Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalShould You Buy or Hold Molina Healthcare Stock Before Q3 Earnings?

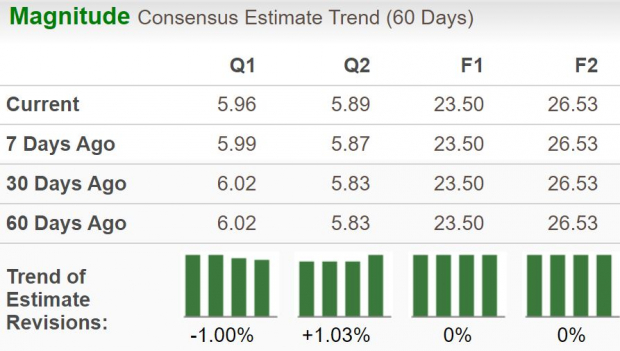

Molina Healthcare, Inc. MOH is set to report third-quarter 2024 results on Oct. 23, 2024, after the closing bell. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $5.96 per share on revenues of $9.96 billion.

Stay up-to-date with all quarterly releases: See Zacks Earnings Calendar.

The third-quarter earnings estimate has witnessed downward revisions over the past 60 days. However, the bottom-line projection indicates a year-over-year increase of 18%. The Zacks Consensus Estimate for quarterly revenues suggests year-over-year growth of 16.5%.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Molina Healthcare has a robust history of surpassing earnings estimates, beating the consensus estimate in each of the last four quarters, with the average surprise being 3.1%. This is depicted in the figure below.

Molina Healthcare, Inc Price and EPS Surprise

Molina Healthcare, Inc price-eps-surprise | Molina Healthcare, Inc Quote

Q3 Earnings Whispers for MOH

However, our proven model does not conclusively predict an earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the odds of an earnings beat. That’s not the case here.

MOH has an Earnings ESP of -0.49% and a Zacks Rank #3.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

What’s Shaping MOH’s Q3 Results?

The growing customer base in the Medicaid and Medicare businesses of Molina Healthcare is expected to have contributed to premium growth, the most significant contributor to the top line of a health insurer, in the third quarter. The Zacks Consensus Estimate for premiums indicates growth of 16.4% year over year in the third quarter, while our model estimate suggests a 15.2% increase. We expect Medicaid premiums to grow more than 10% year over year to $7.4 billion in the to-be-reported quarter. The consensus estimate for the Medicare premiums is $1.48 billion, up 43.1% year over year.

Several contract wins from federal and state authorities, renewal of agreements, as well as buyouts, are likely to have contributed to membership growth in MOH’s Medicaid and Medicare businesses. An aging U.S. population is likely to have sustained the solid demand for its Medicare plans in the third quarter. The Medicaid membership growth is likely to have been partially offset by the redetermination process. Membership within the Medicaid business is expected to increase 5.5% year over year, while the same for MOH’s Medicare business is projected to witness 47.2% growth.

Marketplace membership, after falling 19.3% year over year in 2023, is expected to grow in each quarter of 2024. The Zacks Consensus Estimate for the metric suggests a 31.9% increase from the year-ago period.

A favorable interest rate environment is likely to have driven higher investment income, which, in turn, is likely to have aided revenue growth in the third quarter. The Zacks Consensus Estimate for investment income indicates a 4.5% rise year over year. The factors stated above are likely to position the company for year-over-year growth.

However, the consensus mark for medical care ratio (MCR) in Marketplace is pegged at 81.98% in the to-be-reported quarter, up from 78.90% a year ago, due to elevated medical expenses. An uptick in MCR signals lower leftover premiums consequent to the payment of insurance claims.

Our model estimate for third quarter total operating expenses predicts a more than 15% increase from the year-ago period, due to higher medical care costs and G&A expenses, making an earnings beat uncertain.

MOH’s Price Performance & Valuation

Molina Healthcare's stock has declined 19.9% year to date, underperforming the industry’s growth of 3%. Some of its peers like Humana Inc. HUM and Centene Corporation CNC have plunged 41.8% and 15.1%, respectively, during this time. All these stocks have lagged the S&P 500 significantly, which has rallied 22.5% during the same period.

MOH’s YTD Price Performance

Image Source: Zacks Investment Research

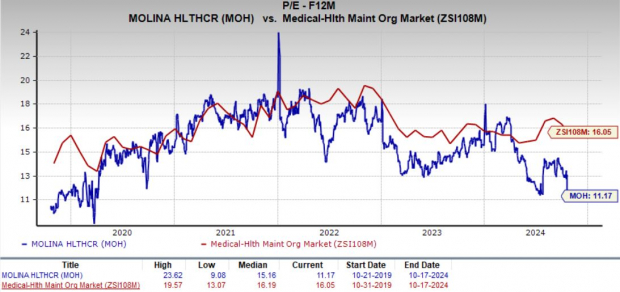

Now, let’s look at the value Molina Healthcare offers investors at current levels.

The company’s valuation looks cheaper compared with the industry average. Currently, MOH is trading at 11.17X forward 12 months earnings, below its five-year median of 15.16X and the industry’s average of 16.05X.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Assessing Molina Healthcare’s Prospects

Molina Healthcare is expected to see consistent growth in its revenue base due to contract wins. Memberships in its Marketplace unit will likely increase going forward. It focuses on buyouts to boost the company's portfolio and diversify income and geographic footprint. Its return on equity — a major profitability measure — is 28.1%, better than the industry average of 23.9%. The metric reflects the company's effectiveness in utilizing its shareholders' money compared with the industry peers, which impresses investors.

Its strong balance sheet provides robust financial flexibility. Its long-term debt to capital of 33% is lower than the industry average of 38.3%. However, challenges such as rising MCR, limited long-term upside for Medicaid margin, and redeterminations weighing on enrollment could affect MOH’s performance. Investors should closely monitor these factors.

Final Words

Although MOH’s long-term outlook remains promising, it might not be the right time to buy just yet. Current investors can hold on to their stocks and benefit from its growth prospects. However, prospective buyers may consider waiting for a more favorable entry point and keep an eye on its margin-improving efforts in the upcoming earnings.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Humana Inc. (HUM): Free Stock Analysis Report

Molina Healthcare, Inc (MOH): Free Stock Analysis Report

Centene Corporation (CNC): Free Stock Analysis Report