- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalMiquel y Costas & Miquel's (BME:MCM) Dividend Will Be Increased To €0.1063

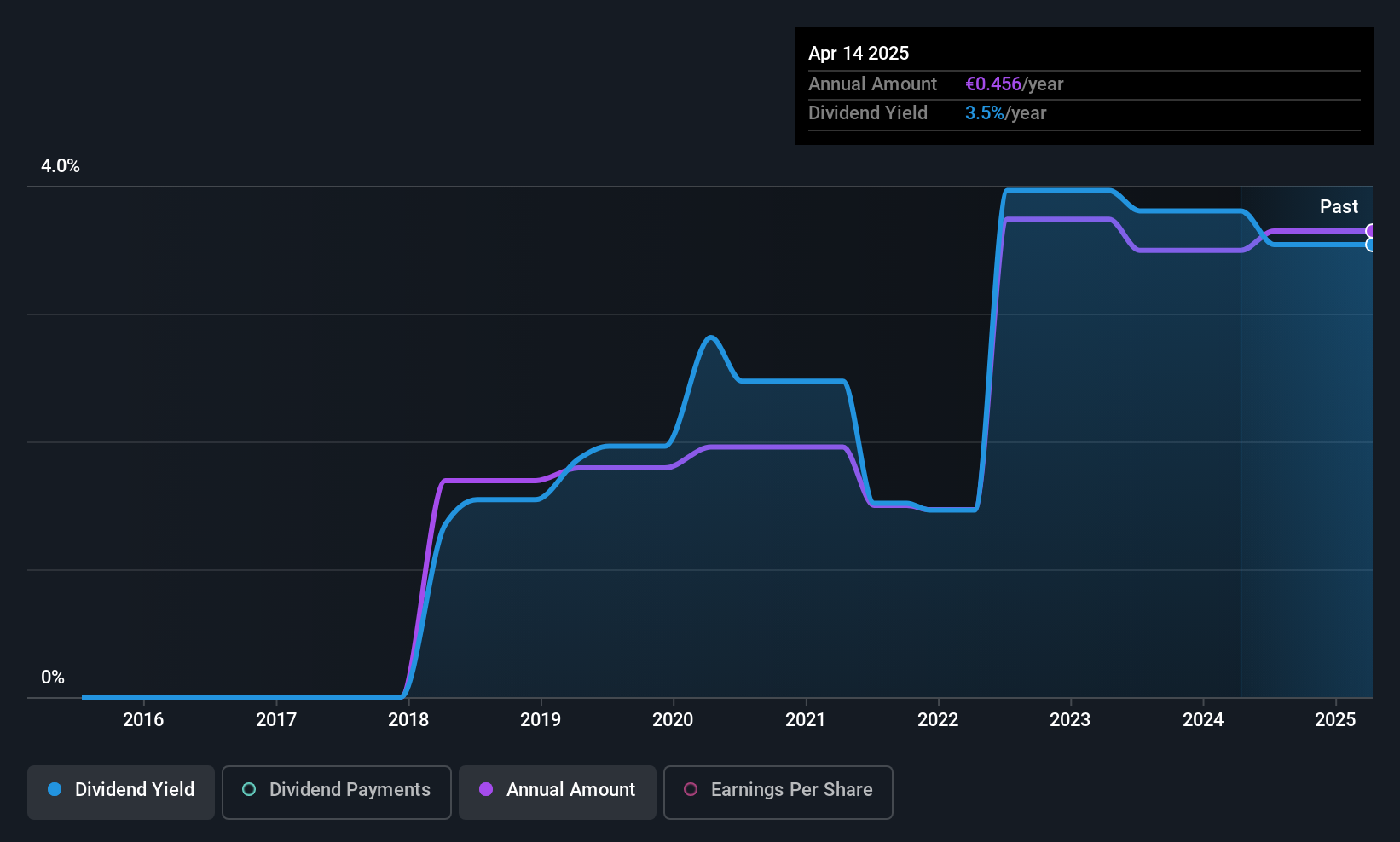

Miquel y Costas & Miquel, S.A. (BME:MCM) has announced that it will be increasing its dividend from last year's comparable payment on the 17th of July to €0.1063. This takes the annual payment to 3.2% of the current stock price, which is about average for the industry.

Miquel y Costas & Miquel's Future Dividend Projections Appear Well Covered By Earnings

Solid dividend yields are great, but they only really help us if the payment is sustainable. However, prior to this announcement, Miquel y Costas & Miquel's dividend was comfortably covered by both cash flow and earnings. This means that most of its earnings are being retained to grow the business.

Looking forward, earnings per share could rise by 6.1% over the next year if the trend from the last few years continues. If the dividend continues on this path, the payout ratio could be 32% by next year, which we think can be pretty sustainable going forward.

Check out our latest analysis for Miquel y Costas & Miquel

Miquel y Costas & Miquel's Dividend Has Lacked Consistency

It's comforting to see that Miquel y Costas & Miquel has been paying a dividend for a number of years now, however it has been cut at least once in that time. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. Since 2018, the annual payment back then was €0.212, compared to the most recent full-year payment of €0.456. This works out to be a compound annual growth rate (CAGR) of approximately 12% a year over that time. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

Miquel y Costas & Miquel Could Grow Its Dividend

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. We are encouraged to see that Miquel y Costas & Miquel has grown earnings per share at 6.1% per year over the past five years. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

In Summary

In summary, it's great to see that the company can raise the dividend and keep it in a sustainable range. While the payout ratios are a good sign, we are less enthusiastic about the company's dividend record. This looks like it could be a good dividend stock going forward, but we would note that the payout ratio has been at higher levels in the past so it could happen again.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Case in point: We've spotted 2 warning signs for Miquel y Costas & Miquel (of which 1 makes us a bit uncomfortable!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.