both declining compared to the same period last year.

- This widening net loss and reduced revenue highlight ongoing operational pressures and underline the financial challenges EchoStar is currently experiencing.

- We'll assess how expanding net losses and falling revenue may alter EchoStar’s investment narrative, especially regarding future profitability assumptions.

Find companies with promising cash flow potential yet trading below their fair value.

EchoStar Investment Narrative Recap

To remain a shareholder in EchoStar, you need to believe that the company’s investments in next-generation telecommunications, broadband, and 5G will lead to sustainable revenue growth as the DISH Network merger matures. However, the most recent quarterly results, showing further deterioration in both revenue and net loss, dose short-term optimism as the immediate catalyst for recovery is under pressure, while the main risk of persistent negative cash flow remains highly relevant for near-term prospects.

Among recent developments, no announcement is more directly tied to current risks than the June 2025 disclosure that EchoStar might pursue bankruptcy protection for its wireless licenses, reflecting the intensifying financial constraints highlighted by the widening losses in Q2. This adds urgency to the question of whether the company’s balance sheet and liquidity position can support its turnround strategy amid ongoing operational pressures.

In contrast, investors should be aware that the company’s ability to manage its cash flow obligations could become a critical concern if current trends persist...

Read the full narrative on EchoStar (it's free!)

EchoStar's narrative projects $16.4 billion in revenue and $1.5 billion in earnings by 2028. This requires 1.4% yearly revenue growth and an earnings increase of $1.7 billion from current earnings of -$214.8 million.

Uncover how EchoStar's forecasts yield a $40.36 fair value, a 50% upside to its current price.

Exploring Other Perspectives

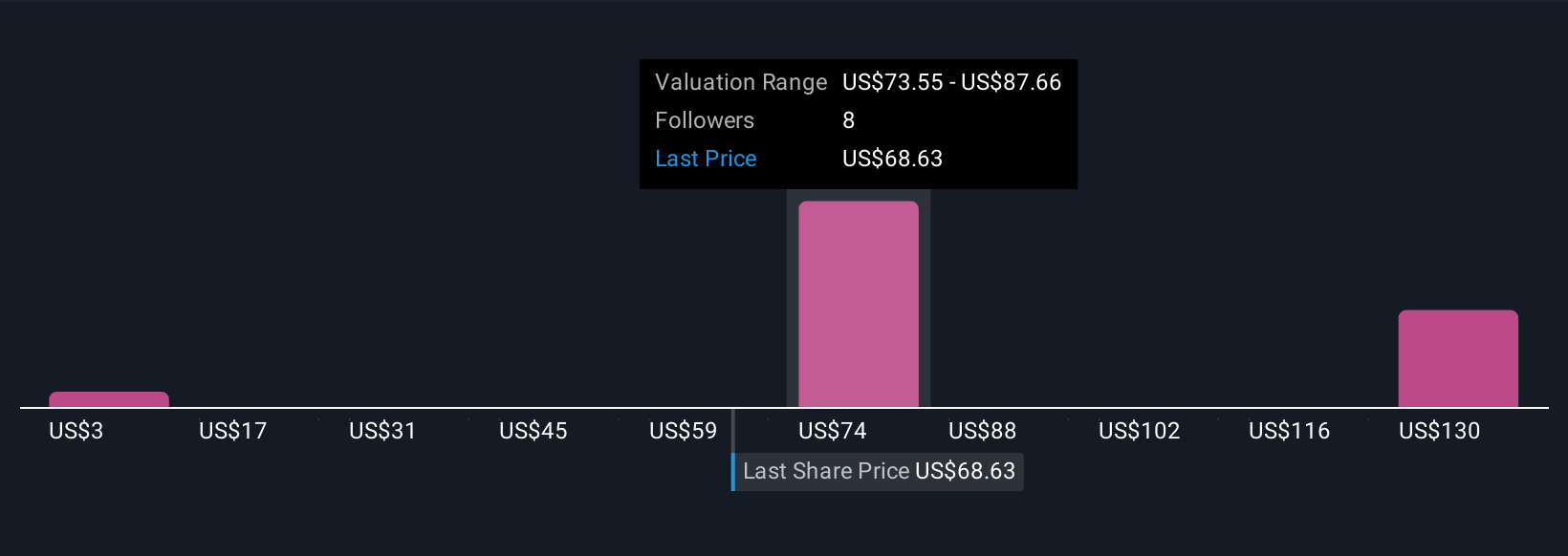

The Simply Wall St Community provides three individual fair value estimates for EchoStar, ranging from as low as US$2.98 to as high as US$40.36 per share. With consensus pointing to ongoing net losses, the company’s ability to stem negative cash flow may weigh heavily on future performance, reminding you how differently various market participants see the path forward.

Explore 3 other fair value estimates on EchoStar - why the stock might be worth as much as 50% more than the current price!

Build Your Own EchoStar Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your EchoStar research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free EchoStar research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EchoStar's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 19 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com