UK's June 2025 Stock Picks Estimated Below Intrinsic Value

The United Kingdom's stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China, highlighting concerns over global economic recovery. As investors navigate these turbulent times, identifying undervalued stocks becomes crucial; such stocks may offer potential opportunities by trading below their intrinsic value amidst broader market uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Vistry Group (LSE:VTY) | £6.258 | £10.78 | 41.9% |

| LSL Property Services (LSE:LSL) | £3.14 | £5.64 | 44.4% |

| Jubilee Metals Group (AIM:JLP) | £0.035 | £0.065 | 45.9% |

| Informa (LSE:INF) | £8.086 | £14.49 | 44.2% |

| Huddled Group (AIM:HUD) | £0.035 | £0.06 | 41.4% |

| Hostelworld Group (LSE:HSW) | £1.365 | £2.60 | 47.5% |

| Gooch & Housego (AIM:GHH) | £6.00 | £10.56 | 43.2% |

| Franchise Brands (AIM:FRAN) | £1.48 | £2.56 | 42.3% |

| Deliveroo (LSE:ROO) | £1.758 | £3.06 | 42.5% |

| AstraZeneca (LSE:AZN) | £102.48 | £178.94 | 42.7% |

Here's a peek at a few of the choices from the screener.

CVS Group (AIM:CVSG)

Overview: CVS Group plc operates in the veterinary, pet crematoria, online pharmacy, and retail sectors with a market cap of £905.36 million.

Operations: The company's revenue is primarily derived from its Veterinary Practices (£600.50 million), Online Retail Business (£48.50 million), Laboratories (£30.90 million), and Crematoria (£12.20 million) segments.

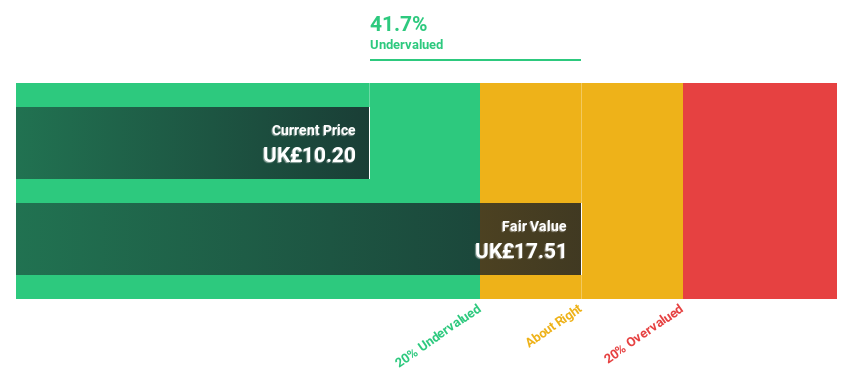

Estimated Discount To Fair Value: 31.4%

CVS Group is trading at £12.62, significantly below its estimated fair value of £18.4, suggesting it is undervalued based on discounted cash flow analysis. Analysts predict a 21.5% stock price increase and expect earnings to grow annually by 21.1%, outpacing the UK market's 13.8%. However, interest payments are not well covered by earnings, and profit margins have declined from 7.3% to 2.9% over the past year.

- The analysis detailed in our CVS Group growth report hints at robust future financial performance.

- Take a closer look at CVS Group's balance sheet health here in our report.

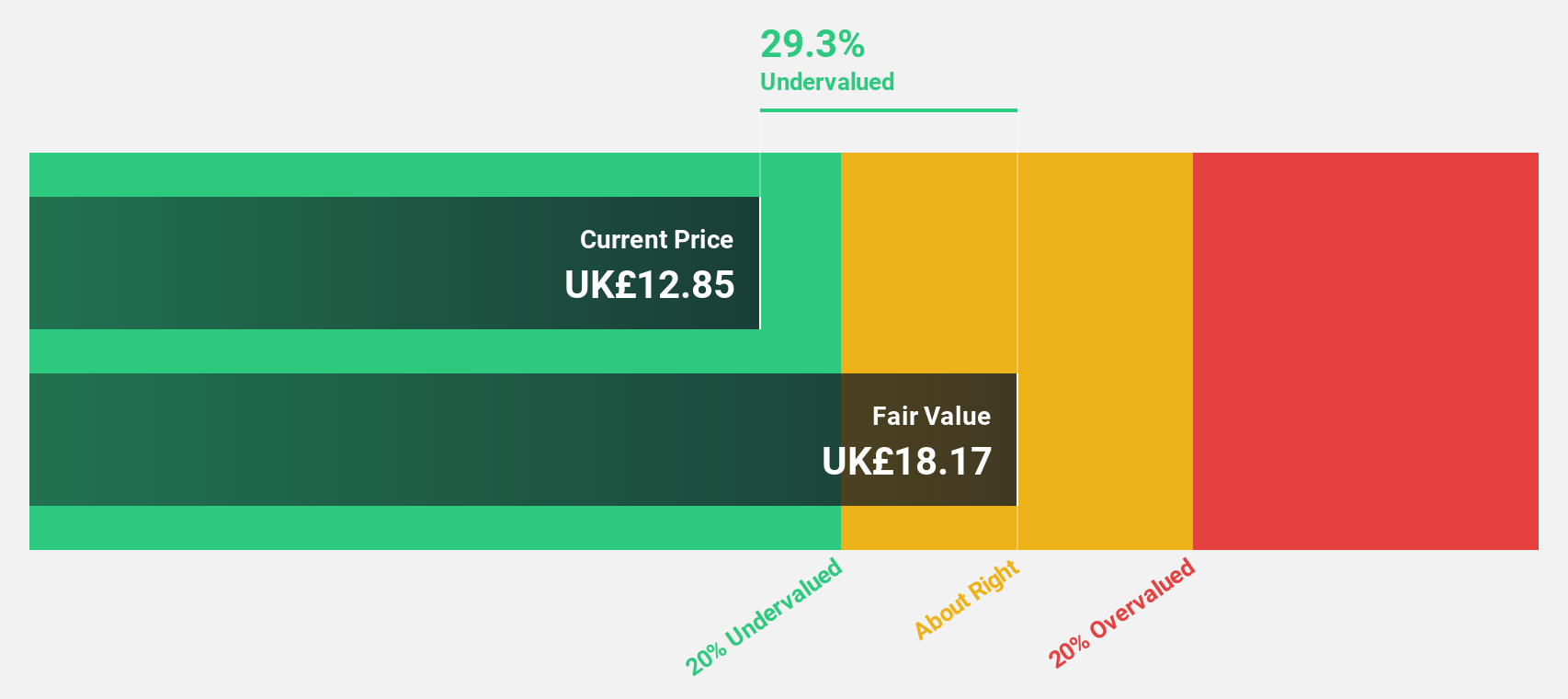

Nichols (AIM:NICL)

Overview: Nichols plc, with a market cap of £506.49 million, supplies soft drinks to the retail, wholesale, catering, licensed, and leisure industries in the United Kingdom and internationally including the Middle East and Africa.

Operations: The company's revenue is derived from two main segments: Packaged, generating £132.82 million, and Out of Home, contributing £39.99 million.

Estimated Discount To Fair Value: 23.7%

Nichols plc, trading at £13.85, is undervalued by over 20% against its estimated fair value of £18.15 based on discounted cash flow analysis. Despite a slower forecasted revenue growth of 3.9% annually compared to the broader market, Nichols' earnings are expected to grow faster than the UK average at 14.8% per year. Recent trading results show stable performance with strategic shifts in international operations and limited exposure to global tariff changes, supporting continued profitable growth ambitions.

- According our earnings growth report, there's an indication that Nichols might be ready to expand.

- Unlock comprehensive insights into our analysis of Nichols stock in this financial health report.

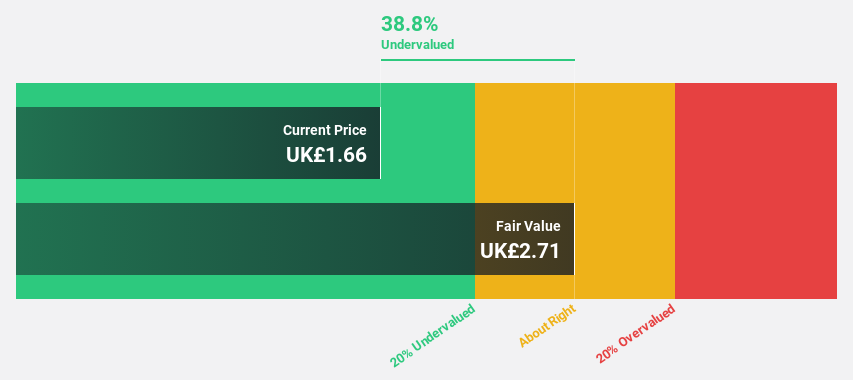

SSP Group (LSE:SSPG)

Overview: SSP Group plc operates food and beverage outlets across various regions including North America, Europe, the UK, Ireland, Asia Pacific, Eastern Europe, and the Middle East with a market cap of approximately £1.35 billion.

Operations: The company's revenue primarily comes from its food and beverage travel sector, mainly at airports and railway stations, amounting to £3.58 billion.

Estimated Discount To Fair Value: 37.6%

SSP Group, trading at £1.68, is significantly undervalued with a fair value estimate of £2.70 based on discounted cash flow analysis. Despite reporting a net loss of £61.5 million for H1 2025, SSP's earnings are forecast to grow substantially by 57.53% annually and the company is expected to become profitable in three years. The stock also trades at good value relative to peers and industry standards, highlighting its potential as an undervalued opportunity.

- Our expertly prepared growth report on SSP Group implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of SSP Group here with our thorough financial health report.

Next Steps

- Access the full spectrum of 49 Undervalued UK Stocks Based On Cash Flows by clicking on this link.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com