Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalSGX Stocks Like Digital Core REIT That May Be Trading Below Estimated Value

The Singapore market has been navigating a period of volatility, with investors closely monitoring economic indicators and global events that could impact the Straits Times Index. In such an environment, identifying undervalued stocks can be crucial for investors seeking opportunities, as these stocks may offer potential value relative to their current market price.

Top 3 Undervalued Stocks Based On Cash Flows In Singapore

| Name | Current Price | Fair Value (Est) | Discount (Est) |

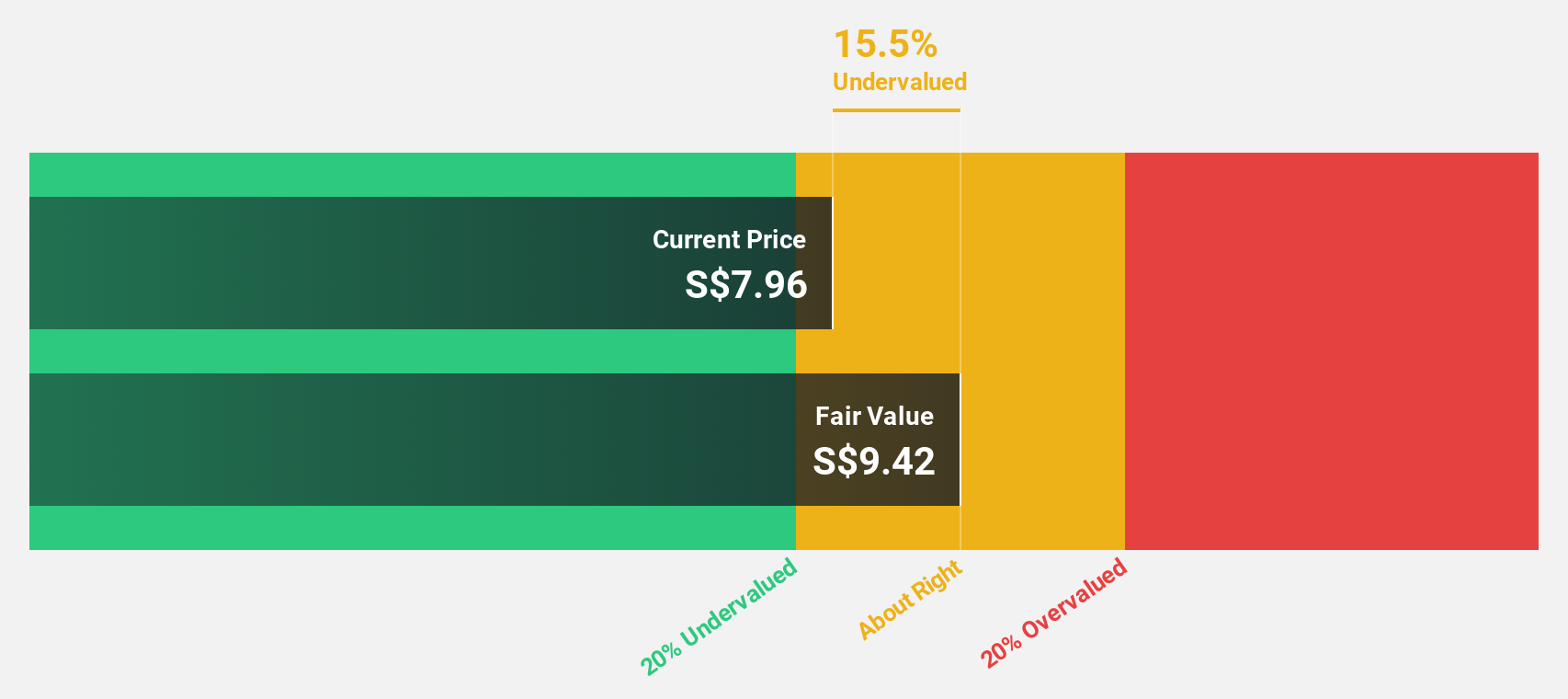

| Singapore Technologies Engineering (SGX:S63) | SGD4.71 | SGD7.30 | 35.5% |

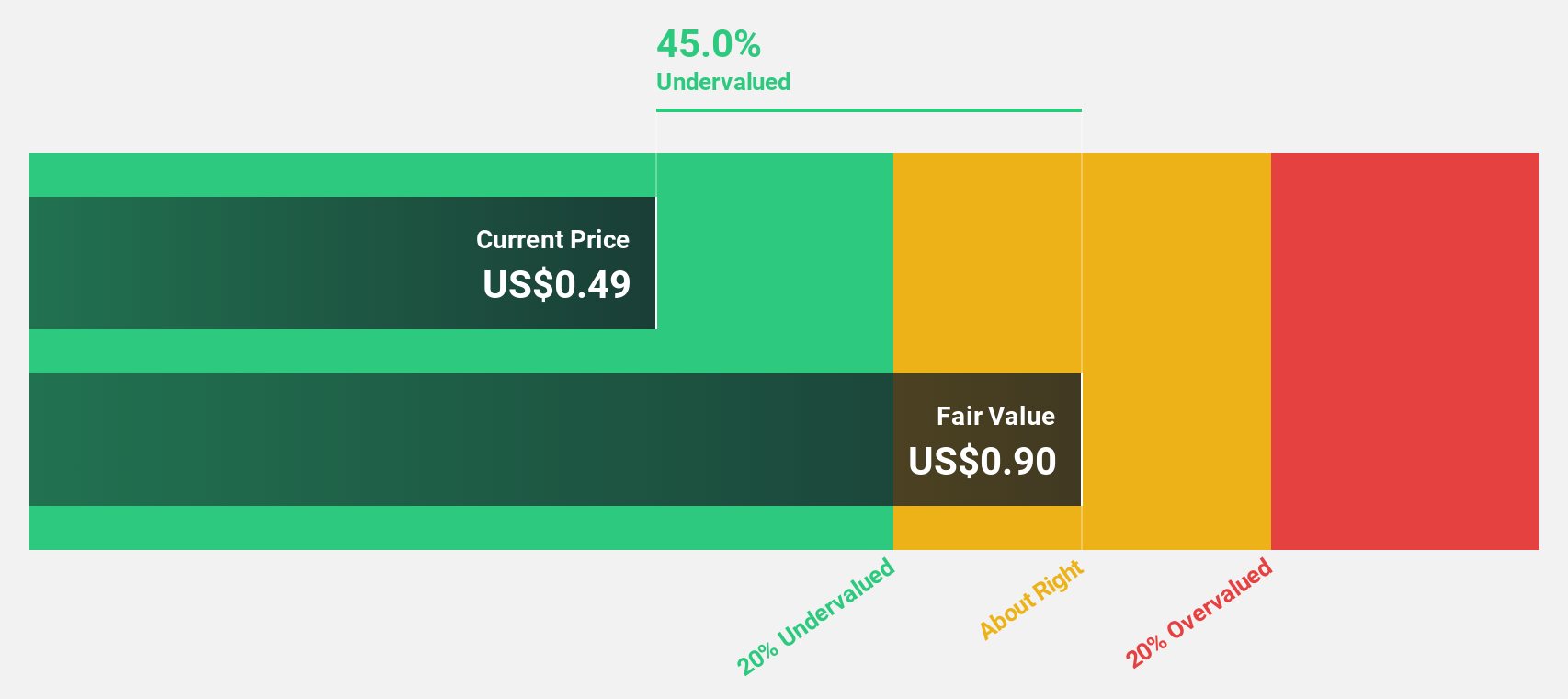

| Digital Core REIT (SGX:DCRU) | US$0.57 | US$0.81 | 29.8% |

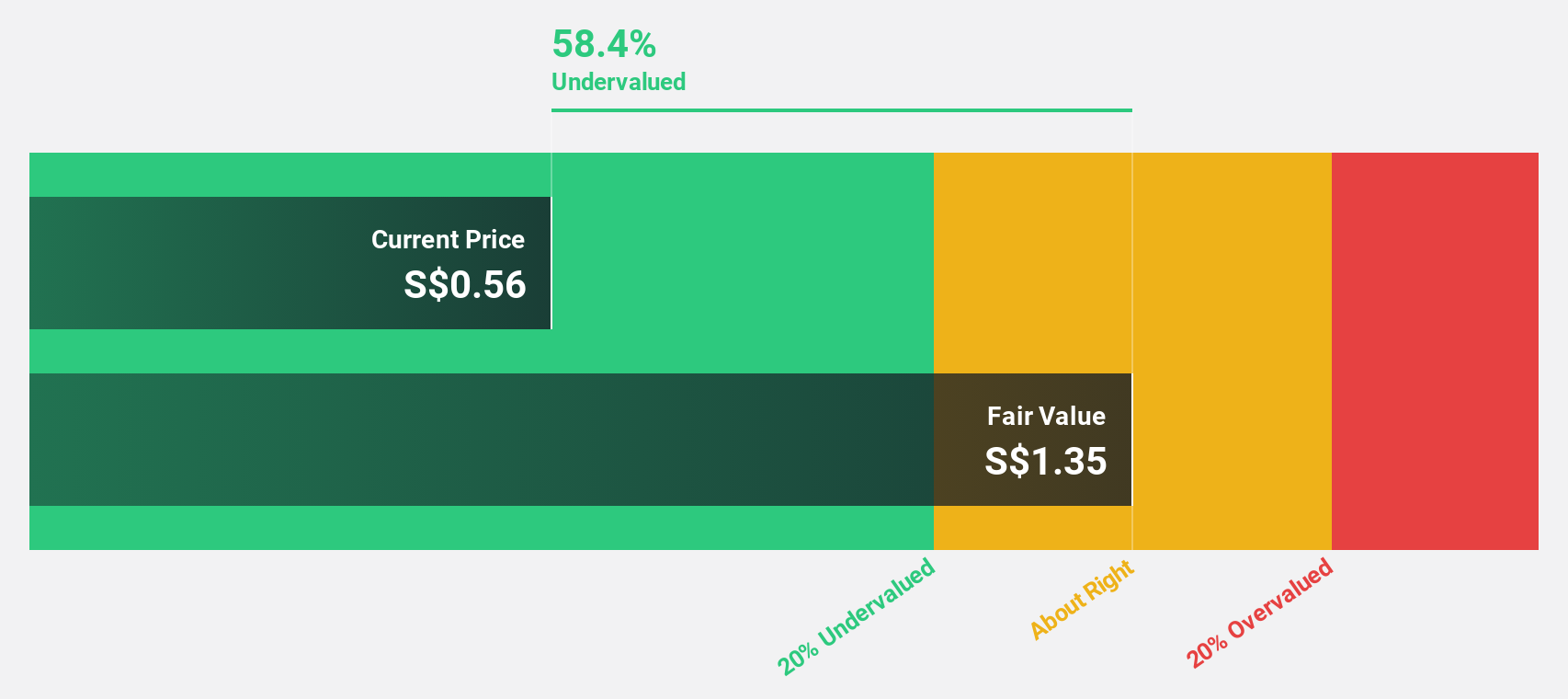

| Nanofilm Technologies International (SGX:MZH) | SGD0.83 | SGD1.42 | 41.7% |

| Seatrium (SGX:5E2) | SGD1.98 | SGD3.04 | 34.8% |

We'll examine a selection from our screener results.

Digital Core REIT (SGX:DCRU)

Overview: Digital Core REIT (SGX: DCRU) is a Singapore-listed pure-play data centre real estate investment trust sponsored by Digital Realty, with a market cap of $740.36 million.

Operations: The company's revenue is derived entirely from its commercial real estate investment trust segment, generating $70.76 million.

Estimated Discount To Fair Value: 29.8%

Digital Core REIT is trading at approximately 29.8% below its estimated fair value of US$0.81, suggesting it may be undervalued based on discounted cash flow analysis. Despite a recent decrease in revenue, net income nearly doubled to US$18.63 million for the half year ended June 30, 2024. While shareholders faced dilution last year and dividends decreased slightly, the company is forecasted to achieve above-average profit growth over the next three years with expected annual revenue growth of 12%.

- Upon reviewing our latest growth report, Digital Core REIT's projected financial performance appears quite optimistic.

- Delve into the full analysis health report here for a deeper understanding of Digital Core REIT.

Nanofilm Technologies International (SGX:MZH)

Overview: Nanofilm Technologies International Limited, with a market cap of SGD540.39 million, offers nanotechnology solutions across Singapore, China, Japan, and Vietnam.

Operations: The company's revenue is primarily derived from its Advanced Materials segment at SGD153.32 million, followed by Nanofabrication at SGD18.37 million, Industrial Equipment at SGD28.71 million, and Sydrogen contributing SGD1.40 million.

Estimated Discount To Fair Value: 41.7%

Nanofilm Technologies International is trading at 41.7% below its estimated fair value of SGD 1.42, indicating potential undervaluation based on discounted cash flow analysis. Despite a first-half net loss of SGD 3.74 million, the company anticipates second-half earnings to improve but remain below last year's figures. Revenue for the first half increased to SGD 82.65 million from the previous year, and future earnings are expected to grow significantly above market averages over the next three years.

- The analysis detailed in our Nanofilm Technologies International growth report hints at robust future financial performance.

- Get an in-depth perspective on Nanofilm Technologies International's balance sheet by reading our health report here.

Singapore Technologies Engineering (SGX:S63)

Overview: Singapore Technologies Engineering Ltd is a global technology, defence, and engineering company with a market cap of SGD14.68 billion.

Operations: The company's revenue is derived from three main segments: Commercial Aerospace (SGD4.34 billion), Urban Solutions & Satcom (SGD2.01 billion), and Defence & Public Security (SGD4.54 billion).

Estimated Discount To Fair Value: 35.5%

Singapore Technologies Engineering is trading at a substantial discount to its estimated fair value of S$7.30, with current shares priced at S$4.71. Despite debt concerns relative to operating cash flow, the company reported strong earnings growth of 19.9% over the past year and anticipates further growth outpacing the Singapore market. A recent strategic alliance in quantum security could enhance future revenue streams, although dividend stability remains uncertain.

- Our comprehensive growth report raises the possibility that Singapore Technologies Engineering is poised for substantial financial growth.

- Click here and access our complete balance sheet health report to understand the dynamics of Singapore Technologies Engineering.

Make It Happen

- Click here to access our complete index of 4 Undervalued SGX Stocks Based On Cash Flows.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com