- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalPunjab Chemicals and Crop Protection Limited's (NSE:PUNJABCHEM) largest shareholders are private companies who were rewarded as market cap surged ₹1.2b last week

Key Insights

- Significant control over Punjab Chemicals and Crop Protection by private companies implies that the general public has more power to influence management and governance-related decisions

- 57% of the business is held by the top 2 shareholders

- Using data from company's past performance alongside ownership research, one can better assess the future performance of a company

A look at the shareholders of Punjab Chemicals and Crop Protection Limited (NSE:PUNJABCHEM) can tell us which group is most powerful. We can see that private companies own the lion's share in the company with 60% ownership. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

As a result, private companies were the biggest beneficiaries of last week’s 12% gain.

In the chart below, we zoom in on the different ownership groups of Punjab Chemicals and Crop Protection.

See our latest analysis for Punjab Chemicals and Crop Protection

What Does The Lack Of Institutional Ownership Tell Us About Punjab Chemicals and Crop Protection?

Institutional investors often avoid companies that are too small, too illiquid or too risky for their tastes. But it's unusual to see larger companies without any institutional investors.

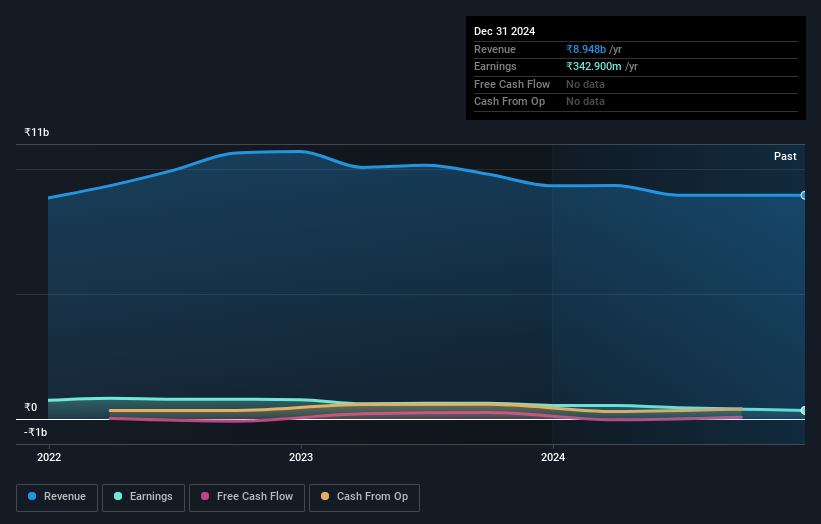

There are many reasons why a company might not have any institutions on the share registry. It may be hard for institutions to buy large amounts of shares, if liquidity (the amount of shares traded each day) is low. If the company has not needed to raise capital, institutions might lack the opportunity to build a position. Alternatively, there might be something about the company that has kept institutional investors away. Punjab Chemicals and Crop Protection's earnings and revenue track record (below) may not be compelling to institutional investors -- or they simply might not have looked at the business closely.

Punjab Chemicals and Crop Protection is not owned by hedge funds. The company's largest shareholder is Hem-Sil Trading And Manufacturing Private Limited, with ownership of 33%. Demuric Holdings Pvt. Ltd. is the second largest shareholder owning 24% of common stock, and Excel Industries Limited holds about 4.8% of the company stock.

A more detailed study of the shareholder registry showed us that 2 of the top shareholders have a considerable amount of ownership in the company, via their 57% stake.

While it makes sense to study institutional ownership data for a company, it also makes sense to study analyst sentiments to know which way the wind is blowing. As far as we can tell there isn't analyst coverage of the company, so it is probably flying under the radar.

Insider Ownership Of Punjab Chemicals and Crop Protection

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

We can see that insiders own shares in Punjab Chemicals and Crop Protection Limited. In their own names, insiders own ₹882m worth of stock in the ₹11b company. This shows at least some alignment, but we usually like to see larger insider holdings. You can click here to see if those insiders have been buying or selling.

General Public Ownership

The general public-- including retail investors -- own 27% stake in the company, and hence can't easily be ignored. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Private Company Ownership

It seems that Private Companies own 60%, of the Punjab Chemicals and Crop Protection stock. It might be worth looking deeper into this. If related parties, such as insiders, have an interest in one of these private companies, that should be disclosed in the annual report. Private companies may also have a strategic interest in the company.

Public Company Ownership

We can see that public companies hold 4.8% of the Punjab Chemicals and Crop Protection shares on issue. We can't be certain but it is quite possible this is a strategic stake. The businesses may be similar, or work together.

Next Steps:

It's always worth thinking about the different groups who own shares in a company. But to understand Punjab Chemicals and Crop Protection better, we need to consider many other factors. For instance, we've identified 1 warning sign for Punjab Chemicals and Crop Protection that you should be aware of.

If you would prefer check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, backed by strong financial data.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.