Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 Japanese Growth Companies With High Insider Ownership Growing Earnings Up To 54%

Japan's stock markets have recently experienced an upward trend, with the Nikkei 225 Index gaining 2.45% and the broader TOPIX Index rising by 0.45%, supported by a weaker yen that has enhanced the profit outlook for exporters. In this context, identifying growth companies with high insider ownership can be particularly appealing, as such firms often align management interests with shareholder value and may offer robust earnings potential even amidst fluctuating economic conditions.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 31.5% |

| Hottolink (TSE:3680) | 26.1% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 40.2% |

| Medley (TSE:4480) | 34% | 30.4% |

| Inforich (TSE:9338) | 19.1% | 29.8% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 75.2% |

| Money Forward (TSE:3994) | 21.4% | 71.3% |

| Loadstar Capital K.K (TSE:3482) | 33.8% | 24.3% |

| Soracom (TSE:147A) | 16.5% | 54.1% |

Let's review some notable picks from our screened stocks.

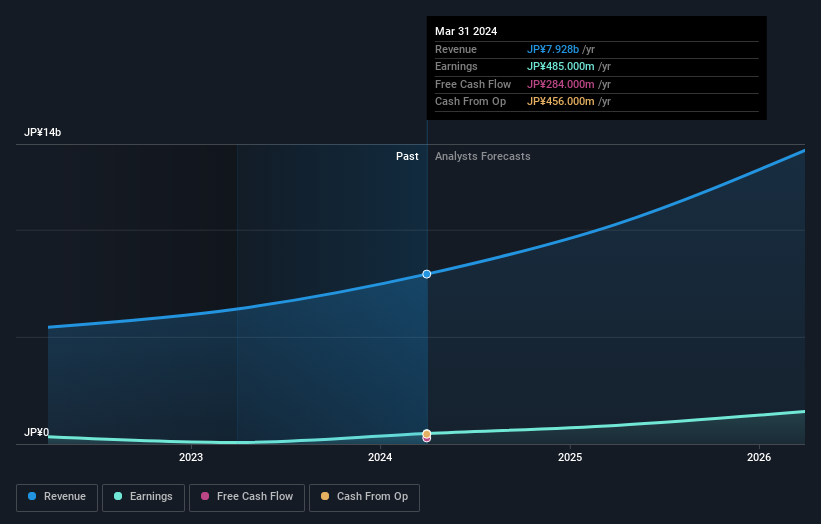

Soracom (TSE:147A)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Soracom, Inc. offers Internet of Things (IoT) based cellular connectivity solutions and has a market capitalization of approximately ¥61.22 billion.

Operations: The company's revenue is primarily derived from its IoT Platform segment, which generated ¥7.93 billion.

Insider Ownership: 16.5%

Earnings Growth Forecast: 54.1% p.a.

Soracom is experiencing robust growth, with expected revenue increases of 27.2% annually, surpassing the Japanese market average. Earnings are projected to grow significantly at 54.1% per year, well above the market's 8.7%. Despite high earnings quality and substantial past profit growth of over 500%, its share price has been highly volatile recently. The company forecasts net sales of ¥9.91 billion and an operating profit of ¥925 million for the fiscal year ending March 2025.

- Dive into the specifics of Soracom here with our thorough growth forecast report.

- Our expertly prepared valuation report Soracom implies its share price may be too high.

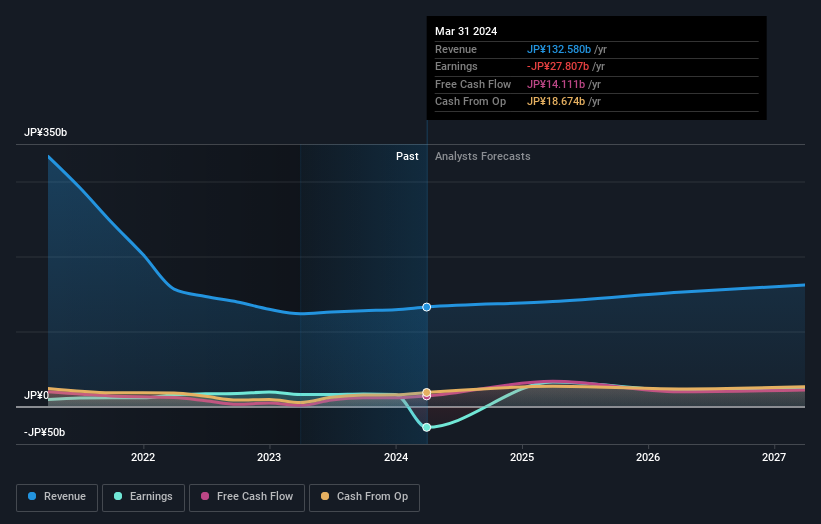

JAPAN MATERIAL (TSE:6055)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: JAPAN MATERIAL Co., Ltd. operates in the electronics and graphics sectors in Japan, with a market cap of ¥188.94 billion.

Operations: The company generates revenue from its electronics segment with ¥47.65 billion, graphics solution business at ¥1.56 billion, and solar power generation business contributing ¥206 million.

Insider Ownership: 35.3%

Earnings Growth Forecast: 24.3% p.a.

Japan Material is positioned for growth with its earnings projected to increase significantly at 24.27% annually, outpacing the Japanese market's 8.7%. Despite a forecasted revenue growth of 14.7% per year, which is slower than some high-growth peers but still above the market average of 4.3%, its shares have shown high volatility recently. The stock trades at a discount, being valued at 32.5% below estimated fair value, although future return on equity remains modest at 17.9%.

- Click here and access our complete growth analysis report to understand the dynamics of JAPAN MATERIAL.

- The valuation report we've compiled suggests that JAPAN MATERIAL's current price could be inflated.

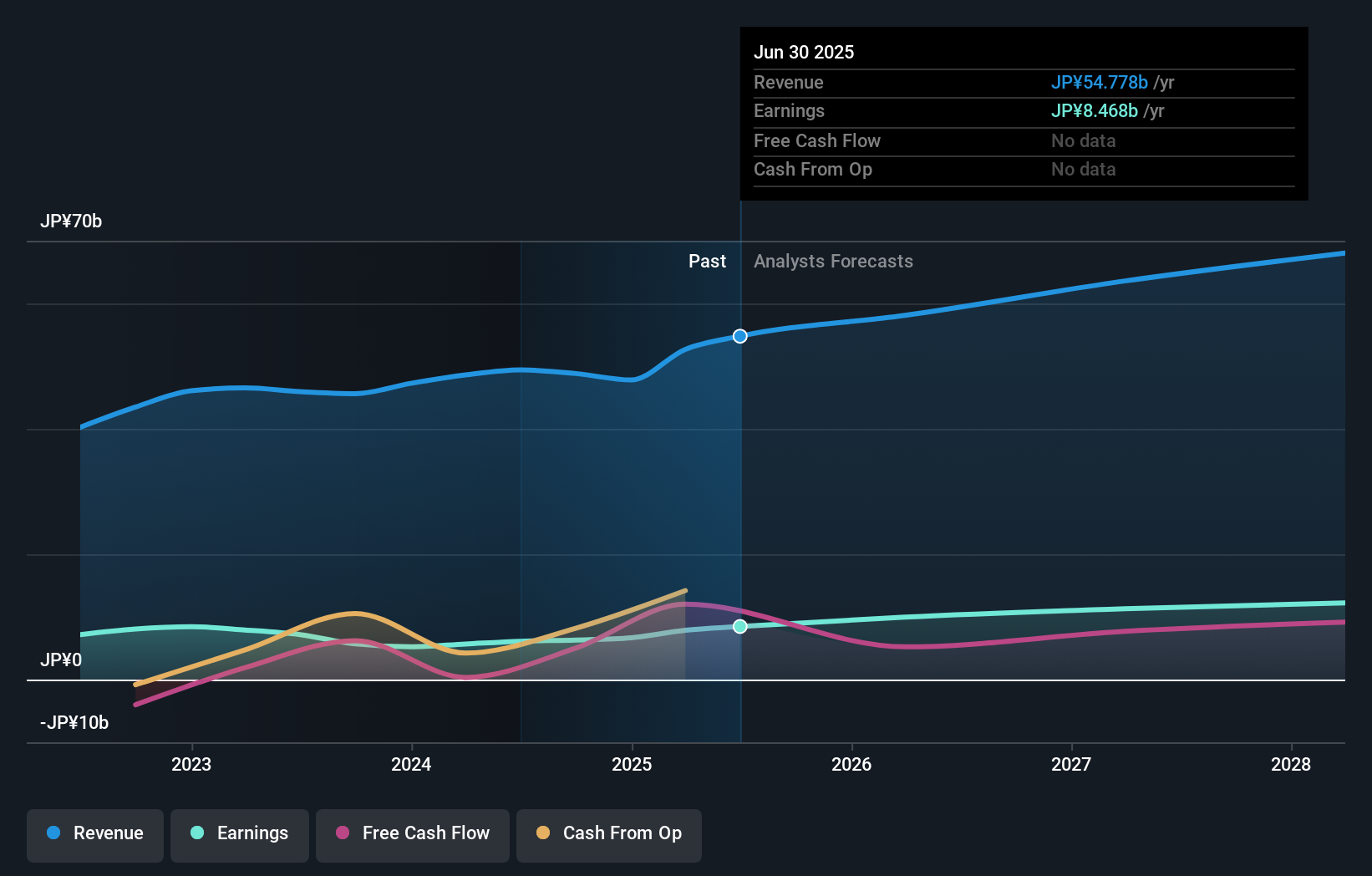

Relo Group (TSE:8876)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Relo Group, Inc. provides property management services in Japan and has a market cap of ¥288.80 billion.

Operations: The company's revenue segments include the Welfare Program at ¥25.94 billion, Tourism Business at ¥14.64 billion, and Relocation Business at ¥95.54 billion.

Insider Ownership: 28.0%

Earnings Growth Forecast: 23.3% p.a.

Relo Group exhibits strong growth potential, with earnings expected to increase by 23.29% annually and revenue growing at 6.2%, surpassing the Japanese market's average of 4.3%. Despite trading at a 23.1% discount to its estimated fair value, its dividend yield of 1.98% is not well covered by earnings. The company has completed a share buyback worth ¥4,354.05 million, enhancing capital efficiency and potentially benefiting insider ownership dynamics in the long term.

- Click to explore a detailed breakdown of our findings in Relo Group's earnings growth report.

- Our comprehensive valuation report raises the possibility that Relo Group is priced higher than what may be justified by its financials.

Summing It All Up

- Get an in-depth perspective on all 101 Fast Growing Japanese Companies With High Insider Ownership by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com