Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalEuronext Amsterdam's Top 3 Growth Stocks With High Insider Ownership

As the pan-European STOXX Europe 600 Index shows signs of optimism with a recent increase, hopes are rising for more accommodative monetary policies from the European Central Bank. Amidst this backdrop, investors are increasingly looking at growth companies with high insider ownership as potential opportunities on Euronext Amsterdam, where such stocks may offer alignment between management and shareholder interests in an evolving economic landscape.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| Ebusco Holding (ENXTAM:EBUS) | 31% | 107.8% |

| Envipco Holding (ENXTAM:ENVI) | 36.7% | 84% |

| MotorK (ENXTAM:MTRK) | 35.7% | 108.4% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 77.7% |

| CVC Capital Partners (ENXTAM:CVC) | 20.2% | 33.5% |

| PostNL (ENXTAM:PNL) | 35.6% | 38.6% |

Underneath we present a selection of stocks filtered out by our screen.

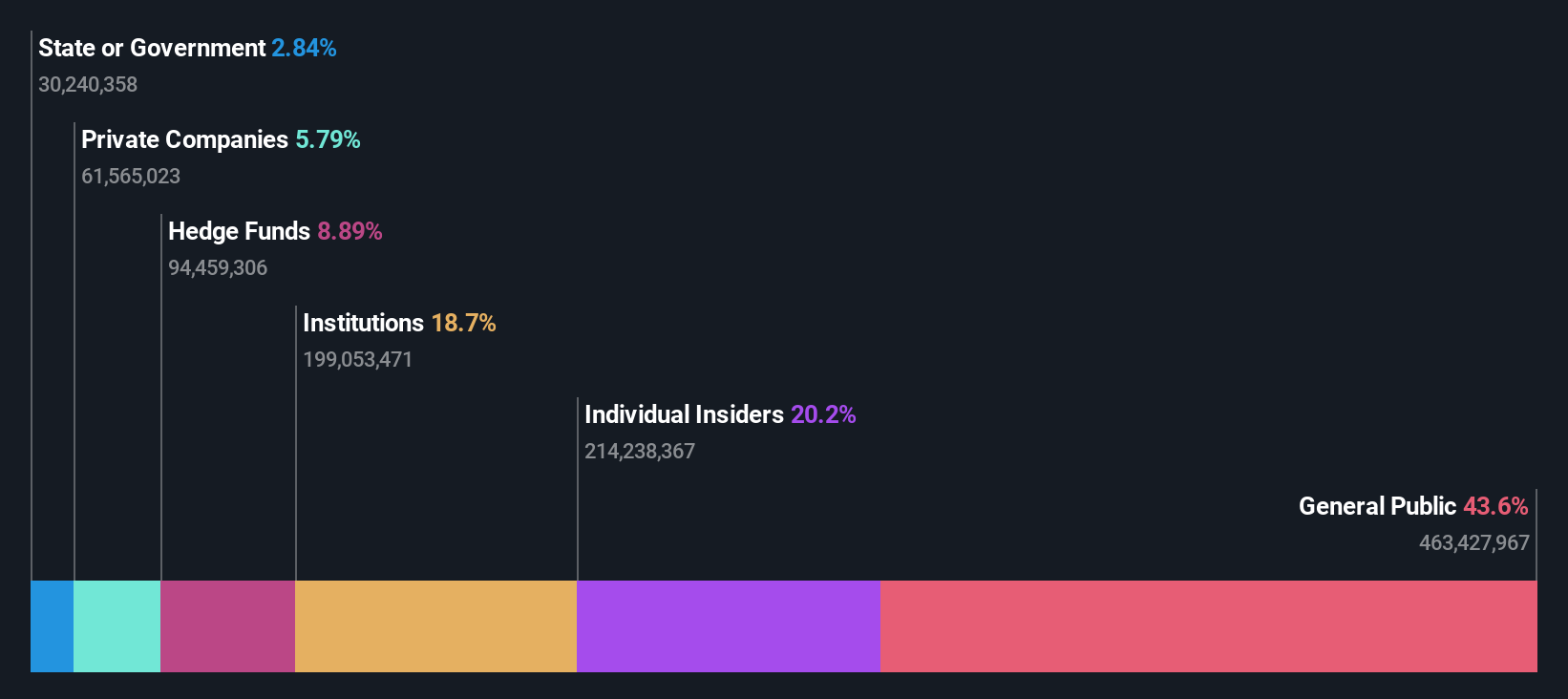

CVC Capital Partners (ENXTAM:CVC)

Simply Wall St Growth Rating: ★★★★★☆

Overview: CVC Capital Partners plc is a private equity and venture capital firm that focuses on middle market secondaries, infrastructure and credit, management buyouts, leveraged buyouts, growth equity, mature investments, recapitalizations, strip sales, and spinouts with a market cap of €21.83 billion.

Operations: CVC Capital Partners plc generates revenue through its focus on private equity and venture capital activities, including middle market secondaries, infrastructure and credit investments, management buyouts, leveraged buyouts, growth equity, mature investments, recapitalizations, strip sales, and spinouts.

Insider Ownership: 20.2%

CVC Capital Partners, a private equity firm in the Netherlands, is poised for significant growth with expected annual earnings increases of 33.5%, outpacing the Dutch market. Trading below its estimated fair value, CVC's financial position is bolstered by high insider ownership. Recent M&A activities include interest in Deutsche Bahn’s Schenker unit and Aavas Financiers. Despite losing to DSV for Schenker, CVC remains active in strategic acquisitions to enhance its portfolio.

- Click here and access our complete growth analysis report to understand the dynamics of CVC Capital Partners.

- Our valuation report here indicates CVC Capital Partners may be overvalued.

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Envipco Holding N.V. is a company that specializes in the design, development, manufacture, assembly, marketing, sale, leasing, and servicing of reverse vending machines for collecting and processing used beverage containers across the Netherlands, North America, and Europe with a market cap of €299.99 million.

Operations: Envipco Holding generates revenue through the design, development, and provision of reverse vending machines for used beverage container collection and processing in the Netherlands, North America, and Europe.

Insider Ownership: 36.7%

Envipco Holding is set for strong growth, with revenue anticipated to increase at 35.6% annually, surpassing the Dutch market's average. Earnings are forecasted to grow significantly at 84% per year, indicating robust expansion potential. Recent developments include a follow-on order from a major Romanian retailer for over 140 Optima RVMs, enhancing its market presence. Despite recent board changes and share price volatility, Envipco remains focused on expanding its operations and improving profitability.

- Dive into the specifics of Envipco Holding here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that Envipco Holding is priced higher than what may be justified by its financials.

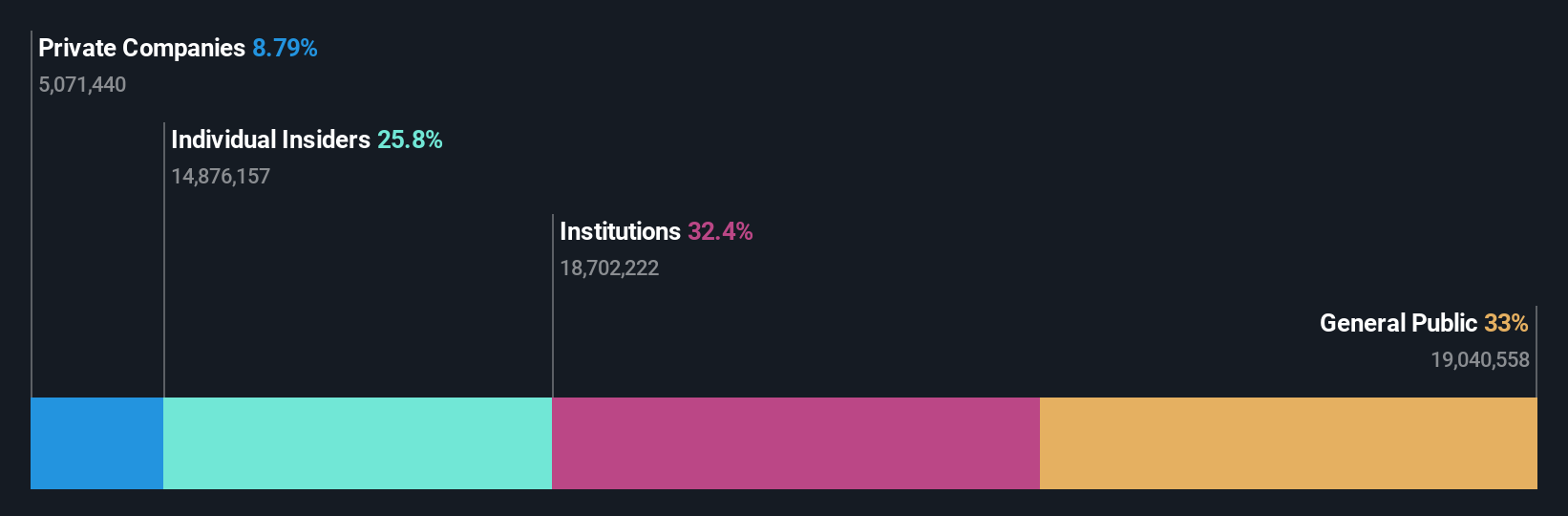

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc offers software-as-a-service solutions for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union with a market cap of €260.21 million.

Operations: The company generates revenue of €42.50 million from its software and programming services tailored for the automotive retail sector in Italy, Spain, France, Germany, and the Benelux Union.

Insider Ownership: 35.7%

MotorK's revenue is projected to grow at 22.1% annually, significantly outpacing the Dutch market average of 8.8%. The company reported a net loss of €6.48 million for H1 2024, an improvement from the prior year's €7.8 million loss, with earnings forecasted to grow by over 100% annually. Despite high share price volatility and limited cash runway, MotorK is expected to achieve profitability within three years, highlighting its growth potential amidst challenges.

- Take a closer look at MotorK's potential here in our earnings growth report.

- Our expertly prepared valuation report MotorK implies its share price may be too high.

Next Steps

- Click this link to deep-dive into the 6 companies within our Fast Growing Euronext Amsterdam Companies With High Insider Ownership screener.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com