Undervalued Asian Small Caps With Insider Buying To Consider

In recent weeks, the Asian markets have experienced a mix of challenges and opportunities, with Chinese stocks gaining traction amid hopes for government stimulus and Japan's economy showing signs of moderate recovery despite some economic headwinds. In this context, identifying promising small-cap stocks involves looking at companies that can navigate these dynamic conditions effectively, often indicated by insider buying as a potential sign of confidence in their future performance.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.4x | 1.0x | 36.78% | ★★★★★★ |

| East West Banking | 3.1x | 0.7x | 33.66% | ★★★★★☆ |

| Lion Rock Group | 5.0x | 0.4x | 49.52% | ★★★★☆☆ |

| Dicker Data | 18.6x | 0.6x | -14.39% | ★★★★☆☆ |

| Atturra | 28.1x | 1.2x | 33.01% | ★★★★☆☆ |

| Sing Investments & Finance | 7.4x | 3.7x | 38.56% | ★★★★☆☆ |

| AInnovation Technology Group | NA | 2.3x | 48.90% | ★★★★☆☆ |

| Integral Diagnostics | 152.5x | 1.8x | 35.74% | ★★★☆☆☆ |

| China Lesso Group Holdings | 7.0x | 0.4x | -385.29% | ★★★☆☆☆ |

| Tabcorp Holdings | NA | 0.6x | -26.36% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

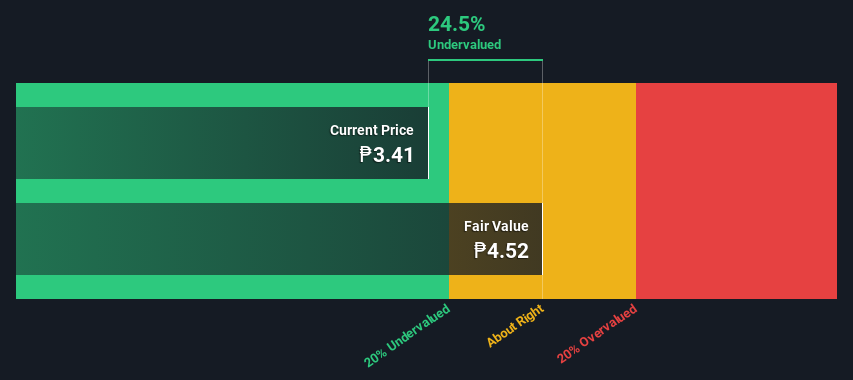

Bloomberry Resorts (PSE:BLOOM)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Bloomberry Resorts operates integrated resort facilities, primarily focusing on gaming and entertainment, with a market capitalization of ₱116.89 billion.

Operations: The company's primary revenue stream is from its integrated resort facility, with recent quarterly revenue reaching ₱54.66 billion. It has experienced fluctuations in net income margins, with a notable high of 21.96% and a low of -75.72%. The gross profit margin has shown variability as well, peaking at 95.27% and dropping to 27.53%, reflecting changes in cost management efficiency over time. Operating expenses have been significant, impacting profitability alongside non-operating expenses such as depreciation and amortization costs.

PE: 17.4x

Bloomberry Resorts, a notable player in the Asian hospitality sector, recently showcased strong financial performance with first-quarter sales of PHP 12.93 billion and net income rising to PHP 3.32 billion. Insider confidence is evident as Cyrus Sherafat acquired over 9 million shares for approximately PHP 69.93 million between March and May 2025. Despite volatility in its share price, the company maintains a promising growth outlook with earnings projected to grow annually by over 11%.

- Delve into the full analysis valuation report here for a deeper understanding of Bloomberry Resorts.

Assess Bloomberry Resorts' past performance with our detailed historical performance reports.

China Lesso Group Holdings (SEHK:2128)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: China Lesso Group Holdings is a leading industrial group in China specializing in the production and sale of building materials and interior decoration products, with a market cap of approximately CN¥22.48 billion.

Operations: The company generates revenue primarily from its Plastics & Rubber segment, with a reported revenue of CN¥27.03 billion. The cost of goods sold (COGS) for the same period was CN¥19.73 billion, leading to a gross profit margin of 26.99%. Operating expenses, including sales and marketing as well as general and administrative costs, totaled CN¥3.42 billion, while non-operating expenses amounted to CN¥2.19 billion. The net income for the period was CN¥1.68 billion, resulting in a net income margin of 6.23%.

PE: 7.0x

China Lesso Group Holdings, operating in the construction materials sector, exhibits potential value with a forecasted earnings growth of 12.29% annually. Despite a drop in sales to CNY 27 billion and net income to CNY 1.68 billion for 2024, insider confidence is evident through recent share purchases by executives throughout early 2025. The company approved a HK$0.20 per share dividend for shareholders, indicating financial stability despite external borrowing risks. Leadership changes include appointing Mr. Huang Zhanxiong as an executive director, focusing on strategic expansion into new energy storage markets, which could drive future growth opportunities.

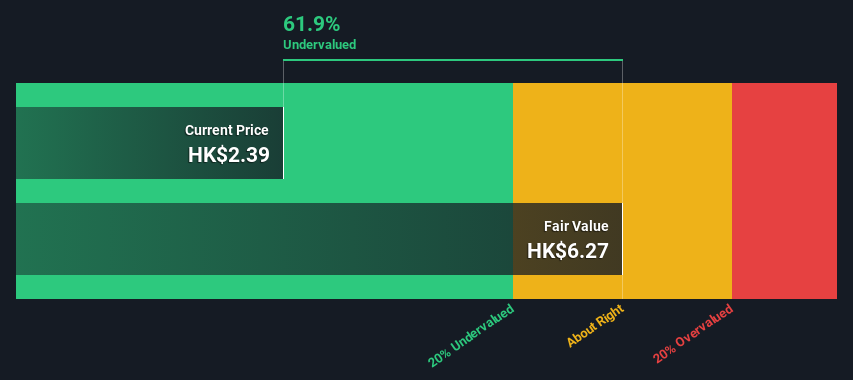

Shougang Fushan Resources Group (SEHK:639)

Simply Wall St Value Rating: ★★★★★☆

Overview: Shougang Fushan Resources Group is engaged in the coking coal mining industry, with operations focused on producing and selling coking coal.

Operations: The primary revenue stream comes from coking coal mining, with recent revenues reaching HK$5.06 billion. The gross profit margin has shown variability, peaking at 68.34% and recently recorded at 51.18%. Operating expenses are primarily driven by general and administrative costs, along with sales and marketing expenses.

PE: 9.1x

Shougang Fushan Resources Group, a small player in Asia's market, recently saw insider confidence with Deputy MD & Executive Director Zhaoqiang Chen purchasing 640,000 shares valued at HK$1.52 million in March 2025. Despite earnings forecasts predicting a 1.9% annual decline over the next three years and reliance on higher-risk external borrowing for funding, the company proposed a dividend increase to HK$0.21 per share for 2024. Recent board changes include Xu Qian's appointment as non-executive director, bringing extensive financial expertise to the table amidst an auditor rotation aimed at enhancing corporate governance.

Where To Now?

- Dive into all 62 of the Undervalued Asian Small Caps With Insider Buying we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com