Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalNextEra Energy (NYSE:NEE) Seems To Be Using A Lot Of Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that NextEra Energy, Inc. (NYSE:NEE) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for NextEra Energy

How Much Debt Does NextEra Energy Carry?

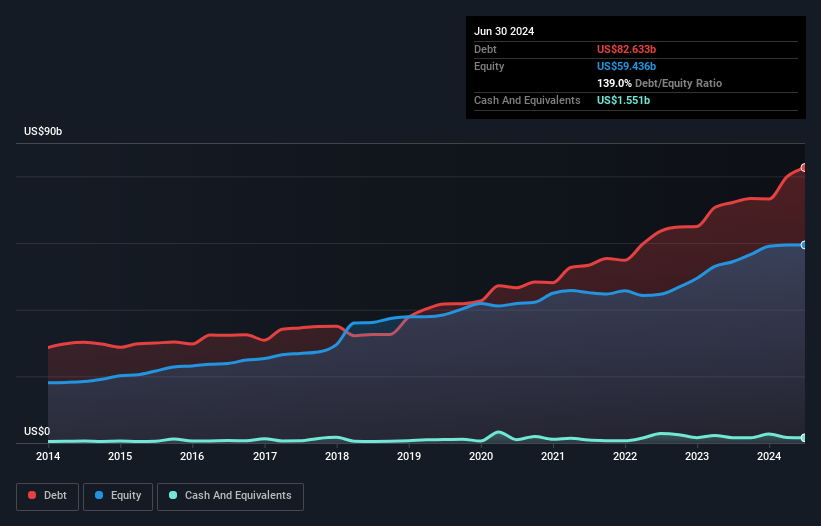

You can click the graphic below for the historical numbers, but it shows that as of June 2024 NextEra Energy had US$82.6b of debt, an increase on US$72.2b, over one year. Net debt is about the same, since the it doesn't have much cash.

How Healthy Is NextEra Energy's Balance Sheet?

We can see from the most recent balance sheet that NextEra Energy had liabilities of US$26.2b falling due within a year, and liabilities of US$99.1b due beyond that. On the other hand, it had cash of US$1.55b and US$6.17b worth of receivables due within a year. So it has liabilities totalling US$117.6b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its very significant market capitalization of US$173.5b, so it does suggest shareholders should keep an eye on NextEra Energy's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

NextEra Energy has a rather high debt to EBITDA ratio of 5.8 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 2.5 times, suggesting it can responsibly service its obligations. Another concern for investors might be that NextEra Energy's EBIT fell 16% in the last year. If that's the way things keep going handling the debt load will be like delivering hot coffees on a pogo stick. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine NextEra Energy's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, NextEra Energy burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both NextEra Energy's net debt to EBITDA and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. And even its interest cover fails to inspire much confidence. We should also note that Electric Utilities industry companies like NextEra Energy commonly do use debt without problems. Overall, it seems to us that NextEra Energy's balance sheet is really quite a risk to the business. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for NextEra Energy (1 is potentially serious) you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.