Traditional life insurance is gradually declining, and dividend insurance is taking over? UBS analyzes new trends in China's insurance industry

The Zhitong Finance App learned that UBS released a research report on July 25, focusing on developments in China's insurance industry. The article points out that the China Insurance Industry Association lowered the pricing interest rate benchmark. This adjustment may mark the end of the golden age of traditional incremental whole life insurance, and dividend insurance products are expected to usher in development opportunities. At the same time, the report analyzes the winning factors and potential winners of insurance companies in the field of dividend insurance in the context of industry transformation, providing a key perspective for understanding recent changes and trends in the Chinese insurance industry.

The pricing interest rate benchmark fell 14 basis points month-on-month to 1.99%, triggering a reduction in pricing interest rates

The China Insurance Industry Association lowered the fixed interest rate (PIR) benchmark by 14 basis points month-on-month to 1.99% (First Finance), which is 51 basis points lower than the current pricing rate of 2.5% for traditional products.

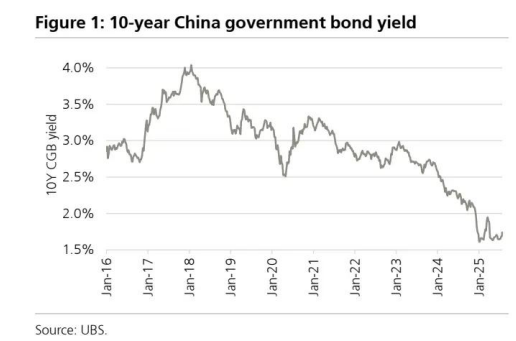

Given the decline in market interest rates (such as treasury bond yields, deposit interest rates, and loan market quoted interest rates) in the second quarter, the current price interest rate benchmark reduction is likely to be within market expectations. Major insurance companies announced that they will reduce the pricing interest rates for traditional, dividend (PAR), and universal products by 50 basis points, 25 basis points, and 50 basis points, respectively, to 2.0%, 1.75%, and 1.0%.

The gap in pricing interest rates between traditional products and dividend products has narrowed, indicating that the direction of supervision is shifting the focus to dividend insurance contracts to mitigate the risk of interest differences and losses. Product transformation work will be completed by the end of August.

Traditional incremental whole life insurance has come to an end, and dividend insurance products have appeared

This reduction in pricing interest rates may herald the end of the golden age of traditional incremental whole life insurance (IWLP). Although there is strong consumer demand for this product, there is a high interest rate risk for insurance companies.

In contrast, whether it is the Hong Kong market (that is, a demonstration return of 6% to 6.5%) or the mainland market, the appeal of dividend insurance products should increase. Traditional insurance policies with a pricing rate of 2.0% give policyholders an internal rate of return (IRR) of 1.6%-1.9% (UBS estimates), and some consumers may be unwilling to lock in such a yield for a long period of time (e.g. 10 years or more). The pricing interest rate for dividend insurance contracts is only 25 basis points lower than the traditional type (previously 50 basis points), and there is an upward opportunity through the variable income portion.

UBS estimates that the interest rate sensitivity of new business value (VNB) will decrease significantly in the first half of 2025 as most insurance companies have accelerated their transition to dividend insurance. Product portfolios that prefer dividend insurance will also increase the allocation of equity assets such as stocks, because dividend insurance accounts often have higher risk tolerance (that is, there is room to invest in risky assets).

Winning Factors: Investment+ Distribution Capability, and Rapid Dividend Insurance Transition

In June 2025, the China Financial Supervisory Administration issued the “Regulatory Guidelines on Dividend Allocation of Dividend Insurance Policies”, which replaced the rigid upper limit of 3% to 3.2% return on dividend insurance products with a principled framework. Financially sound insurance companies are allowed to provide policyholders with more competitive dividend insurance dividend yields. According to the guideline, key leverage to break through the dividend insurance dividend limit includes:

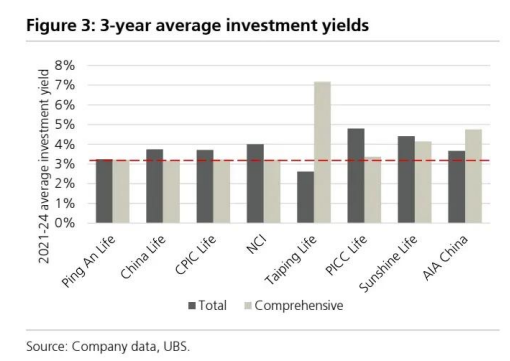

(1) The 3-year average comprehensive return on investment was higher than the industry average (3.2% in total; see Figure 1)

(2) The regulatory rating is 1-3;

(3) The dividend insurance account has been in existence for more than 3 years;

(4) The balance of the special reserve for dividends is positive. In addition to these standards, insurers with stronger fulfillment rates, distribution capabilities, and a faster shift to dividend insurance products may also gain a competitive advantage.

Potential winners in the dividend insurance sector

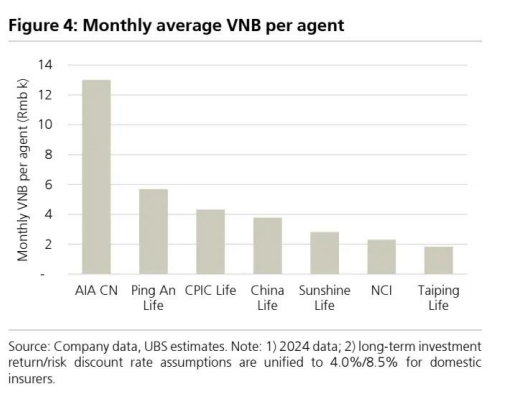

UBS believes that AIA China (01299, AIA China) is in an advantageous position to seize dividend insurance opportunities because it has relatively strong investment capacity (the average comprehensive return on investment in 2021-24 was 4.8%; compared to the average 4% of listed life insurance peers), fulfillment rate, and agency productivity (the value of each agent's new business per month in 2024 was 13,000 yuan; the same transaction as listing was 1,800-5,700 yuan).

AIA China also began dividend insurance transformation earlier. In the first quarter of 2025, dividend insurance products contributed more than 80% of the value of the new long-term savings business through agency channels. Based on the criteria in the “winning factors” section above, Ping An Life and China Life Insurance also performed better than their peers.

Figure 1: China 10-year Treasury Bond Yield

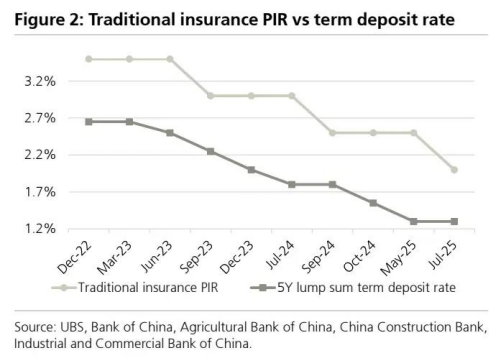

Figure 2: Traditional Insurance Pricing Rates vs. Time Deposit Rates

Figure 3:3-year average return on investment

Figure 4: Average monthly new business value per agent