Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalHigh Growth Tech Stocks In Hong Kong To Watch

As global markets experience a mix of highs and lows, with U.S. indices reaching record levels amidst inflation concerns and cautious central bank policies, Hong Kong's tech sector faces its own set of challenges and opportunities. In this dynamic environment, identifying high growth tech stocks involves looking for companies that demonstrate resilience through innovation, adaptability to market changes, and strong fundamentals that align with the evolving economic landscape.

Top 10 High Growth Tech Companies In Hong Kong

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Wasion Holdings | 22.37% | 25.47% | ★★★★★☆ |

| MedSci Healthcare Holdings | 48.74% | 48.78% | ★★★★★☆ |

| Inspur Digital Enterprise Technology | 25.31% | 39.04% | ★★★★★☆ |

| RemeGen | 26.30% | 52.19% | ★★★★★☆ |

| Cowell e Holdings | 31.68% | 35.44% | ★★★★★★ |

| Innovent Biologics | 21.74% | 59.60% | ★★★★★☆ |

| Akeso | 33.46% | 53.03% | ★★★★★★ |

| Biocytogen Pharmaceuticals (Beijing) | 21.53% | 109.17% | ★★★★★☆ |

| Beijing Airdoc Technology | 37.47% | 93.35% | ★★★★★☆ |

| Sichuan Kelun-Biotech Biopharmaceutical | 24.70% | 8.53% | ★★★★★☆ |

Click here to see the full list of 43 stocks from our SEHK High Growth Tech and AI Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

Kingboard Laminates Holdings (SEHK:1888)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kingboard Laminates Holdings Limited is an investment holding company that manufactures and sells laminates across the People's Republic of China, Europe, other Asian countries, and the United States with a market capitalization of HK$20.90 billion.

Operations: Kingboard Laminates Holdings derives the majority of its revenue from the laminates segment, contributing HK$17.06 billion, while its properties and investments segments contribute significantly less at HK$121.11 million and HK$99.14 million respectively.

Kingboard Laminates Holdings has demonstrated a robust financial performance, with its recent half-year earnings showing a significant increase in net income to HKD 727.8 million from HKD 422.24 million year-over-year, propelled by a strong market demand that boosted sales volumes. Its strategic vertical integration model further solidifies its market position, contributing to an anticipated annual profit growth of 33.3%. Despite these gains, the company's revenue growth projection of 12.2% trails the more aggressive industry benchmarks. However, this steady growth coupled with a recent dividend increase suggests a balanced approach to shareholder returns and reinvestment in business operations.

Lenovo Group (SEHK:992)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lenovo Group Limited is an investment holding company that develops, manufactures, and markets technology products and services, with a market cap of HK$136.45 billion.

Operations: The company's revenue is primarily driven by the Intelligent Devices Group (IDG), contributing $45.76 billion, followed by the Infrastructure Solutions Group (ISG) at $10.17 billion, and the Solutions and Services Group (SSG) at $7.64 billion.

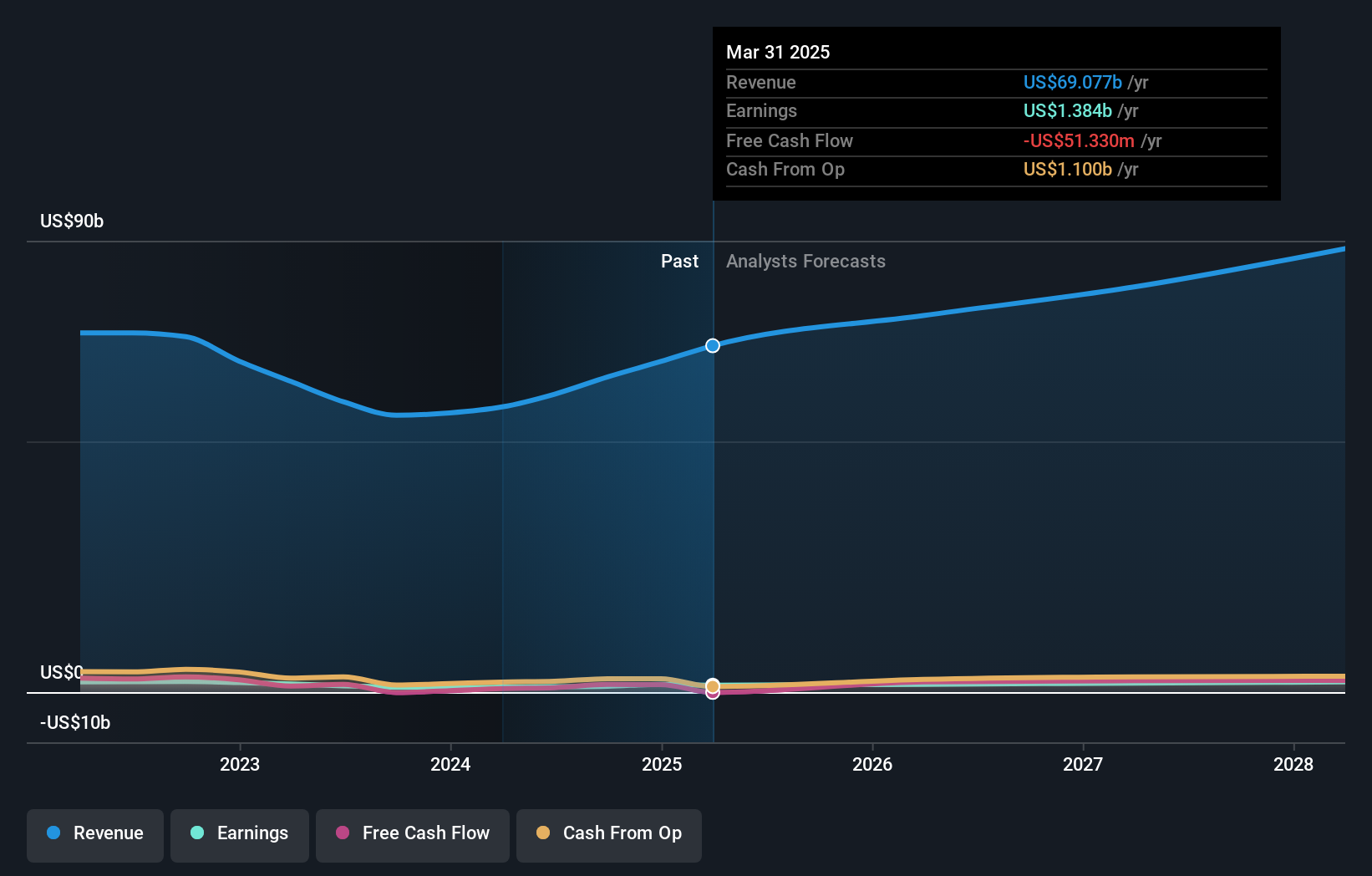

Lenovo Group is capitalizing on the escalating demand for AI and high-performance computing solutions, evidenced by their recent collaboration with Red Hat to integrate RHEL AI on ThinkSystem servers, enhancing AI model development capabilities. This partnership underscores Lenovo's commitment to innovation, aligning with an 18.8% forecasted annual earnings growth and a strategic focus on R&D that has seen expenses rise significantly to support these advanced tech initiatives. Additionally, their involvement in creating Alzheimer’s Intelligence—a 3D avatar for dementia support—highlights their pioneering role in applying AI to healthcare, further diversifying their technological impact while expecting revenue growth of 7.9%. These ventures not only enhance Lenovo's product offerings but also position them favorably within the competitive tech landscape of Hong Kong.

- Click here and access our complete health analysis report to understand the dynamics of Lenovo Group.

Evaluate Lenovo Group's historical performance by accessing our past performance report.

Akeso (SEHK:9926)

Simply Wall St Growth Rating: ★★★★★★

Overview: Akeso, Inc. is a biopharmaceutical company that focuses on the research, development, manufacturing, and commercialization of antibody drugs with a market cap of HK$57.06 billion.

Operations: Akeso generates revenue primarily through the research, development, production, and sale of biopharmaceutical products, amounting to CN¥1.87 billion.

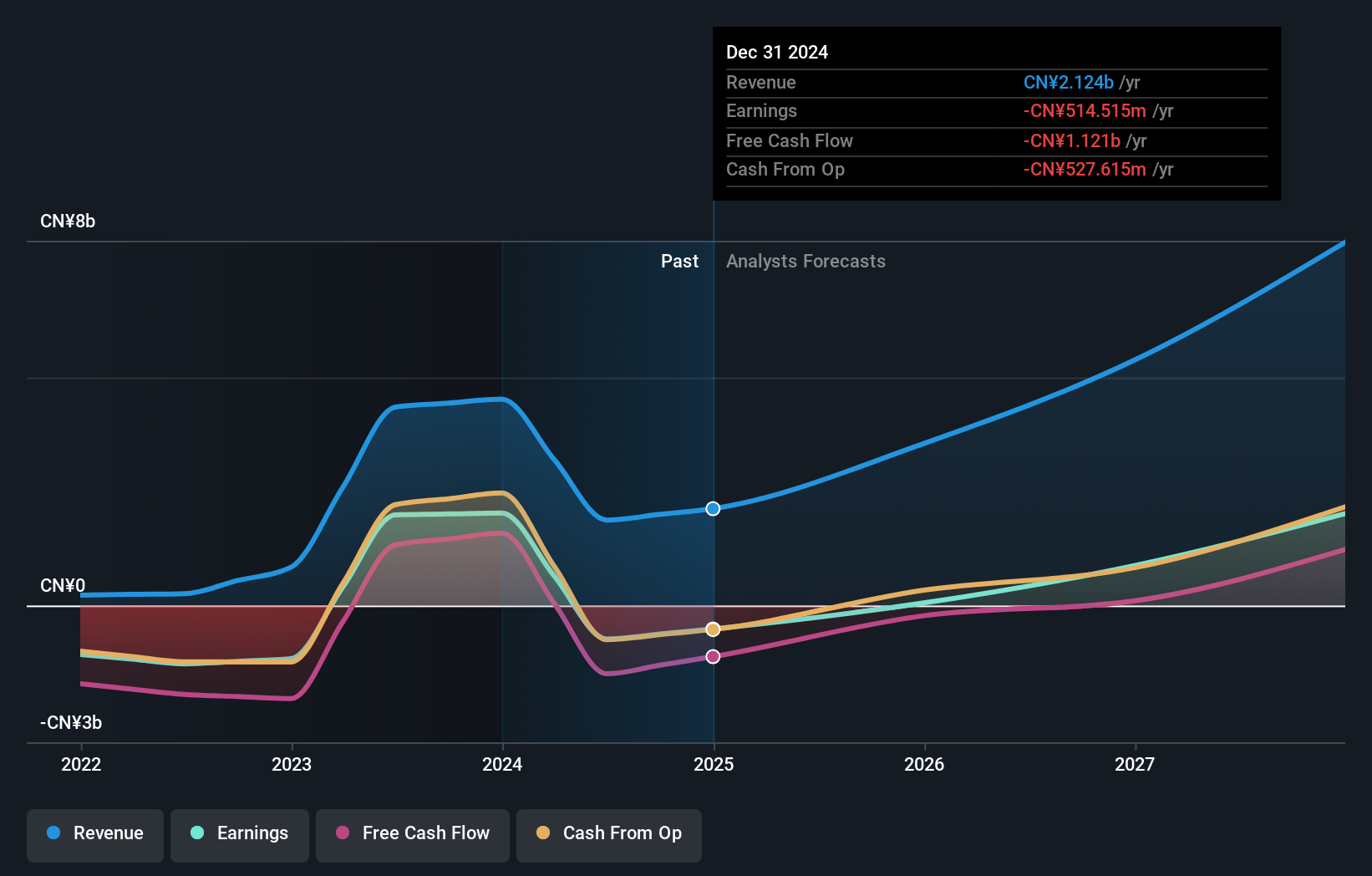

Akeso's recent strides in biopharmaceutical innovation, particularly with its PD-1/CTLA-4 bispecific antibody, cadonilimab, underscore its potential within high-growth tech sectors in Hong Kong. The company announced significant clinical benefits from its COMPASSION-16 study for cervical cancer treatment, showing a 33.5% annual revenue growth rate and forecasting earnings to surge by 53.0% annually. These developments highlight Akeso's robust R&D commitment—evidenced by substantial investment in research that aligns with projected market demands and patient needs, positioning it well for future advancements in oncology therapy.

- Take a closer look at Akeso's potential here in our health report.

Assess Akeso's past performance with our detailed historical performance reports.

Key Takeaways

- Access the full spectrum of 43 SEHK High Growth Tech and AI Stocks by clicking on this link.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com