- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalTop TSX Dividend Stocks For May 2025

As trade tensions ease and the Bank of Canada maintains a neutral stance on interest rates, the Canadian market is experiencing gains, providing a favorable environment for dividend stocks. In this context, selecting dividend stocks with strong fundamentals and consistent payout histories can offer investors potential stability and income amid evolving economic conditions.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Whitecap Resources (TSX:WCP) | 8.64% | ★★★★★☆ |

| Canadian Imperial Bank of Commerce (TSX:CM) | 4.36% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 4.17% | ★★★★★☆ |

| IGM Financial (TSX:IGM) | 5.12% | ★★★★★☆ |

| Power Corporation of Canada (TSX:POW) | 4.46% | ★★★★★☆ |

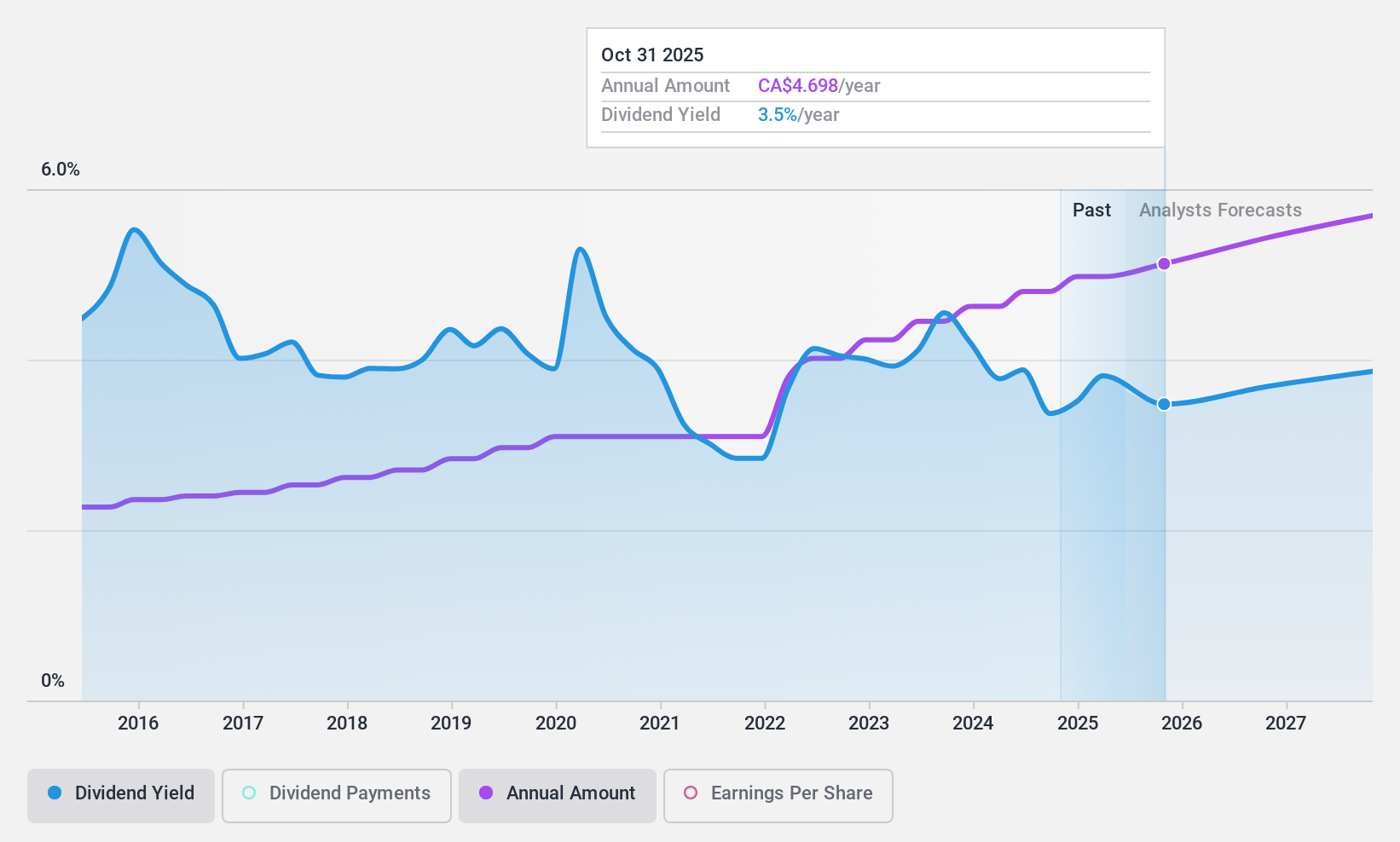

| Royal Bank of Canada (TSX:RY) | 3.50% | ★★★★★☆ |

| Olympia Financial Group (TSX:OLY) | 6.80% | ★★★★★☆ |

| National Bank of Canada (TSX:NA) | 3.62% | ★★★★★☆ |

| Acadian Timber (TSX:ADN) | 6.61% | ★★★★★☆ |

| Sun Life Financial (TSX:SLF) | 4.03% | ★★★★★☆ |

Click here to see the full list of 25 stocks from our Top TSX Dividend Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

National Bank of Canada (TSX:NA)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: National Bank of Canada offers a range of financial services to individuals, businesses, institutional clients, and governments both domestically and internationally, with a market cap of CA$48.90 billion.

Operations: National Bank of Canada's revenue segments include Wealth Management at CA$2.90 billion, Personal and Commercial at CA$4.30 billion, Financial Markets (Excluding USSF&I) at CA$3.22 billion, and U.S. Specialty Finance and International (USSF&I) at CA$1.30 billion.

Dividend Yield: 3.6%

National Bank of Canada offers a stable dividend with a payout ratio of 40.1%, suggesting dividends are well covered by earnings and forecasted to remain so at 44% in three years. Despite the dividend yield of 3.62% being lower than the top Canadian payers, it remains reliable and has grown over the past decade. Recent news highlights strategic moves, such as redeeming $125 million in debentures, aligning with regulatory capital management efforts.

- Click to explore a detailed breakdown of our findings in National Bank of Canada's dividend report.

- Upon reviewing our latest valuation report, National Bank of Canada's share price might be too pessimistic.

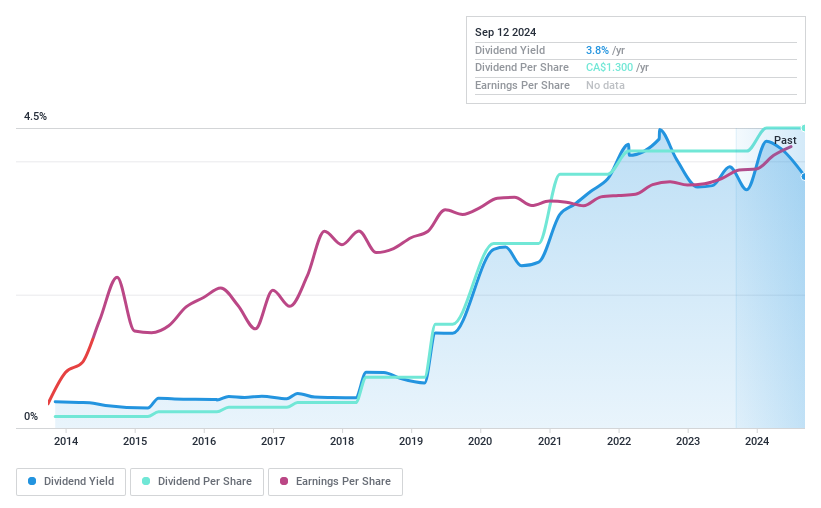

Quebecor (TSX:QBR.A)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Quebecor Inc. operates in the telecommunications, media, and sports and entertainment sectors in Canada, with a market cap of CA$8.89 billion.

Operations: Quebecor Inc.'s revenue is primarily derived from its telecommunications segment at CA$4.82 billion, followed by media at CA$698.80 million, and sports and entertainment contributing CA$228.30 million.

Dividend Yield: 3.6%

Quebecor's dividends are well-supported by a 40.1% payout ratio from earnings and a 36% cash payout ratio, indicating sustainability. The dividend yield stands at 3.59%, below the top Canadian payers but has shown consistent growth over the past decade. Despite high debt levels, Quebecor trades at a significant discount to estimated fair value, offering potential for capital appreciation alongside reliable dividends. Recent earnings show improved profitability with net income rising to C$190.7 million in Q1 2025.

- Dive into the specifics of Quebecor here with our thorough dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Quebecor shares in the market.

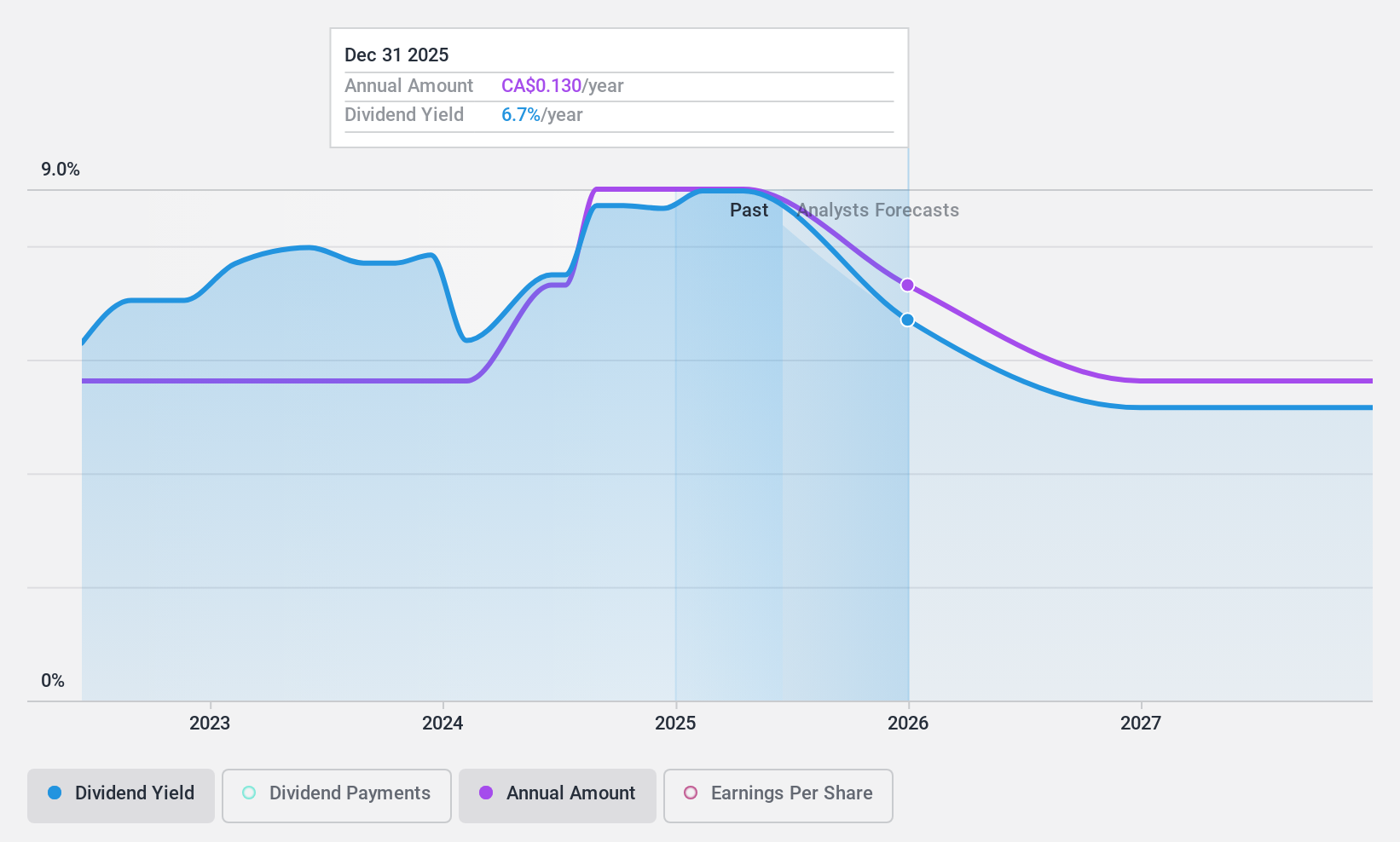

Hemisphere Energy (TSXV:HME)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Hemisphere Energy Corporation acquires, explores, develops, and produces petroleum and natural gas interests in Canada with a market cap of CA$166.47 million.

Operations: Hemisphere Energy Corporation generates revenue of CA$79.71 million from its petroleum and natural gas interests in Canada.

Dividend Yield: 9.1%

Hemisphere Energy's dividends are supported by a 29.6% payout ratio from earnings and a 62.7% cash payout ratio, suggesting sustainability. The company declared a special dividend of C$0.03 per share in addition to its quarterly base dividend, reflecting strong financial health. With a high dividend yield of 9.14%, Hemisphere is among the top Canadian payers despite only three years of consistent dividends, and it trades at an attractive value with a low price-to-earnings ratio of 5.1x.

- Delve into the full analysis dividend report here for a deeper understanding of Hemisphere Energy.

- Our comprehensive valuation report raises the possibility that Hemisphere Energy is priced lower than what may be justified by its financials.

Summing It All Up

- Unlock more gems! Our Top TSX Dividend Stocks screener has unearthed 22 more companies for you to explore.Click here to unveil our expertly curated list of 25 Top TSX Dividend Stocks.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com