- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalThe S&P 500 is approaching a high point: should we buy US stocks and assets now?

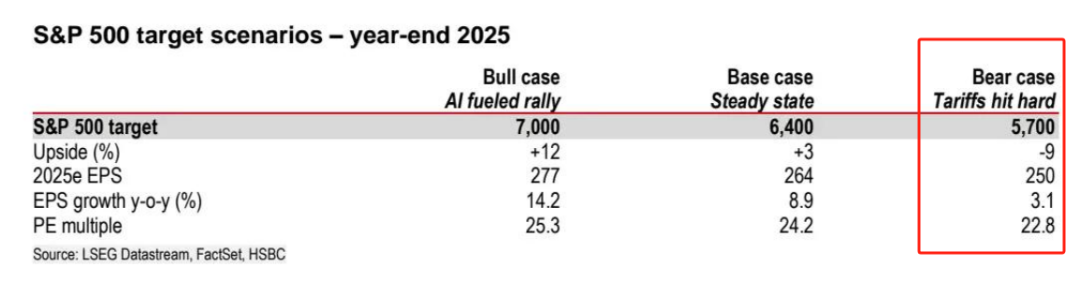

The Zhitong Finance App learned that when the S&P 500 index quietly approached an all-time high under the strong leadership of technology stocks, ordinary investors fell into collective hesitation. Whether to buy US stocks and assets at this time depends on investors' risk appetite and allocation strategy. From an institutional perspective, supporting factors still dominate: strong profitability resilience in technology stocks (UBS, HSBC, Barclays), marginal improvements in trade and policy uncertainty (Barclays, HSBC), and global capital reallocation biases against US dollar assets (Barclays, HSBC). Together, these factors form the basis for “cautious optimism.” HSBC raised the target level of the S&P 500 index to 6,400 points by the end of 2025, which may even reach 7,000 points in a bull market scenario, providing direction guidance for long-term investors.

However, risks also cannot be ignored. Profit differentiation requires investors to avoid sectors severely impacted by tariffs (energy, some consumer sectors) and focus on technology (especially artificial intelligence applications) and financial sectors; the lagging effects of tariffs remind investors to pay attention to changes in profit margins in the third quarter earnings report; and valuation concerns mean that it is not appropriate to blindly pursue higher levels, which can be gradually adjusted in the face of market adjustments.

For ordinary investors, instead of struggling with “whether to buy,” it is better to think about “how to buy”: select leaders with profits exceeding expectations within technology stocks (such as Meta and Amazon's top six TECH+ companies), pair them with financial stocks that benefit from policy easing, and control positions to cope with potential fluctuations. As the complex situation in the market shows, there is no absolute “do's and don'ts”, only “whether it is appropriate” that matches one's own risk tolerance. ,

I. Market Status: Structural Market Dominated by Technology Stocks

<pstyle="white-space: normal; word-spacing: 0px; text-transform: none; color: rgb (0,0,0); orphans: 2; widows: 2; margin: 5px0px; letter-spacing: normal; text-indent: 0px; -webkit-text-stroke-width: 0px; text -decoration-thickness: initial; text-decoration-style: initial; text-decoration-color: initial">

<pstyle="white-space: normal; word-spacing: 0px; text-transform: none; color: rgb (0,0,0); orphans :2; widows: 2; margin: 5px0px; letter-spacing: normal; text-indent: 0px; -webkit-text-stroke-width: 0px; text-decoration-thickness: initial; text-decoration-style: initial; text-decoration-color: initial">

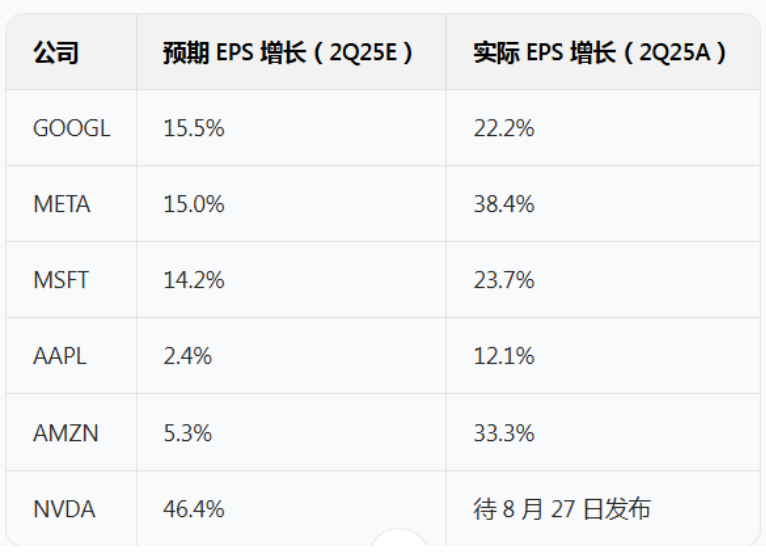

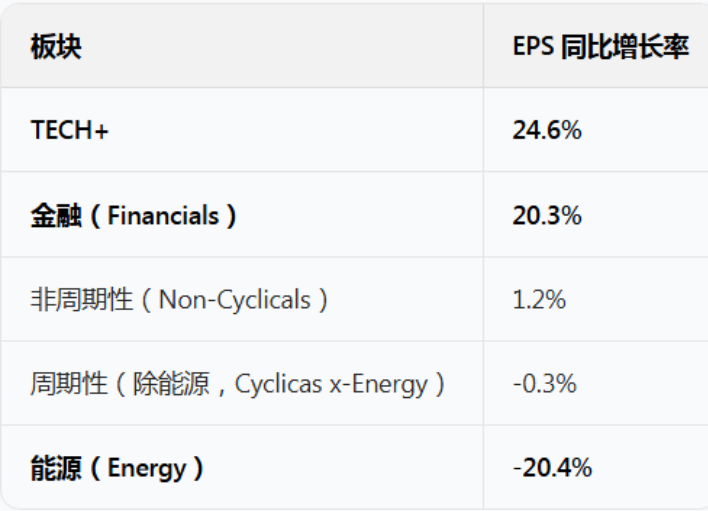

The current rise in the S&P 500 index is not an overall rise, but a structural market dominated by the technology sector. According to the 2Q25 US stock earnings report released by UBS on August 6, 2025, the market value of 76.9% of the S&P 500 index had released second-quarter earnings reports, and overall earnings per share (EPS) increased 10.2% year on year, far exceeding the initial 5% forecast. Among them, the TECH+ sector performed the most impressive. EPS increased 24.6% year on year, while the energy sector fell 20.4% year on year, in stark contrast. What is more noteworthy is that the overall EPS of the six major Tech+ companies (Google, Meta, Microsoft, Apple, Amazon, and Nvidia) increased 27.5% year over year, far exceeding the 5.9% growth rate of the rest of the market. Specifically, Meta's actual EPS grew by 38.4% (expected 15.0%), and Amazon actually grew by 33.3% (expected 5.3%). This “top student” level performance became the core driving force driving the S&P 500 index to approach historic highs.

</pstyle="white-space: normal; word-spacing: 0px; text-transform: none; color: rgb (0,0,0); orphans: 2; widows: 2; margin: 5px0px; letter-spacing: normal; text-indent: 0px; -webkit-text-stroke-width: 0px; text-decoration-thickness: initial; text-decoration-style: initial; text-decoration-color: initial">

</pstyle="white-space: normal; word-spacing: 0px; text-transform: none; color: rgb (0,0,0) ; orphans: 2; widows: 2; margin: 5px0px; letter-spacing: normal; text-indent: 0px; -webkit-text-stroke-width: 0px; text-decoration-thickness: initial; text-decoration-style: initial; text-decoration- Color: initial">

(Table source: UBS)

From a valuation perspective, Barclays's latest opinion points out that the historical premium of large technology stocks over the S&P 500 index is in the bottom quarter range, which means there is still room for upward growth in current valuations. Although the S&P 500 index (excluding large technology stocks) has closed the return gap with the European market since this year, the valuation of large US stocks is still in a downward position at the top of the 10-year observation data, and there have been no serious deviations.

II. The three core logics that support buying

(1) Corporate Profitability Resilience: Driven by the Dual Engine of Technology and Finance

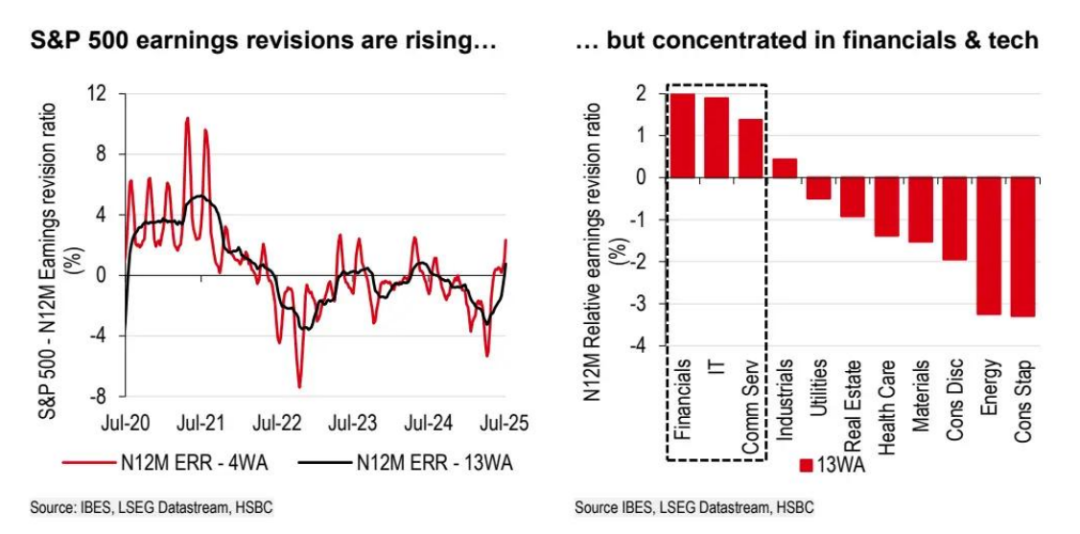

Corporate profit is the core cornerstone that supports stock prices. According to the HSBC Global Investment Research August 6, 2025 report, the S&P 500 EPS growth rate reached 10% in the second quarter, and the performance of more than two-thirds of companies was better than expected. Among them, more than 90% of individual stocks in the technology sector EPS exceeded expectations, and the performance of brokerage stocks in the financial sector also far exceeded expectations.

This profit resilience is not short-lived. According to UBS data, overall corporate profits for the quarter exceeded expectations by 8.1%, and 74% of the company's performance standards were met, while the historical average from the second quarter of 2020 to the second quarter of 2024 exceeded expectations by only 4.9%. The current profit performance is significantly superior to most of the past period.

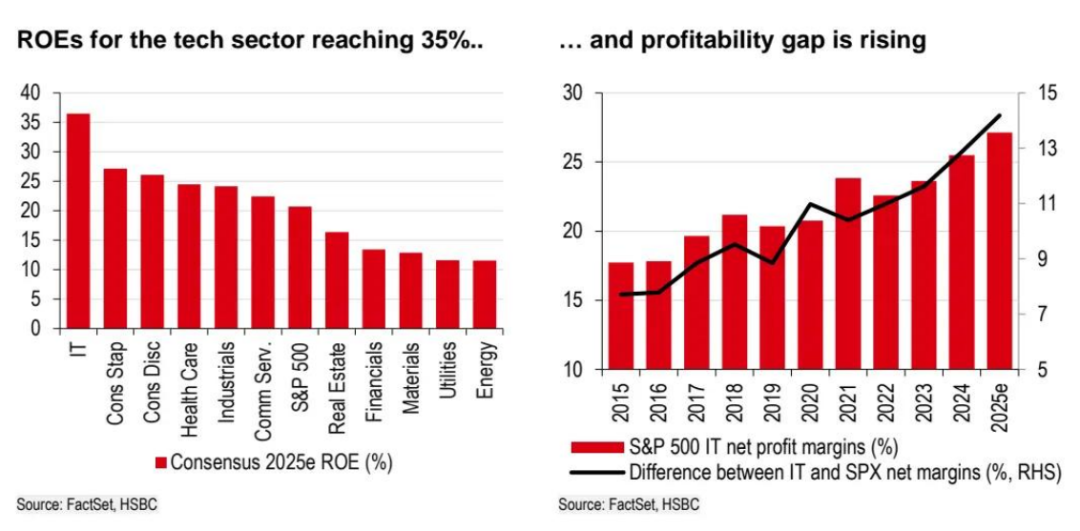

Earnings growth in the tech sector is particularly sustainable. According to HSBC, the profit growth rate of the technology sector is expected to reach about 20% in 2025, and the profit correction ratio is on the rise. Microsoft's artificial intelligence business continues to accelerate, and Meta was upgraded to a “buy” rating, high return on net assets (36%, 15 percentage points higher than the market average), strong balance sheet, and continued capital expenditure, further expanding its competitive advantage.

(Chart source: HSBC Global Investment Research, August 5, 2025)

Barclays also mentioned that the results of Google, Meta, and Microsoft for the second quarter of 2025 show that the growth momentum of large technology stocks, which are the main engines of profitability in the US stock market, has not been affected (Barclays).

(ii) Policy and trade environment: marginal improvement in uncertainty

The easing of trade uncertainty has provided important support for US assets. Barclays believes that the US has escaped the influence of “excessive reliance on large technology stocks and trade-related concerns”. Although tariff negotiations still exist, a series of agreements reached between the US government and global trading partners mark that the peak of trade uncertainty has passed.

This judgment was confirmed in the foreign exchange market: the US dollar index (DXY) stabilized after a record sell-off in the first half of 2025, and the decline against major G10 currencies narrowed over the past month, especially against the British pound and yen.

Although the pace of the Federal Reserve's policy shift is debatable, the benchmark scenario is biased towards moderation. HSBC's benchmark scenario assumes that the economic slowdown in the second half of 2025 will cause the Federal Reserve to start cutting interest rates (25 basis points each in September and December), which will provide liquidity support for the market. Despite the risk of “independence of the Federal Reserve,” Barclays pointed out that the surprise level of US economic data has improved compared to a month ago, and corporate profits have remained resilient, which provides buffer space for policy adjustments.

(3) Global capital reallocation: the attractiveness of US dollar assets has rebounded

Global capital flows are shifting back towards US assets. Barclays observed that commodity trading advisor (CTA) long positions in the British, Chinese, and Japanese stock markets are close to historical extremes, while the US stock market's exposure to sideways trading/rising markets may increase further, and there is still room for expansion in the allocation of volatility control strategies and risk parity strategies.

In the foreign exchange market, HSBC foreign exchange strategists believe that as the US reaches trade agreements with Japan and the EU, the euro may gradually fall to the 1.13 level against the US dollar, and the dollar may continue to rise from bottom, which will enhance the attractiveness of US dollar assets to global capital.

Judging from the position structure, both retail investors and institutions have room to increase their positions. Barclays mentioned that retail purchases have continued, while hedge funds/leveraged investors (HF/LO) still have room to increase their participation (Barclays). This trend of capital reallocation resonates with the expectation that the US “has the greatest room for upward profit margins in the world,” further strengthening the allocation value of US assets.

3. The root cause of hesitation: the three major risks cannot be ignored

(1) The diversification of corporate profits has intensified, and the non-technology sector is under pressure

The structural differentiation of profit growth is one of the core reasons investors are hesitant. According to UBS data, the difference in EPS growth between the S&P 500 sectors is extremely significant: the TECH+ sector grew 24.6%, while the energy sector fell 20.4%, the cyclical sector (excluding energy) fell 0.3%, and the non-cyclical sector grew by only 1.2%.

(Table source: UBS)

HSBC also pointed out that the profit growth and momentum of the S&P 500's “other sectors” (non-technology/non-top seven tech giants) is slowing down, and the essential consumer goods and non-essential consumer goods sectors affected by tariffs are facing negative earnings revisions and weak guidance.

(Chart source: HSBC Global Investment Research, August 5, 2025)

This differentiation means that buying “American assets” is not a simple overall decision, but requires precise stock selection.

(2) The lagging effects of tariff shocks may become critical in the third quarter

The impact of tariffs on corporate profits may be delayed.

HSBC warned that the current effective US tariff rate is about 18%, far higher than 2.5% at the beginning of the year. Although profit margins remained stable in the second quarter (13.2%), the third quarter may be more significantly impacted as inventory reduction and migration work progresses.

In a bear market scenario, tariffs may cause corporate profits to fall and inflation to rise, limit the Federal Reserve's interest rate cut, and cause the S&P 500 index to drop to 5,700 points. This potential risk makes investors doubt the sustainability of current valuations.

(Chart source: HSBC Global Investment Research, August 5, 2025)

(3) The psychological game between valuation and historical highs

Valuation concerns raised by the S&P 500 approaching an all-time high cannot be ignored. Although Barclays believes that the valuation of large US stocks has not seriously deviated from a reasonable range, HSBC points out that the expected price-earnings ratio for the next 12 months for the non-tech and non-“ Big Seven Tech” sectors is 18.5 times, which is 17.3 times higher than the five-year average, and there is limited room for revaluation.

For ordinary investors, the fear of “buying at a high point” has been amplified — although technology stocks have profit support, a price-earnings ratio of 29.6 times (HSBC data) is no longer cheap. Once the AI boom recedes or policies fall short of expectations, the risk of valuation pullbacks will rise.