Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 US Growth Stocks With High Insider Ownership And 167% Earnings Growth

As the U.S. stock market continues to reach new heights, with the Dow Jones Industrial Average marking its 39th record close of the year, investors are increasingly focused on growth opportunities amid strong economic indicators. In this robust environment, stocks with high insider ownership and significant earnings growth can offer compelling prospects for those looking to align their interests with company insiders who have a vested interest in long-term success.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 41.9% |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.4% |

| GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 26% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 33.3% |

| Super Micro Computer (NasdaqGS:SMCI) | 25.7% | 28.0% |

| Hims & Hers Health (NYSE:HIMS) | 13.7% | 37.4% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.0% | 95% |

| Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

| BBB Foods (NYSE:TBBB) | 22.9% | 51.2% |

Underneath we present a selection of stocks filtered out by our screen.

Burke & Herbert Financial Services (NasdaqCM:BHRB)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Burke & Herbert Financial Services Corp. is the bank holding company for Burke & Herbert Bank & Trust Company, offering a range of community banking products and services in Virginia and Maryland, with a market cap of $957.52 million.

Operations: The company generates revenue of $124.67 million from its community banking products and services in Virginia and Maryland.

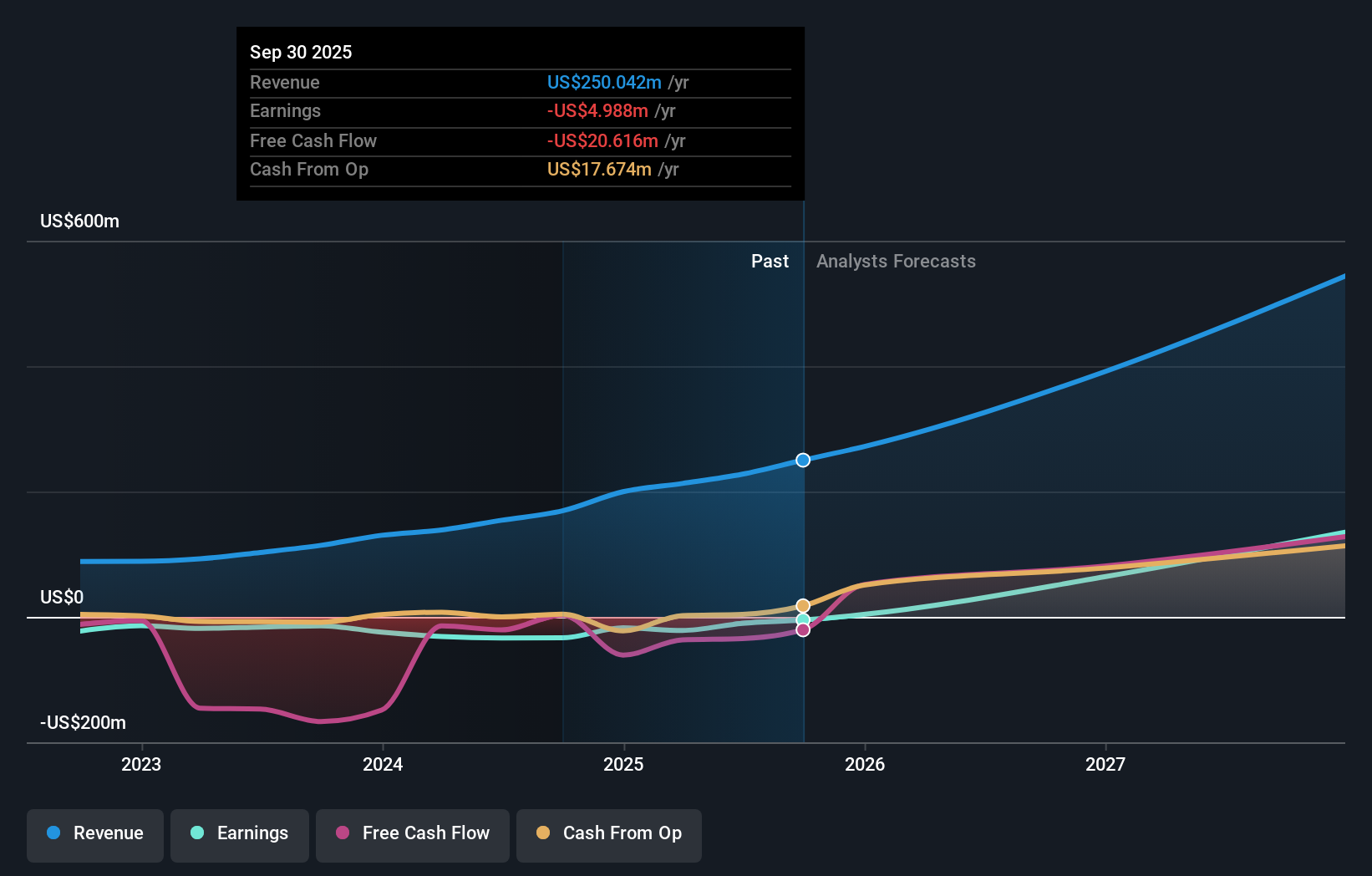

Insider Ownership: 12.5%

Earnings Growth Forecast: 167.6% p.a.

Burke & Herbert Financial Services demonstrates significant insider ownership with recent substantial insider buying and no major selling in the past three months. Despite a challenging financial performance, including a net loss of US$16.92 million for Q2 2024, the company is forecast to achieve above-average market profit growth over the next three years. Revenue is expected to grow at 57.3% annually, outpacing the US market's growth rate. The stock trades at 25.2% below its estimated fair value, suggesting potential undervaluation amidst its inclusion in the S&P Global BMI Index as of September 2024.

- Get an in-depth perspective on Burke & Herbert Financial Services' performance by reading our analyst estimates report here.

- In light of our recent valuation report, it seems possible that Burke & Herbert Financial Services is trading beyond its estimated value.

Harrow (NasdaqGM:HROW)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Harrow, Inc. is an eyecare pharmaceutical company focused on the discovery, development, and commercialization of ophthalmic pharmaceutical products with a market cap of approximately $1.95 billion.

Operations: The company's revenue segment consists of $154.15 million from the discovery, development, and commercialization of innovative ophthalmic therapies.

Insider Ownership: 14.3%

Earnings Growth Forecast: 76.7% p.a.

Harrow exhibits high insider ownership and is forecast to grow revenue at a robust 39.5% annually, outpacing the US market's growth rate of 8.8%. Despite reporting a net loss of US$6.47 million for Q2 2024, Harrow's earnings are expected to grow significantly at 76.72% per year, with profitability anticipated within three years. The company's recent relaunch of TRIESENCE® could bolster its market position further, although its share price remains highly volatile and trades significantly below estimated fair value.

- Dive into the specifics of Harrow here with our thorough growth forecast report.

- Our valuation report unveils the possibility Harrow's shares may be trading at a discount.

Ibotta (NYSE:IBTA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ibotta, Inc. is a technology company that provides the Ibotta Performance Network (IPN) for consumer packaged goods brands to offer digital promotions to consumers, with a market cap of $2.08 billion.

Operations: The company's revenue is primarily derived from its Internet Software segment, which generated $355.21 million.

Insider Ownership: 18.8%

Earnings Growth Forecast: 68.4% p.a.

Ibotta recently joined the S&P Global BMI Index, signaling increased market recognition. Despite a net loss of US$33.97 million in Q2 2024, its revenue rose to US$87.93 million from the previous year. The company forecasts significant earnings growth at 68.4% annually and expects revenue to grow faster than the market at 16.5% per year. A new partnership with Instacart could enhance its consumer reach, although insider selling has been significant recently.

- Delve into the full analysis future growth report here for a deeper understanding of Ibotta.

- Our comprehensive valuation report raises the possibility that Ibotta is priced lower than what may be justified by its financials.

Summing It All Up

- Explore the 186 names from our Fast Growing US Companies With High Insider Ownership screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com