Here's Why It's Unlikely That South China Holdings Company Limited's (HKG:413) CEO Will See A Pay Rise This Year

Key Insights

- South China Holdings will host its Annual General Meeting on 17th of June

- CEO Christina Cheung's total compensation includes salary of HK$3.02m

- The overall pay is 100% above the industry average

- South China Holdings' three-year loss to shareholders was 57% while its EPS was down 72% over the past three years

South China Holdings Company Limited (HKG:413) has not performed well recently and CEO Christina Cheung will probably need to up their game. At the upcoming AGM on 17th of June, shareholders can hear from the board including their plans for turning around performance. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. We present the case why we think CEO compensation is out of sync with company performance.

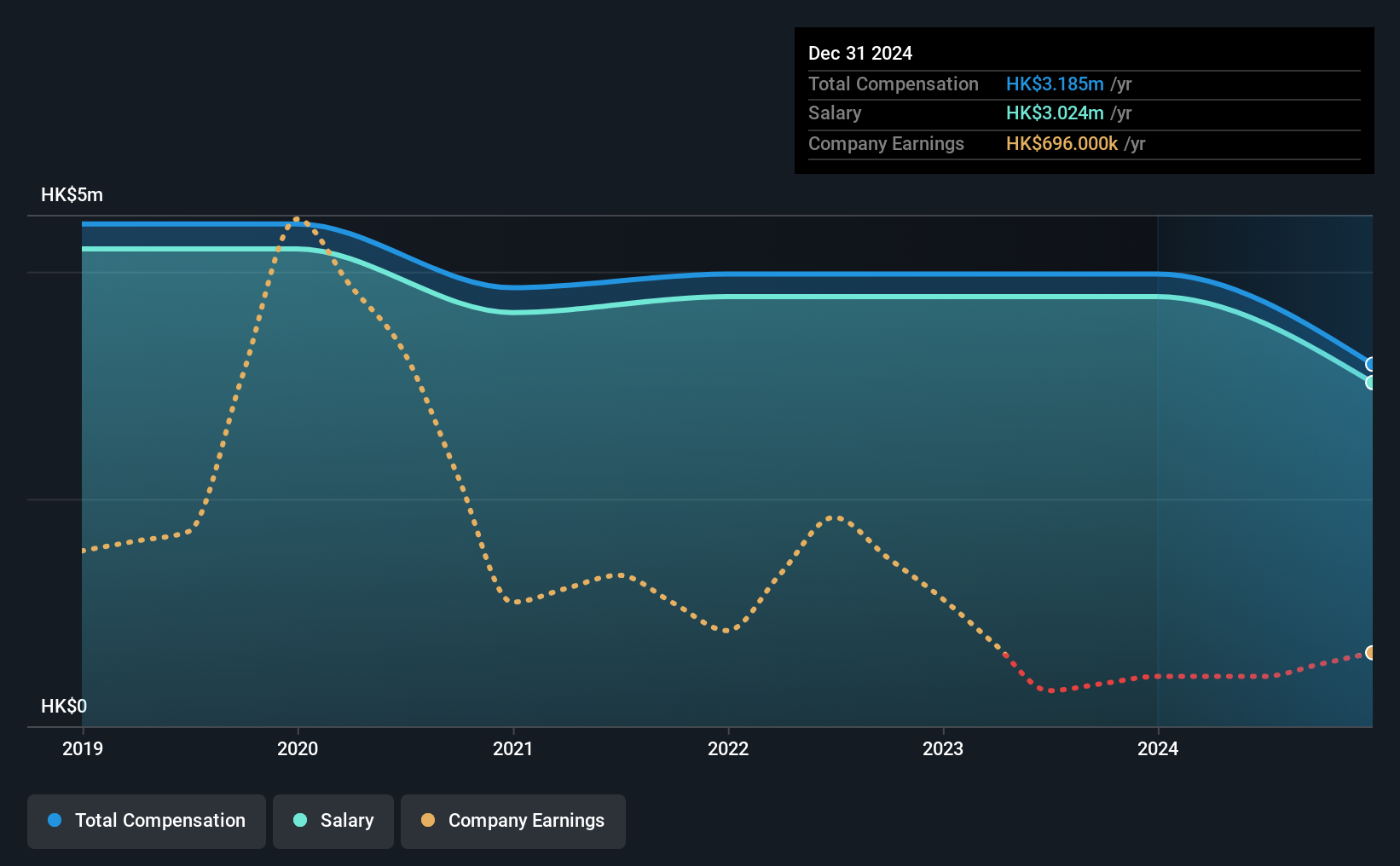

See our latest analysis for South China Holdings

Comparing South China Holdings Company Limited's CEO Compensation With The Industry

According to our data, South China Holdings Company Limited has a market capitalization of HK$389m, and paid its CEO total annual compensation worth HK$3.2m over the year to December 2024. We note that's a decrease of 20% compared to last year. We note that the salary portion, which stands at HK$3.02m constitutes the majority of total compensation received by the CEO.

In comparison with other companies in the Hong Kong Leisure industry with market capitalizations under HK$1.6b, the reported median total CEO compensation was HK$1.6m. This suggests that Christina Cheung is paid more than the median for the industry. What's more, Christina Cheung holds HK$1.2m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | HK$3.0m | HK$3.8m | 95% |

| Other | HK$161k | HK$199k | 5% |

| Total Compensation | HK$3.2m | HK$4.0m | 100% |

Speaking on an industry level, nearly 92% of total compensation represents salary, while the remainder of 8% is other remuneration. There isn't a significant difference between South China Holdings and the broader market, in terms of salary allocation in the overall compensation package. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at South China Holdings Company Limited's Growth Numbers

Over the last three years, South China Holdings Company Limited has shrunk its earnings per share by 72% per year. Its revenue is up 12% over the last year.

The decline in EPS is a bit concerning. While the revenue growth is good to see, it is outweighed by the fact that EPS are down, over three years. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has South China Holdings Company Limited Been A Good Investment?

Few South China Holdings Company Limited shareholders would feel satisfied with the return of -57% over three years. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Given that shareholders haven't seen any positive returns on their investment, not to mention the lack of earnings growth, this may suggest that few of them would be willing to award the CEO with a pay rise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We identified 4 warning signs for South China Holdings (2 are significant!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.