Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 US Growth Stocks With High Insider Ownership And Earnings Growth Up To 61%

As the U.S. stock market continues to reach new heights, driven by strong performances in sectors like semiconductors and artificial intelligence, investors are increasingly focused on growth opportunities with robust fundamentals. In this environment, companies with high insider ownership and significant earnings growth potential can be particularly attractive, as they often indicate strong alignment between management and shareholder interests.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 41.9% |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.4% |

| GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 26% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 33.2% |

| Super Micro Computer (NasdaqGS:SMCI) | 25.7% | 28.0% |

| Hims & Hers Health (NYSE:HIMS) | 13.7% | 37.4% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.0% | 95% |

| Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

| BBB Foods (NYSE:TBBB) | 22.9% | 51.2% |

We're going to check out a few of the best picks from our screener tool.

Liquidia (NasdaqCM:LQDA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Liquidia Corporation is a biopharmaceutical company that develops, manufactures, and commercializes products addressing unmet patient needs in the United States, with a market cap of $981.32 million.

Operations: Revenue Segments (in millions of $): Liquidia generates revenue primarily from its Pharmaceuticals segment, amounting to $14.84 million.

Insider Ownership: 10.6%

Earnings Growth Forecast: 57.5% p.a.

Liquidia is positioned as a growth company with significant insider ownership, evidenced by substantial insider buying over the past three months. The company's revenue is forecast to grow at 57% annually, outpacing the US market average. Despite recent shareholder dilution and volatile share prices, Liquidia's strategic expansion through an amended licensing agreement with Pharmosa Biopharm enhances its market reach. The expected profitability within three years and favorable clinical trial data for L606 support its growth trajectory.

- Unlock comprehensive insights into our analysis of Liquidia stock in this growth report.

- Our valuation report unveils the possibility Liquidia's shares may be trading at a premium.

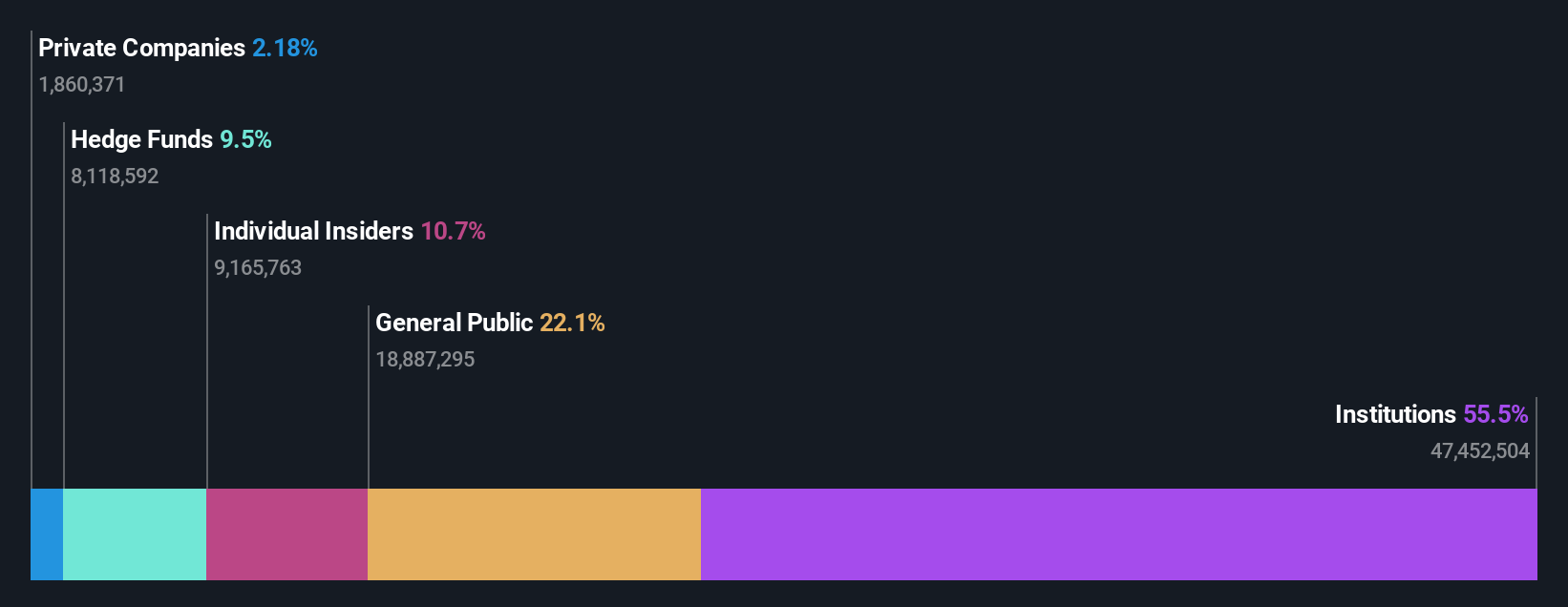

GigaCloud Technology (NasdaqGM:GCT)

Simply Wall St Growth Rating: ★★★★★★

Overview: GigaCloud Technology Inc. offers comprehensive B2B ecommerce solutions for large parcel merchandise both in the United States and internationally, with a market cap of approximately $1.02 billion.

Operations: The company's revenue primarily comes from its online retailers segment, which generated $984.85 million.

Insider Ownership: 25.7%

Earnings Growth Forecast: 26% p.a.

GigaCloud Technology's growth prospects are underscored by its inclusion in major indices and a robust earnings report, with revenue reaching US$310.87 million in Q2 2024. The company anticipates continued revenue growth of over 20% annually, surpassing the US market average. Despite recent executive changes and share price volatility, GigaCloud is executing a US$46 million share repurchase program, leveraging its strong cash position to enhance shareholder value while trading significantly below estimated fair value.

- Click here to discover the nuances of GigaCloud Technology with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential undervaluation of GigaCloud Technology shares in the market.

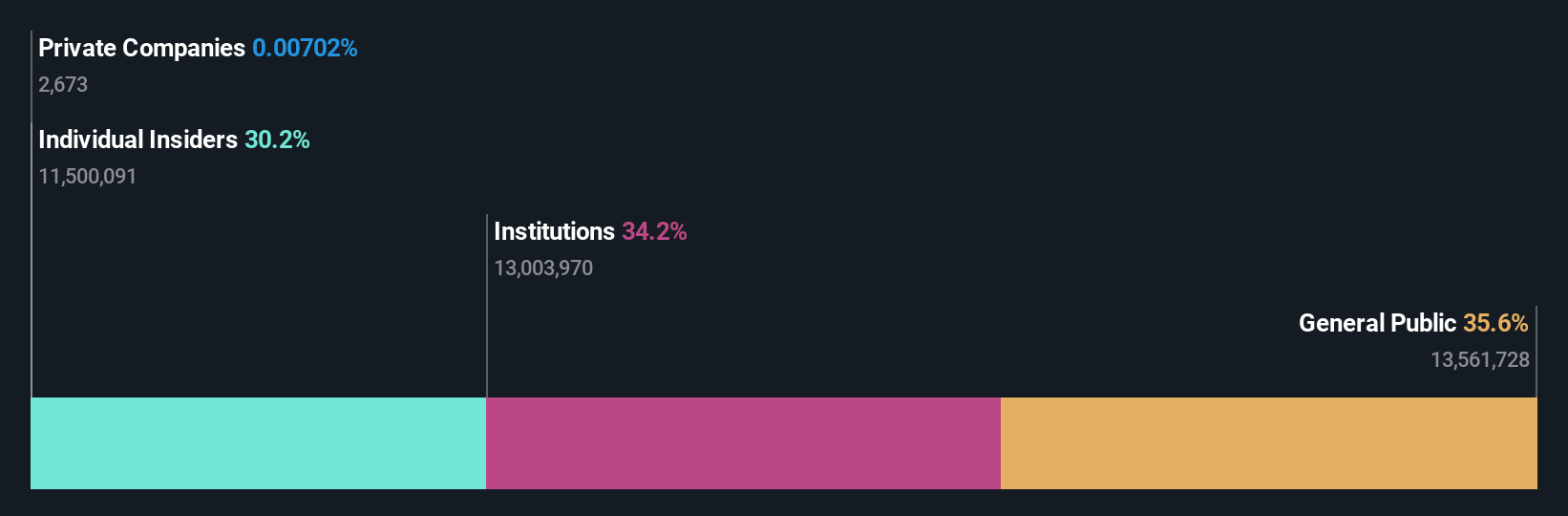

Toast (NYSE:TOST)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Toast, Inc. provides a cloud-based digital technology platform for the restaurant industry across the United States, Ireland, and India with a market cap of approximately $16.31 billion.

Operations: The company generates revenue of $4.39 billion from its data processing segment, serving the restaurant industry across multiple countries.

Insider Ownership: 21.2%

Earnings Growth Forecast: 61% p.a.

Toast's growth potential is highlighted by its recent product innovations, including a Branded Mobile App aimed at enhancing restaurant engagement and revenue. The company's Q2 2024 revenue reached US$1.24 billion, with a net income of US$14 million, marking a turnaround from the previous year's loss. Forecasts suggest Toast will become profitable within three years, with expected annual profit growth above market averages and revenue growth outpacing the broader US market.

- Dive into the specifics of Toast here with our thorough growth forecast report.

- Upon reviewing our latest valuation report, Toast's share price might be too optimistic.

Turning Ideas Into Actions

- Explore the 188 names from our Fast Growing US Companies With High Insider Ownership screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com