Asian Growth Companies With High Insider Ownership

Amid escalating trade tensions and heightened market volatility, the Asian markets have been navigating a complex economic landscape. As investors seek stability and growth potential, companies with high insider ownership often stand out due to their alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Arctech Solar Holding (SHSE:688408) | 37.9% | 24.7% |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.3% | 26% |

| AcrelLtd (SZSE:300286) | 40% | 32% |

| Shanghai Huace Navigation Technology (SZSE:300627) | 24.7% | 24.3% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 39.9% |

| Global Tax Free (KOSDAQ:A204620) | 20.8% | 35.1% |

| Vuno (KOSDAQ:A338220) | 15.6% | 148.6% |

| Synspective (TSE:290A) | 12.8% | 44.5% |

| Fulin Precision (SZSE:300432) | 13.6% | 74.7% |

Let's review some notable picks from our screened stocks.

PharmaResearch (KOSDAQ:A214450)

Simply Wall St Growth Rating: ★★★★★★

Overview: PharmaResearch Co., Ltd., along with its subsidiaries, is a biopharmaceutical company operating mainly in South Korea with a market cap of ₩3.80 trillion.

Operations: The company generates revenue primarily from its Pharmaceuticals segment, amounting to ₩350.12 billion.

Insider Ownership: 38.6%

Return On Equity Forecast: 23% (2027 estimate)

PharmaResearch demonstrates strong growth potential with earnings forecasted to grow 27.8% annually, outpacing the Korean market's 22%. Revenue is expected to increase by 20.7% per year, surpassing both its historical performance and market averages. The company trades at a discount of 9.7% below estimated fair value, indicating potential undervaluation. Despite no recent insider trading activity, high insider ownership aligns management interests with shareholders, supporting long-term growth prospects in Asia's competitive landscape.

- Get an in-depth perspective on PharmaResearch's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that PharmaResearch's share price might be on the expensive side.

Beijing Wantai Biological Pharmacy Enterprise (SHSE:603392)

Simply Wall St Growth Rating: ★★★★★★

Overview: Beijing Wantai Biological Pharmacy Enterprise Co., Ltd. operates in the biotechnology and pharmaceutical sector, focusing on diagnostics and vaccines, with a market cap of CN¥85.80 billion.

Operations: Revenue segments for the company include diagnostics generating CN¥3.45 billion and vaccines contributing CN¥2.67 billion.

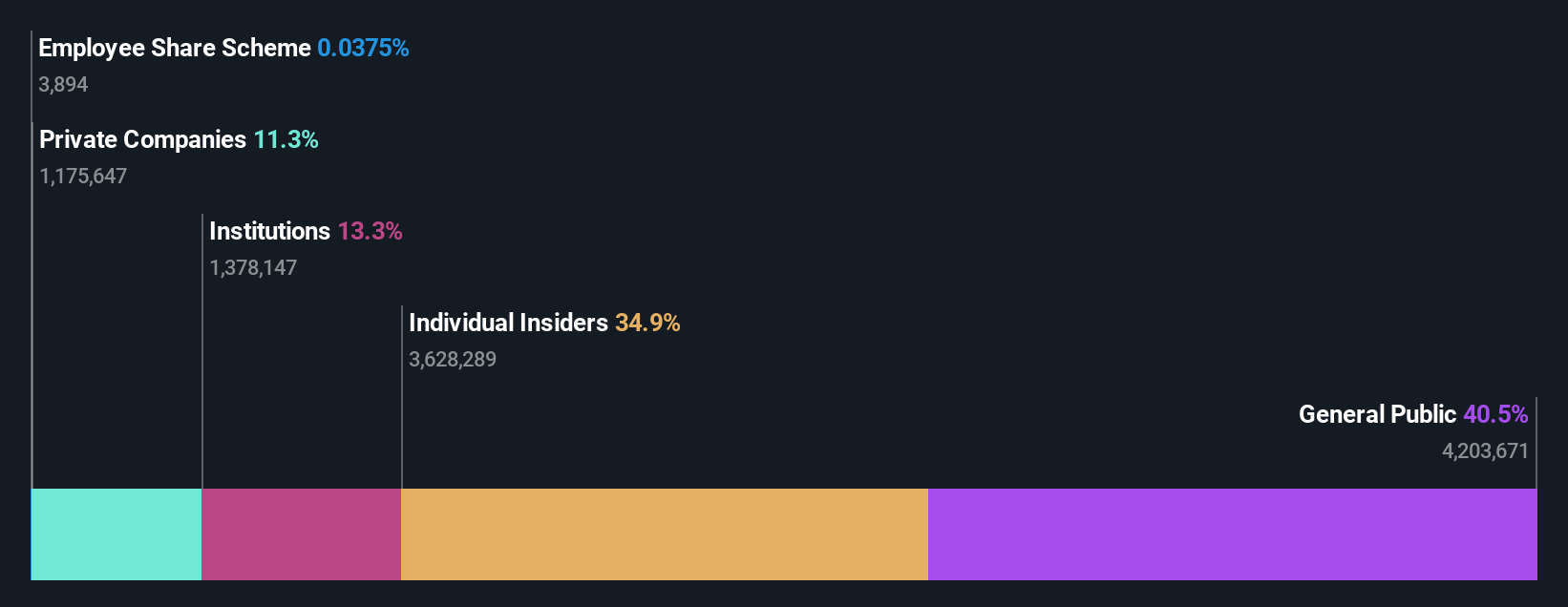

Insider Ownership: 24%

Return On Equity Forecast: 21% (2027 estimate)

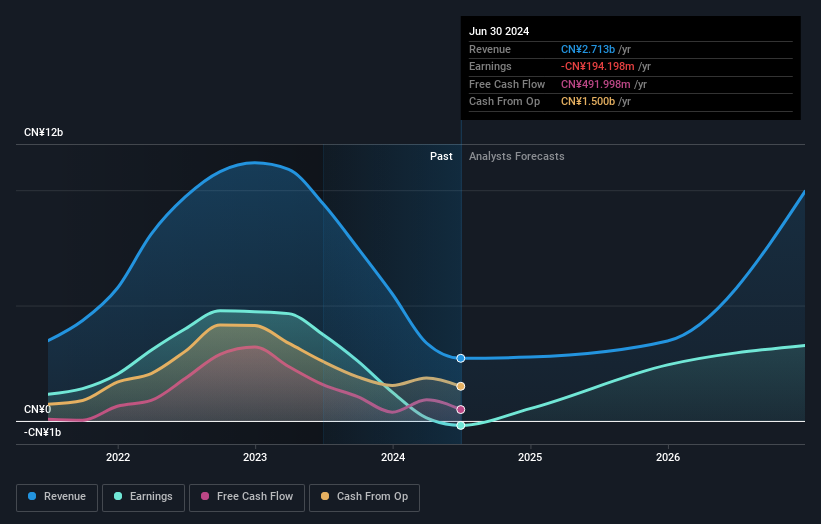

Beijing Wantai Biological Pharmacy Enterprise's earnings are forecasted to grow significantly at 91.6% annually, far exceeding the Chinese market average of 24%. Revenue is also expected to rise by 66.7% per year, indicating robust growth potential despite a recent decline in sales and net income. High insider ownership aligns management with shareholders, although profit margins have decreased due to large one-off items impacting financial results. No significant insider trading has been reported recently.

- Click here to discover the nuances of Beijing Wantai Biological Pharmacy Enterprise with our detailed analytical future growth report.

- Our valuation report unveils the possibility Beijing Wantai Biological Pharmacy Enterprise's shares may be trading at a premium.

International Games SystemLtd (TPEX:3293)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: International Games System Co., Ltd. engages in the planning, design, research, development, manufacturing, marketing, servicing, and licensing of arcade, online, and mobile games primarily in Taiwan, the United Kingdom, and China with a market cap of NT$231.92 billion.

Operations: The company's revenue is primarily derived from its Online Games Division, which generated NT$11.51 billion, and its Business Game Division, contributing NT$7.01 billion.

Insider Ownership: 11.3%

Return On Equity Forecast: 58% (2027 estimate)

International Games System Ltd. has shown impressive financial performance, with sales reaching TWD 18.51 billion and net income at TWD 9.06 billion for the year ending December 31, 2024. Earnings per share increased significantly compared to the previous year. The company's revenue is forecasted to grow at a rate of 17.8% annually, outpacing the Taiwanese market average of 10%. Despite high earnings quality, its dividend yield of 3.52% is not well covered by earnings or free cash flows.

- Click here and access our complete growth analysis report to understand the dynamics of International Games SystemLtd.

- In light of our recent valuation report, it seems possible that International Games SystemLtd is trading beyond its estimated value.

Next Steps

- Click this link to deep-dive into the 633 companies within our Fast Growing Asian Companies With High Insider Ownership screener.

- Want To Explore Some Alternatives? The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com