- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalBritish American Tobacco (LSE:BATS) Reports GBP 4,512M Income with Revenue Growth Expectations

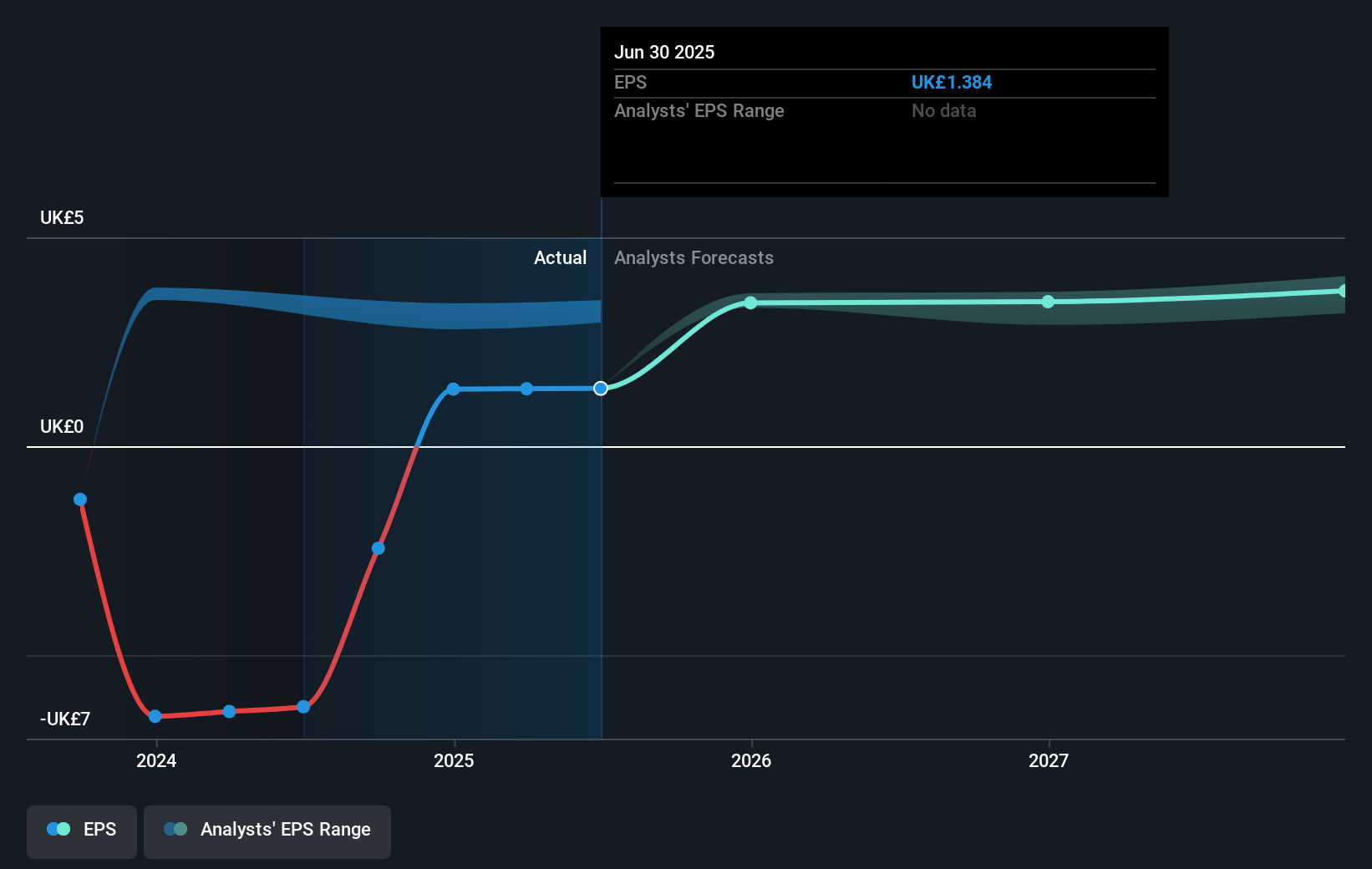

British American Tobacco (LSE:BATS) recently reported steady performance in its half-year earnings, with a slight dip in sales but stable net income. The company also confirmed its full-year guidance, anticipating revenue growth at the higher end of expectations. This positive outlook coincided with a 25% rise in its stock over the last quarter, possibly bolstered by the expanded buyback plan and sales performance of new product categories. Despite broader market downturns, such as tariff-induced investor concerns and weaker jobs data, British American Tobacco's strategic corporate actions likely contributed to buoyant investor sentiment.

British American Tobacco's recent performance and optimistic outlook, as explored in the introduction, highlight its resilience amid challenging market conditions. Over the past five years, the company's total return, including share price and dividends, was 138.77%, illustrating robust long-term shareholder value. In comparison, over the past year, the company's stock performance exceeded the UK Tobacco industry, which returned 40.9%. This strong performance may reflect investor confidence in BAT's innovative product strategies and operational efficiency improvements. Despite broader market headwinds, the company's share price ascent in the last quarter suggests positive investor sentiment fueled by expanded buybacks and anticipated revenue growth from new categories.

The impact of recent developments on British American Tobacco's revenue and earnings forecasts is significant. The expansion in new categories and investments in innovation such as glo Hyper Pro and Velo+ are expected to boost future revenue growth. Operational efficiencies and focus on the U.S. market further underpin profit margin enhancement expectations. Analysts forecast earnings to reach £7.9 billion by 2028, a surge from current levels, supporting optimistic future growth assumptions.

Despite trading at a slight premium to the analyst consensus price target of £39.0, the current share price of £40.40 reflects investor confidence in the company's future trajectory. The small share price discount to the target underscores varying analyst perspectives on BAT's valuation. It highlights the importance of individual assessment of the company's potential, given its ambitious revenue and earnings targets amidst ongoing industry challenges and regulatory risks. Thus, investors may want to critically evaluate whether recent operational and market developments align with long-term growth expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com