Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalTake Care Before Jumping Onto Borneo Oil Berhad (KLSE:BORNOIL) Even Though It's 50% Cheaper

Borneo Oil Berhad (KLSE:BORNOIL) shareholders that were waiting for something to happen have been dealt a blow with a 50% share price drop in the last month. For any long-term shareholders, the last month ends a year to forget by locking in a 67% share price decline.

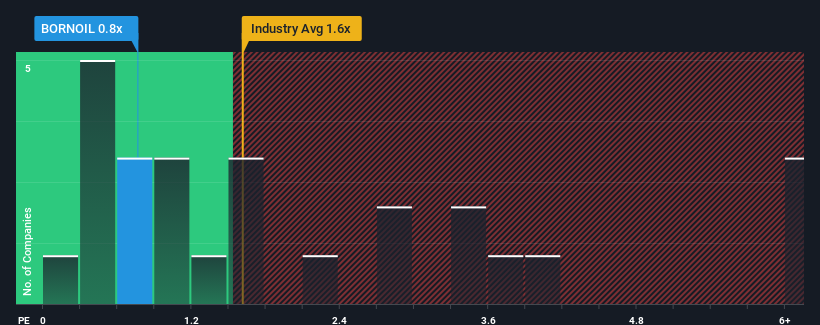

Following the heavy fall in price, Borneo Oil Berhad may be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.8x, since almost half of all companies in the Hospitality industry in Malaysia have P/S ratios greater than 1.4x and even P/S higher than 4x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for Borneo Oil Berhad

How Has Borneo Oil Berhad Performed Recently?

As an illustration, revenue has deteriorated at Borneo Oil Berhad over the last year, which is not ideal at all. One possibility is that the P/S is low because investors think the company won't do enough to avoid underperforming the broader industry in the near future. Those who are bullish on Borneo Oil Berhad will be hoping that this isn't the case so that they can pick up the stock at a lower valuation.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Borneo Oil Berhad will help you shine a light on its historical performance.Do Revenue Forecasts Match The Low P/S Ratio?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Borneo Oil Berhad's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 7.6% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 53% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

When compared to the industry's one-year growth forecast of 3.4%, the most recent medium-term revenue trajectory is noticeably more alluring

With this in mind, we find it intriguing that Borneo Oil Berhad's P/S isn't as high compared to that of its industry peers. It looks like most investors are not convinced the company can maintain its recent growth rates.

What We Can Learn From Borneo Oil Berhad's P/S?

Borneo Oil Berhad's recently weak share price has pulled its P/S back below other Hospitality companies. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We're very surprised to see Borneo Oil Berhad currently trading on a much lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. Potential investors that are sceptical over continued revenue performance may be preventing the P/S ratio from matching previous strong performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to perceive a likelihood of revenue fluctuations in the future.

Having said that, be aware Borneo Oil Berhad is showing 2 warning signs in our investment analysis, and 1 of those is a bit concerning.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.