Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalThe Return Trends At Iljeong IndustrialLtd (KRX:008500) Look Promising

What are the early trends we should look for to identify a stock that could multiply in value over the long term? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. So when we looked at Iljeong IndustrialLtd (KRX:008500) and its trend of ROCE, we really liked what we saw.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Iljeong IndustrialLtd:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.13 = ₩2.1b ÷ (₩34b - ₩18b) (Based on the trailing twelve months to June 2024).

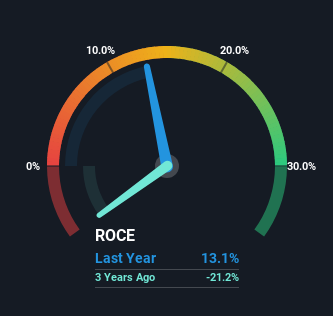

So, Iljeong IndustrialLtd has an ROCE of 13%. In absolute terms, that's a satisfactory return, but compared to the Luxury industry average of 7.3% it's much better.

Check out our latest analysis for Iljeong IndustrialLtd

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Iljeong IndustrialLtd.

How Are Returns Trending?

We're delighted to see that Iljeong IndustrialLtd is reaping rewards from its investments and has now broken into profitability. Historically the company was generating losses but as we can see from the latest figures referenced above, they're now earning 13% on their capital employed. At first glance, it seems the business is getting more proficient at generating returns, because over the same period, the amount of capital employed has reduced by 59%. This could potentially mean that the company is selling some of its assets.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. The current liabilities has increased to 53% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. And with current liabilities at those levels, that's pretty high.

Our Take On Iljeong IndustrialLtd's ROCE

In a nutshell, we're pleased to see that Iljeong IndustrialLtd has been able to generate higher returns from less capital. And since the stock has fallen 32% over the last five years, there might be an opportunity here. So researching this company further and determining whether or not these trends will continue seems justified.

Iljeong IndustrialLtd does come with some risks though, we found 2 warning signs in our investment analysis, and 1 of those doesn't sit too well with us...

While Iljeong IndustrialLtd isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.