- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalFerric Collaboration Enhances Power Solutions for Marvell Technology (NasdaqGS:MRVL) AI Platforms

Marvell Technology (NasdaqGS:MRVL) recently collaborated with Ferric, Inc. to advance integrated power solutions, aiming to optimize AI and cloud infrastructure. This strategic alliance coincided with a notable 25% increase in Marvell's stock price over the past month, a movement significantly above the market's general upward trend of 1.7%. While the Ferric partnership likely contributed to this surge, other factors such as earnings growth and executive changes may have also had an impact. These developments added weight to Marvell's strong performance and distinguished it from broader market gains.

The recent collaboration between Marvell Technology and Ferric, Inc. is expected to significantly bolster Marvell's position in the AI and cloud infrastructure markets. Given the strong AI demand and the company's plans to ramp up custom AI silicon production, this partnership could enhance Marvell's revenue, aligning with its strategic initiatives to introduce advanced technologies. The new developments, such as co-packaged optics, are projected to improve margins and drive future earnings growth. Despite these positive prospects, the company's reliance on certain markets and customers introduces risks that could impact its long-term profitability.

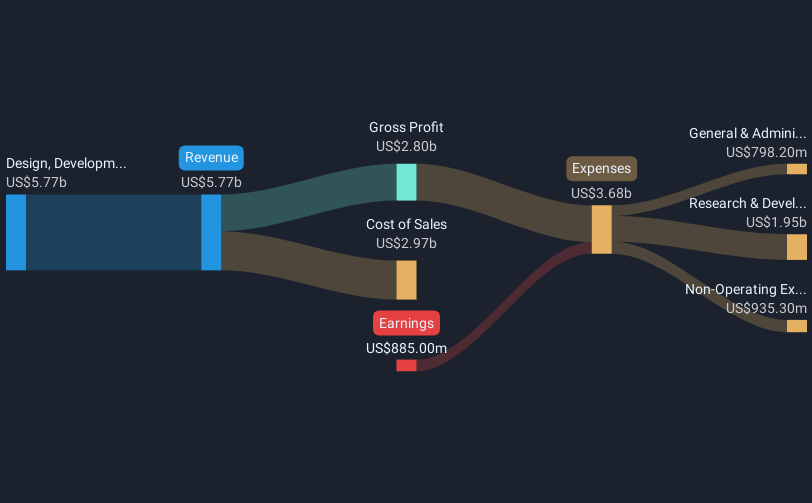

Over the past five years, Marvell's total shareholder return, including dividends, reached 125.86%. This performance highlights the company's long-term growth capacity, outperforming the broader semiconductor industry over the past year, where Marvell underperformed the industry's 15.4% return. Nevertheless, its share price, currently at US$61.22, reflects a significant discount to the consensus analyst price target of US$103.36, suggesting potential upside if the company meets future growth projections.

The partnership and ongoing technological advancements are crucial factors that analysts consider in their revenue and earnings forecasts. Marvell's revenue is anticipated to grow by 16.5% annually, and earnings are expected to transition to positive figures within the next three years. However, these forecasts hinge on successful execution of its product enhancements and market strategies. While the current share price stands substantially below analyst targets, it remains essential for investors to evaluate the involved risks, such as inventory management and dependency on key customers, when considering future performance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com