Two new drug RWA revolutions in a week are disrupting the innovative drug industry. Why now?

Within a week, two new drug RWA revolutions are disrupting the innovative drug industry. Why now?

If the first time that China's innovative drugs were globalized was to “authorize innovative drugs to go overseas,” the second time it would be “putting R&D capabilities on the chain.”

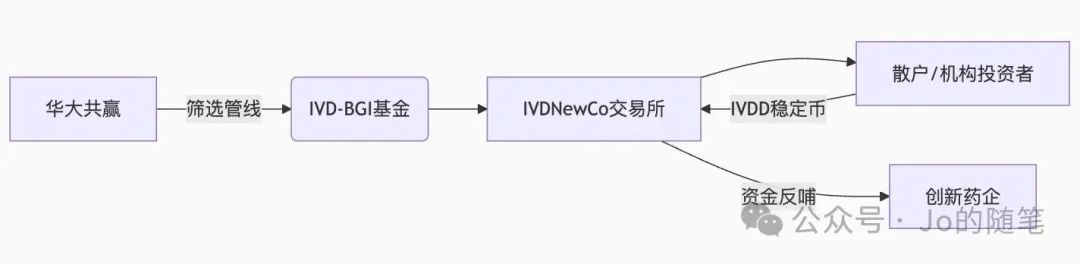

On July 31, Huajian Healthcare (01931, intraday +19.82%) announced the launch of the world's first IVD medical equipment RWA project, releasing 300 million dollars in liquidity by anchoring the ownership of 3,000 testing devices on the chain.

On August 4, Hanyu Pharmaceutical (300199.SZ, intraday +19.98%) teamed up with the crypto exchange KuCoin to explore the “future income rights” of new peptide drug pipelines such as GLP-1 and rare diseases as the underlying asset to launch China's first innovative drug RWA tokenization exploration in Hong Kong.

Within a week, two medical/pharmaceutical companies used the same key — RWA (Real World Assets) — to unlock the trillion-dollar liquidity shackles of pharmaceutical assets. While traditional license-outs are still raving about $12 billion in overseas transactions, a paradigm revolution from “authorized BD to go overseas” to “asset options to go overseas” has quietly broken out. China's innovative drugs can no longer only “authorize BD to go overseas,” but can also “go overseas as asset options.”

RWA × stablecoin: reconstructing the liquidity of pharmaceutical assets

RWA (Real World Assets): Uses blockchain technology to tokenize physical assets (such as real estate, bonds, equipment income rights) to enable on-chain transactions.

Stablecoin: A digital currency (such as USDT, USDC) that is anchored to fiat/gold, and acts as a payment medium and pricing unit for RWA transactions.

Relationship: Stablecoins are the “infrastructure” of RWA, providing stable pricing and cross-border settlement channels for high-risk pharmaceutical assets.

Case: Circle's USDC is backed by 100% US debt reserves to provide RWA with compliant payment tools, and its market capitalization surpassed 61 billion US dollars in 2025.

Market Size: Blockchain's New Multi-Trillion-Dollar Engine

Citi predicts that in 2030, the RWA market will reach 4.5 trillion US dollars (securities tokenization) + 1 trillion US dollars (trade finance).

Boston Advisory Report: The potential value of global RWA is 16 trillion US dollars, and the share of pharmaceutical R&D assets will rapidly increase.

Core driving forces: Insufficient liquidity of traditional assets (such as the long development cycle of innovative drugs or up to 10 years); blockchain enables asset fragmentation and 7×24 hour transactions.

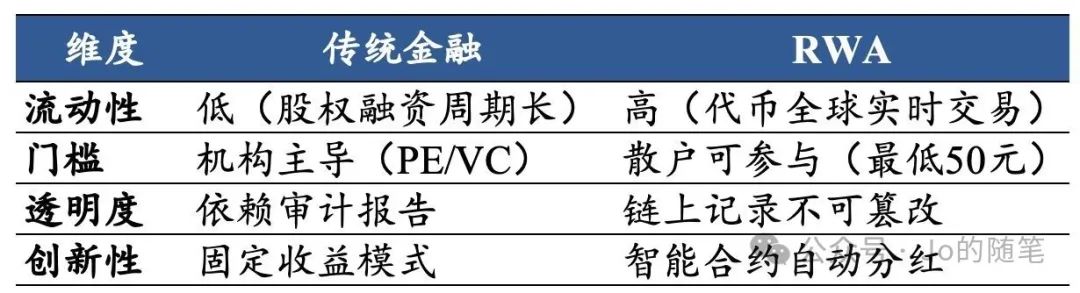

Differences between RWA and traditional finance

Example: GCL Nengke's RWA raised 200 million yuan for photovoltaic power plants. Investors subscribe to power plant revenue rights tokens through stablecoins, and T+0 settlement.

Classic cases at home and abroad: the leap from new energy to medicine

RWA's core value for innovative medicines

1) Solve the difficulties of going out to sea

Pain points of the traditional BD model:

Valuation discounts (overpricing by overseas pharmaceutical companies);

Long cycle time (license-out average 18 months);

Risk concentration (clinical failure leads to termination of cooperation).

RWA Solution:

Asset optionalization: splitting future earnings from the R&D pipeline into tokens, and global investors subscribe in segments;

Risk diversification: retail investors share R&D risks and reduce the probability of single agency thunderstorms.

2) Restructure financing logic

From “selling off interests” to “selling expected profits”: retaining ownership of IP and anchoring the right to income;

From “reliance on PE” to direct access to global capital: KuCoin connects Hanyu with 41 million cross-border investors.

In 2024, China's innovative drug license-out reached US$51.9 billion. If 10% were converted to RWA financing, it would release more than US$5 billion in liquidity.

Why is the new drug RWA now? The triple resonance of policy, capital, and technology

1) Policy inflection point: the formation of a global regulatory framework

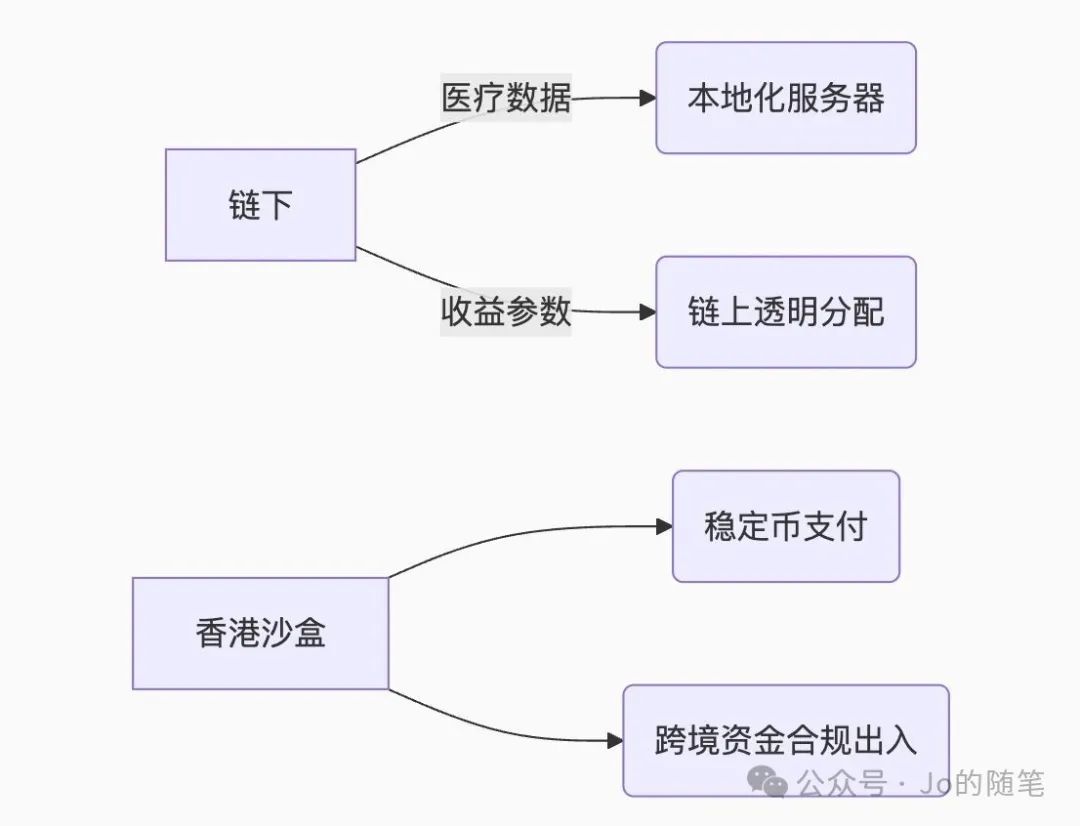

Hong Kong policy: The Stablecoin Ordinance came into effect on August 1, providing a compliance anchor and allowing pharmaceutical RWA sandbox testing;

US Act: The “GENIUS Act” was passed in June. US stablecoins are bound to US bonds, and funds are being sought for new targets;

Technology maturity: AntChain issued the “RWA On-Chain Technical Specification”, and the pharmaceutical data desensitization on-chain solution was implemented;

Capital thirst: The world's low liquidity assets amount to $260 trillion, and capital is pouring into the high-yield innovative drug RWA.

2) Capital demand: release of trillion-level liquidity

Boston Consulting predicts that by 2030, the global RWA market will reach US$16.1 trillion, accounting for more than 20% of healthcare assets. Currently, only 0.1% of pharmaceutical assets are tokenized, and there is huge room for growth.

3) Mature technology: perfect Web3 infrastructure

Smart contracts: automatically distribute profits (such as dividends to coin holders after the drug is marketed);

Oracle network: Off-chain medical data (such as clinical trial results) is securely on-chain to resolve information asymmetry.

4) Ecological collaboration: pharmaceutical companies+exchanges+VC new alliances

Huajian medical model:

Form a closed loop of “asset screening - token issuance - liquidity supply - R&D re-investment”.

Five core pain points of innovative pharmaceutical companies

1) Long capital deposition cycle and exhaustion of liquidity

The average development cycle for an innovative drug is 10 years, and 80% of the capital is consumed in the clinical stage (especially phase II/III), but assets cannot be circulated and monetized at this stage, causing the company to “lose blood” over a long period of time.

Traditional financing relies on PE/VC, but in 2025, the H1 healthcare sector IPO raised only 18 billion yuan, which is far from meeting demand.

2) The dilemma of valuation discounts and transfer of rights

Although license-out (external licensing) brought an annual transaction scale of 51.9 billion US dollars (2024), the down payment accounted for a low share of the down payment and required the transfer of global rights; some were sold to the US “second-hand dealer” shell company, commonly known in the industry, and finally, the listed shell company authorized a second time to major multinational pharmaceutical companies with milestone income rights.

3) The investment threshold is high, and retail capital is excluded

The financing of an innovative drug project alone requires tens of millions of dollars. Only institutions can participate, and ordinary investors cannot share the high growth dividends.

4) Highly concentrated risk

The clinical failure rate is over 90% (phase I to listing), and the failure of a single pipeline may directly cause Biotech to go bankrupt.

5) Inefficient globalization

Cross-border capital flows are limited by foreign exchange controls and high compliance costs, making it difficult for China's innovative drugs to reach European and American retail investors and special funds

Preliminary study on the implementation path of innovative drug RWA

1) Anchored design: three types of pharmaceutical assets are preferred

R&D pipeline revenue rights (Hanyu model): tokens are graded according to clinical stage (for example, phase I/phase III tokens have different risk premiums);

Ownership of equipment (China inspection model): confirmation of on-chain ownership of testing equipment, tokenization of rental income;

Right to use data assets: desensitization clinical data pool (such as Malu Gru data assets increase by 3 million yuan per year).

2) Frame design

Key avoidance: Exclude sensitive data such as human genetic resources

Risks and Prospects: From “Making Dreams” to “Building Roads”

Challenge:

Regulatory dynamics (the Hong Kong Monetary Authority needs to refine pharmaceutical RWA rules);

the complexity of estimating new drugs (probability of clinical failure requires quantitative modeling);

Technical security (preventing hackers from attacking smart contracts).

Countermeasures:

Adopt Ondo Finance tiered tokens (high risk and high return);

Cooperate with a Hong Kong licensed trusteeship agency.

Outlook:

If pharmaceutical RWA runs through, China's 3000+ clinical pipeline can release trillion-level sleeping assets and promote the upgrading of innovative drugs from “going overseas with a single product” to global export of R&D capabilities.

Conclusion: R&D capacity on the chain, the second globalization of Chinese medicine

Innovative drug RWA is not a technical gimmick, but rather a restructuring of the “capital-development-market” relationship. When Huajian Medical's IVDD stablecoin flows through the Hong Kong Exchange, Dang Hanyu Pharmaceutical teamed up with KuCoin to announce the launch of China's first innovative drug RWA tokenization exploration in Hong Kong using the GLP-1 new peptide drug pipeline as the underlying asset - Chinese pharmaceutical people finally bid farewell to the BD era of “making a wedding dress for foreign investors” and move into a new era of global pricing power for R&D assets, and sit side by side with multinational giants!

This article is reprinted from the “Jo's Essay” official account, Zhitong Finance Editor: Jiang Yuanhua.