Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalDiscover Three Indian Growth Stocks With Strong Insider Ownership

Over the last 7 days, the Indian market has experienced a slight decline of 1.0%, yet it remains robust with a 39% increase over the past year and an anticipated annual earnings growth of 17%. In this context, identifying growth stocks with strong insider ownership can be particularly appealing as they often indicate management's confidence in their company's long-term potential amidst fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership In India

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| Jupiter Wagons (NSEI:JWL) | 10.8% | 27.4% |

| Dixon Technologies (India) (NSEI:DIXON) | 24.6% | 30.8% |

| Paisalo Digital (BSE:532900) | 16.3% | 24.8% |

| Apollo Hospitals Enterprise (NSEI:APOLLOHOSP) | 10.4% | 32.3% |

| Rajratan Global Wire (BSE:517522) | 18.3% | 35.8% |

| Pricol (NSEI:PRICOLLTD) | 25.5% | 24% |

| KEI Industries (BSE:517569) | 19.2% | 22.5% |

| Aether Industries (NSEI:AETHER) | 31.1% | 45.8% |

Below we spotlight a couple of our favorites from our exclusive screener.

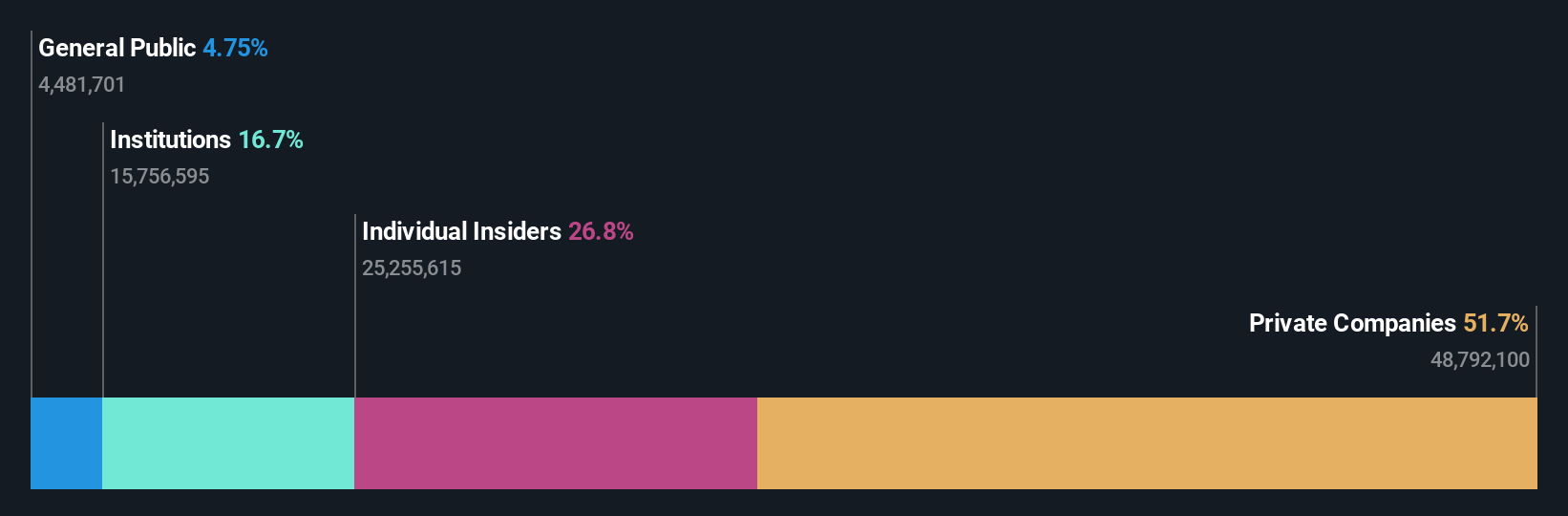

Five-Star Business Finance (NSEI:FIVESTAR)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Five-Star Business Finance Limited is a non-banking financial company in India with a market cap of ₹262.58 billion.

Operations: The company's revenue primarily comes from MSME Loans, Housing Loans, and Property Loans, totaling ₹17.79 billion.

Insider Ownership: 18.7%

Revenue Growth Forecast: 21.9% p.a.

Five-Star Business Finance demonstrates robust growth potential, with forecasted revenue and earnings growth exceeding 20% annually. Despite a low return on equity projection of 19.4%, its price-to-earnings ratio of 29.1x is attractive compared to the Indian market average. Recent strategic moves include issuing INR 25 billion in non-convertible debentures and appointing Deloitte as auditors, indicating a focus on strengthening financial governance and expanding capital resources for future growth initiatives.

- Navigate through the intricacies of Five-Star Business Finance with our comprehensive analyst estimates report here.

- Our valuation report here indicates Five-Star Business Finance may be overvalued.

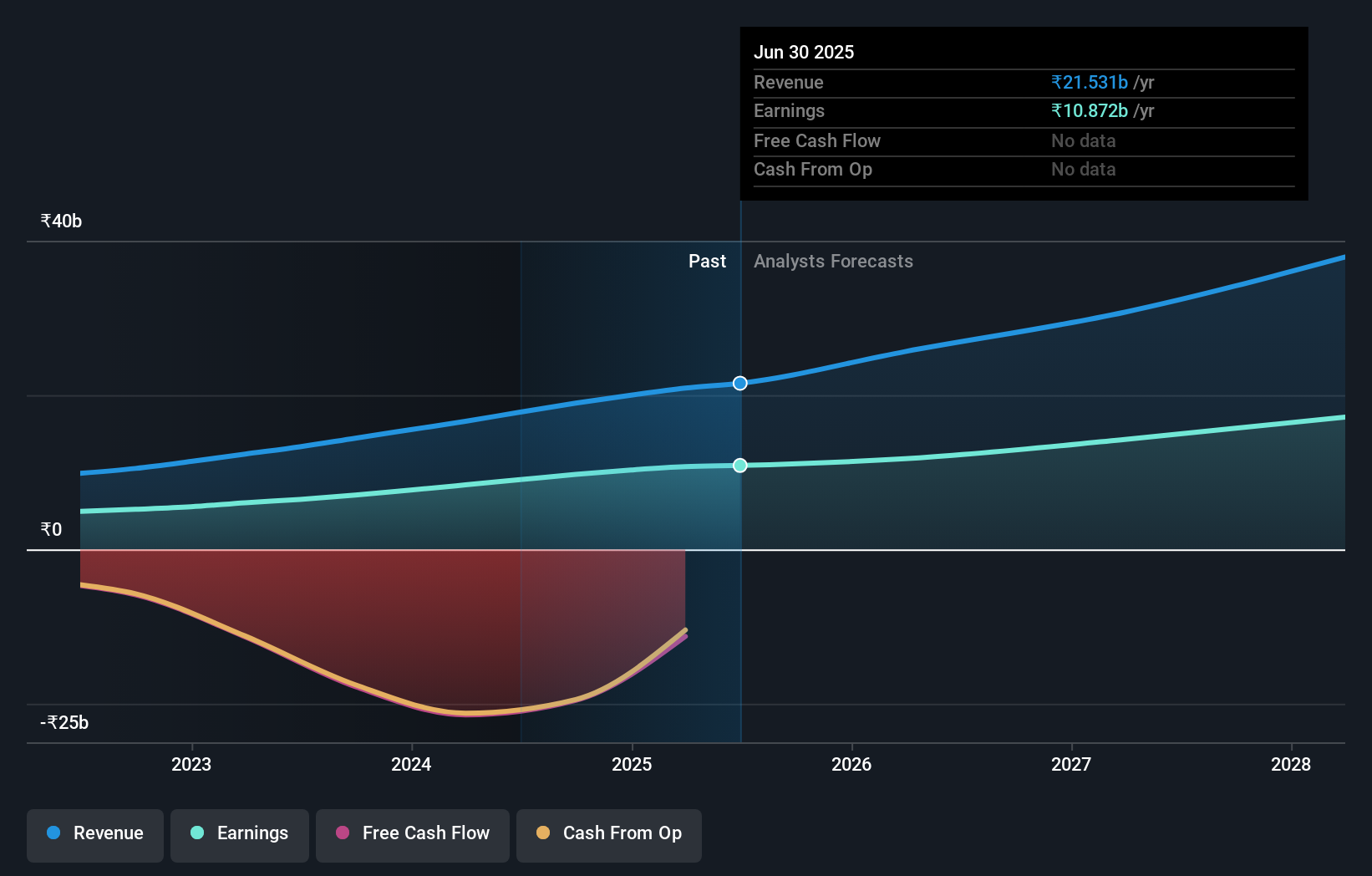

Happy Forgings (NSEI:HAPPYFORGE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Happy Forgings Limited manufactures and sells forgings and related components both in India and internationally, with a market cap of ₹104.43 billion.

Operations: The company's revenue is primarily derived from its Forged and Machined Products segment, which generated ₹13.70 billion.

Insider Ownership: 26.8%

Revenue Growth Forecast: 17% p.a.

Happy Forgings exhibits strong growth potential, with earnings expected to grow significantly at 20.4% annually, outpacing the Indian market. Despite a low forecasted return on equity of 18.7%, analysts anticipate a 24.1% stock price increase. Recent earnings show stable sales and revenue growth, though net income slightly declined year-over-year to ₹638 million in Q1 2025. The dividend yield remains modest at 0.36%, suggesting limited coverage by free cash flows.

- Take a closer look at Happy Forgings' potential here in our earnings growth report.

- Our expertly prepared valuation report Happy Forgings implies its share price may be too high.

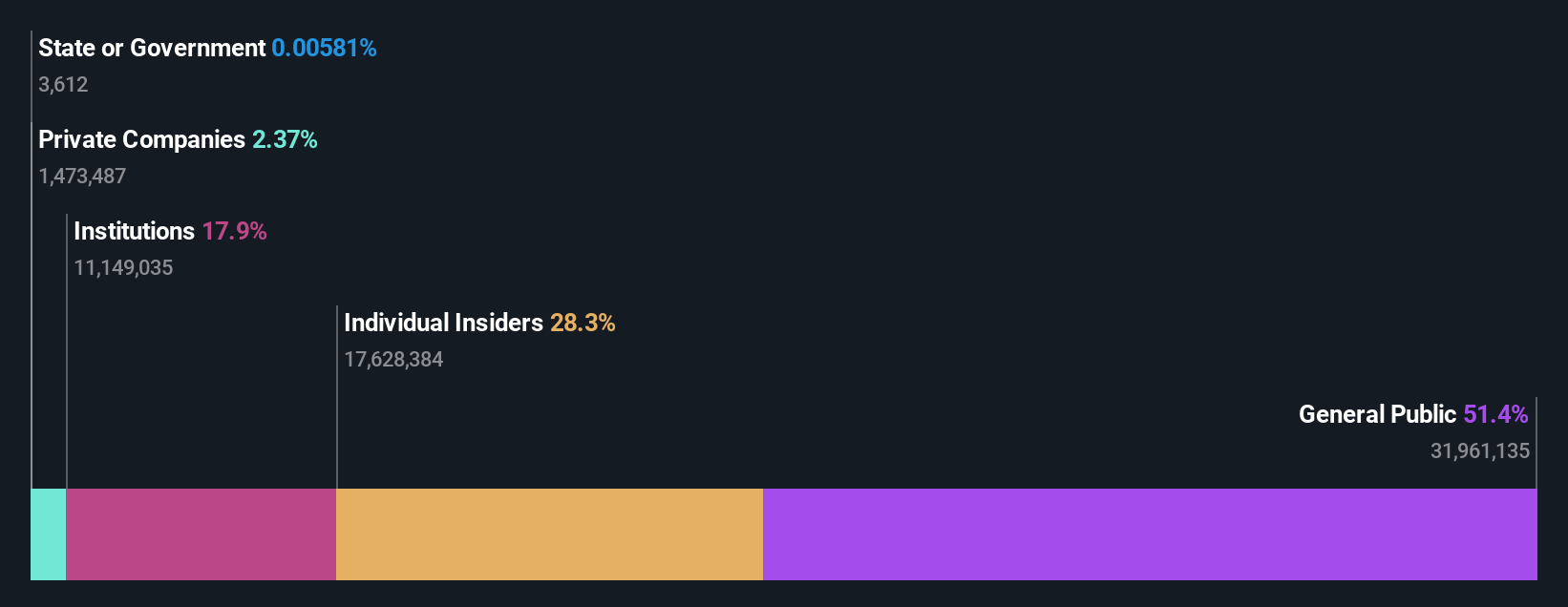

VA Tech Wabag (NSEI:WABAG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: VA Tech Wabag Limited, along with its subsidiaries, specializes in the design, supply, installation, construction, operation, and maintenance of drinking water, waste and industrial water treatment, and desalination plants both in India and internationally; it has a market cap of ₹110.57 billion.

Operations: The company's revenue primarily comes from the construction and maintenance of water treatment plants, amounting to ₹29.30 billion.

Insider Ownership: 28.3%

Revenue Growth Forecast: 17.4% p.a.

VA Tech Wabag demonstrates substantial growth potential, with earnings projected to grow at 27.3% annually, surpassing the Indian market's average. Despite no significant insider buying recently, the company has secured major contracts, including a ₹10 billion desalination project with Indosol Solar and a $317 million contract in Saudi Arabia. Legal challenges persist but are being contested. Recent financials show revenue growth from ₹5.79 billion to ₹6.37 billion year-over-year for Q1 2024-25.

- Dive into the specifics of VA Tech Wabag here with our thorough growth forecast report.

- According our valuation report, there's an indication that VA Tech Wabag's share price might be on the expensive side.

Turning Ideas Into Actions

- Navigate through the entire inventory of 87 Fast Growing Indian Companies With High Insider Ownership here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com