European Market Highlights: 3 Stocks That May Be Trading Below Estimated Value

As the European markets experience mixed returns, with the pan-European STOXX Europe 600 Index remaining relatively flat and major indices showing varied performance, investors are keenly observing economic indicators such as inflation rates and labor market stability. In this environment, identifying stocks that may be trading below their estimated value can offer potential opportunities for those looking to capitalize on discrepancies between market price and intrinsic value.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Sulzer (SWX:SUN) | CHF142.00 | CHF277.82 | 48.9% |

| SNGN Romgaz (BVB:SNG) | RON6.74 | RON13.17 | 48.8% |

| QPR Software Oyj (HLSE:QPR1V) | €0.822 | €1.62 | 49.3% |

| innoscripta (XTRA:1INN) | €100.20 | €195.81 | 48.8% |

| Hybrid Software Group (ENXTBR:HYSG) | €3.54 | €6.96 | 49.1% |

| Green Oleo (BIT:GRN) | €0.795 | €1.58 | 49.6% |

| cyan (XTRA:CYR) | €2.20 | €4.39 | 49.9% |

| Cambi (OB:CAMBI) | NOK21.70 | NOK43.04 | 49.6% |

| Apotea (OM:APOTEA) | SEK87.70 | SEK173.54 | 49.5% |

| Almirall (BME:ALM) | €10.68 | €21.21 | 49.6% |

Below we spotlight a couple of our favorites from our exclusive screener.

Tikehau Capital (ENXTPA:TKO)

Overview: Tikehau Capital is an alternative asset management group with €46.1 billion in assets under management and a market capitalization of approximately €3.34 billion.

Operations: The company's revenue is derived from Investment Activities amounting to €207.07 million and Asset Management Activities totaling €350.70 million.

Estimated Discount To Fair Value: 31.7%

Tikehau Capital appears undervalued, trading 31.7% below its estimated fair value of €28.33, with earnings forecasted to grow significantly at 36.15% annually, outpacing the French market's growth rate. However, its dividend yield of 4.14% is not well-covered by earnings or free cash flows. Recent strategic initiatives include a partnership to launch a €150 million private equity fund focused on defense and cybersecurity sectors in Europe, enhancing its investment appeal in strategic industries.

- Insights from our recent growth report point to a promising forecast for Tikehau Capital's business outlook.

- Take a closer look at Tikehau Capital's balance sheet health here in our report.

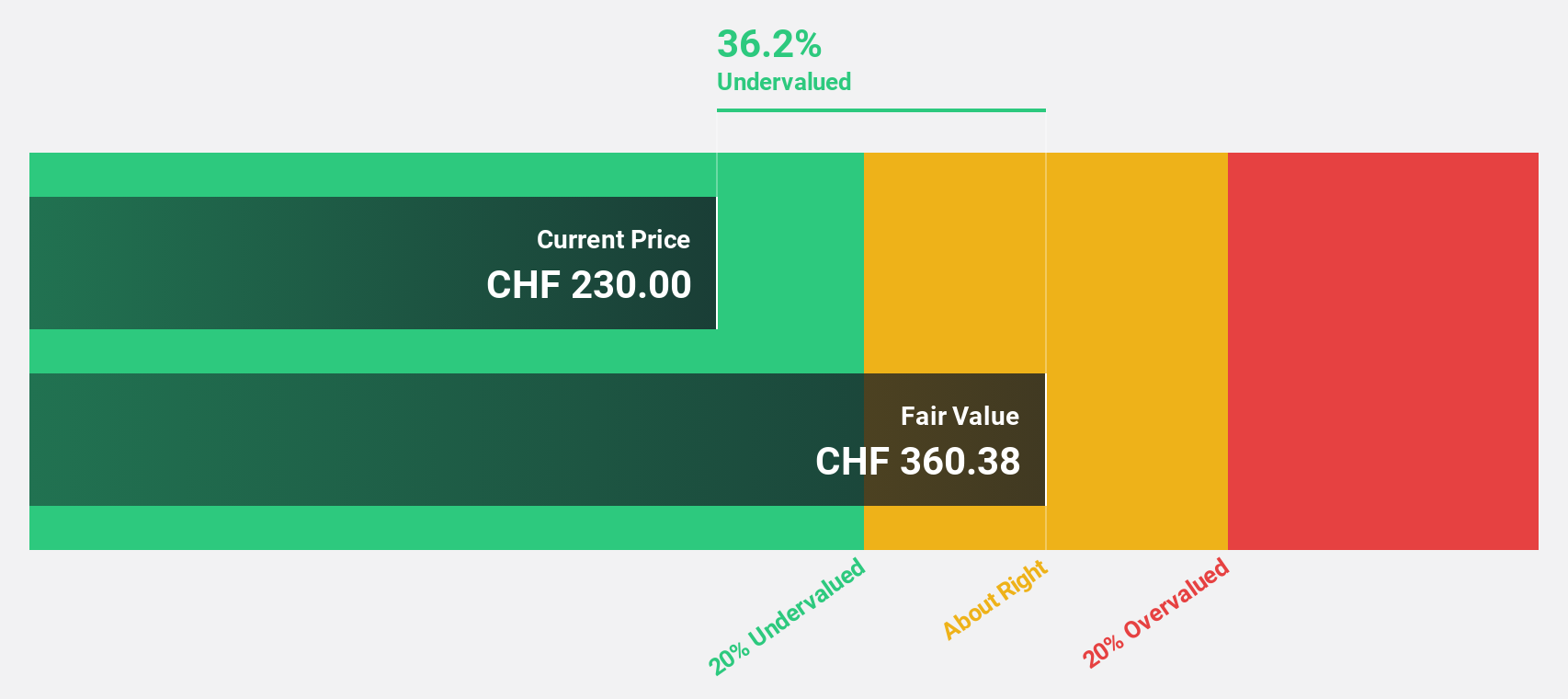

Comet Holding (SWX:COTN)

Overview: Comet Holding AG, with a market cap of CHF2.07 billion, operates globally through its subsidiaries to deliver X-ray and radio frequency power technology solutions across Europe, North America, Asia, and other international markets.

Operations: Comet Holding AG generates revenue through its X-Ray Systems (CHF115.89 million), Industrial X-Ray Modules (CHF94.57 million), and Plasma Control Technologies (CHF247.39 million) segments.

Estimated Discount To Fair Value: 28.6%

Comet Holding is trading at CHF266.8, significantly below its fair value estimate of CHF373.72, and earnings are expected to grow substantially at 31.4% annually, outpacing the Swiss market's growth rate. Recent first-quarter sales surged by 37.5% year-over-year to CHF111.2 million, reflecting strong operational performance. Despite a slower revenue growth forecast of 12.6%, Comet remains undervalued based on discounted cash flow analysis and offers potential for appreciation amidst strategic leadership changes.

- In light of our recent growth report, it seems possible that Comet Holding's financial performance will exceed current levels.

- Get an in-depth perspective on Comet Holding's balance sheet by reading our health report here.

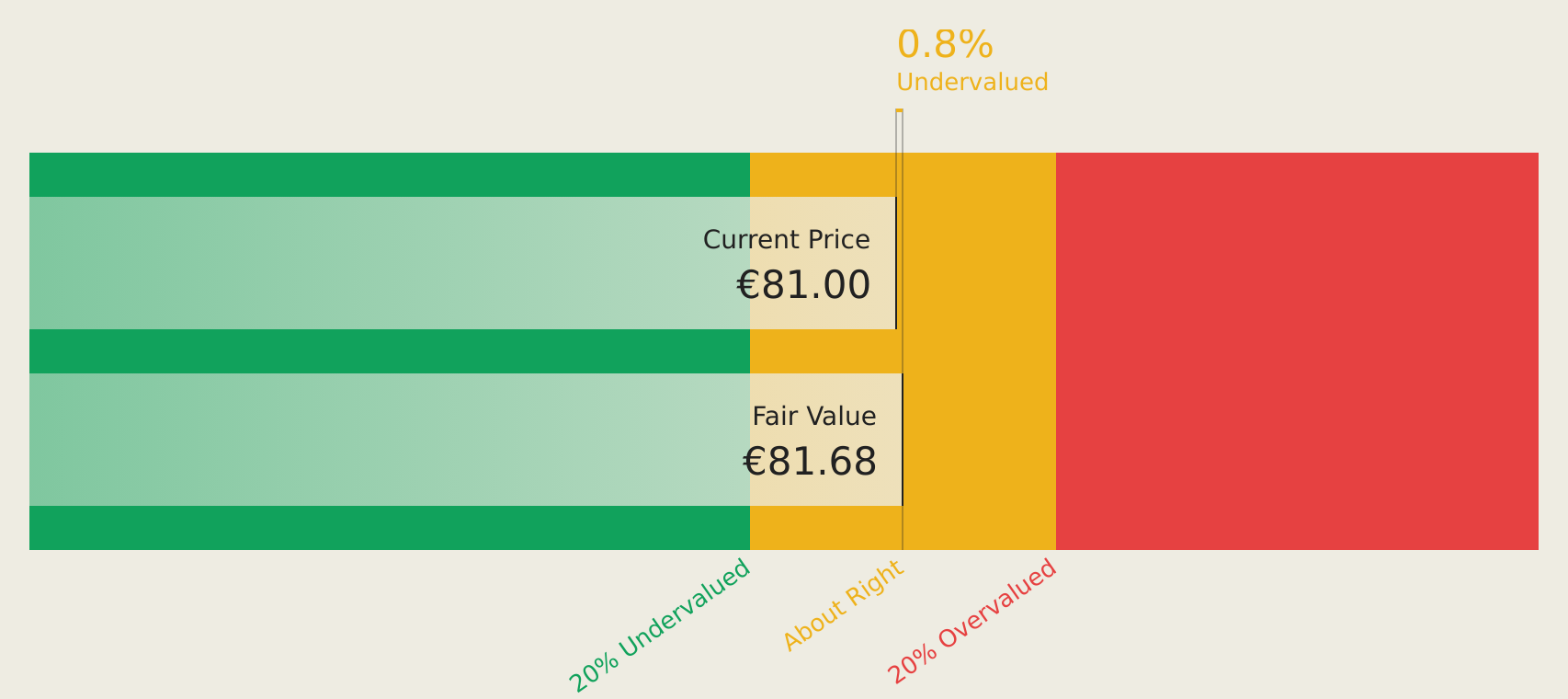

PFISTERER Holding (XTRA:PFSE)

Overview: PFISTERER Holding SE manufactures and sells cable fittings, insulators for overhead lines, and associated components for energy networks and renewable energy generation, with a market cap of €796.40 million.

Operations: The company's revenue segments are composed of Components (€100.70 million), Overhead Lines (€78.59 million), High Voltage Cable Accessories (€149.68 million), and Medium Voltage Cable Accessories (€52.72 million).

Estimated Discount To Fair Value: 40.4%

PFISTERER Holding SE is trading at €44, well below its estimated fair value of €73.8, indicating it is undervalued based on discounted cash flow analysis. The company's earnings are projected to grow 17.88% annually, surpassing the German market's average growth rate of 16.5%. Following a recent IPO raising €167 million, PFISTERER plans to use proceeds for strategic acquisitions and capacity expansion, enhancing its potential for future cash flow generation and value appreciation.

- Our earnings growth report unveils the potential for significant increases in PFISTERER Holding's future results.

- Click here and access our complete balance sheet health report to understand the dynamics of PFISTERER Holding.

Where To Now?

- Click this link to deep-dive into the 181 companies within our Undervalued European Stocks Based On Cash Flows screener.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com