Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalExploring Caisse Régionale de Crédit Agricole Mutuel d'Ille-et-Vilaine Société Coopérative and 2 Promising French Small Caps

As the pan-European STOXX Europe 600 Index experiences a modest rise, buoyed by hopes of quicker interest rate cuts from the European Central Bank and potential economic stimulus from China, attention turns to France's small-cap market as a fertile ground for investment opportunities. In this environment, discerning investors often seek stocks with strong fundamentals and growth potential, such as Caisse Régionale de Crédit Agricole Mutuel d'Ille-et-Vilaine Société Coopérative and other promising French small caps.

Top 10 Undiscovered Gems With Strong Fundamentals In France

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Caisse Régionale de Crédit Agricole Mutuel Brie Picardie Société coopérative | 34.89% | 3.23% | 3.61% | ★★★★★★ |

| Caisse Régionale de Crédit Agricole Mutuel Nord de France Société coopérative | 10.84% | 3.22% | 6.38% | ★★★★★★ |

| EssoF | 1.19% | 11.14% | 41.41% | ★★★★★★ |

| Caisse régionale de Crédit Agricole Mutuel d'Ille-et-Vilaine Société coopérative | 12.60% | 7.75% | 11.53% | ★★★★★★ |

| ADLPartner | 82.84% | 9.86% | 16.18% | ★★★★★☆ |

| VIEL & Cie société anonyme | 54.02% | 5.66% | 19.86% | ★★★★★☆ |

| Caisse Regionale de Credit Agricole Mutuel Toulouse 31 | 14.94% | 0.59% | 5.95% | ★★★★★☆ |

| La Forestière Equatoriale | 0.00% | -50.76% | 49.41% | ★★★★★☆ |

| Caisse Régionale de Crédit Agricole Mutuel Alpes Provence Société coopérative | 391.01% | 4.67% | 17.31% | ★★★★☆☆ |

| Société Fermière du Casino Municipal de Cannes | 11.60% | 6.69% | 10.30% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

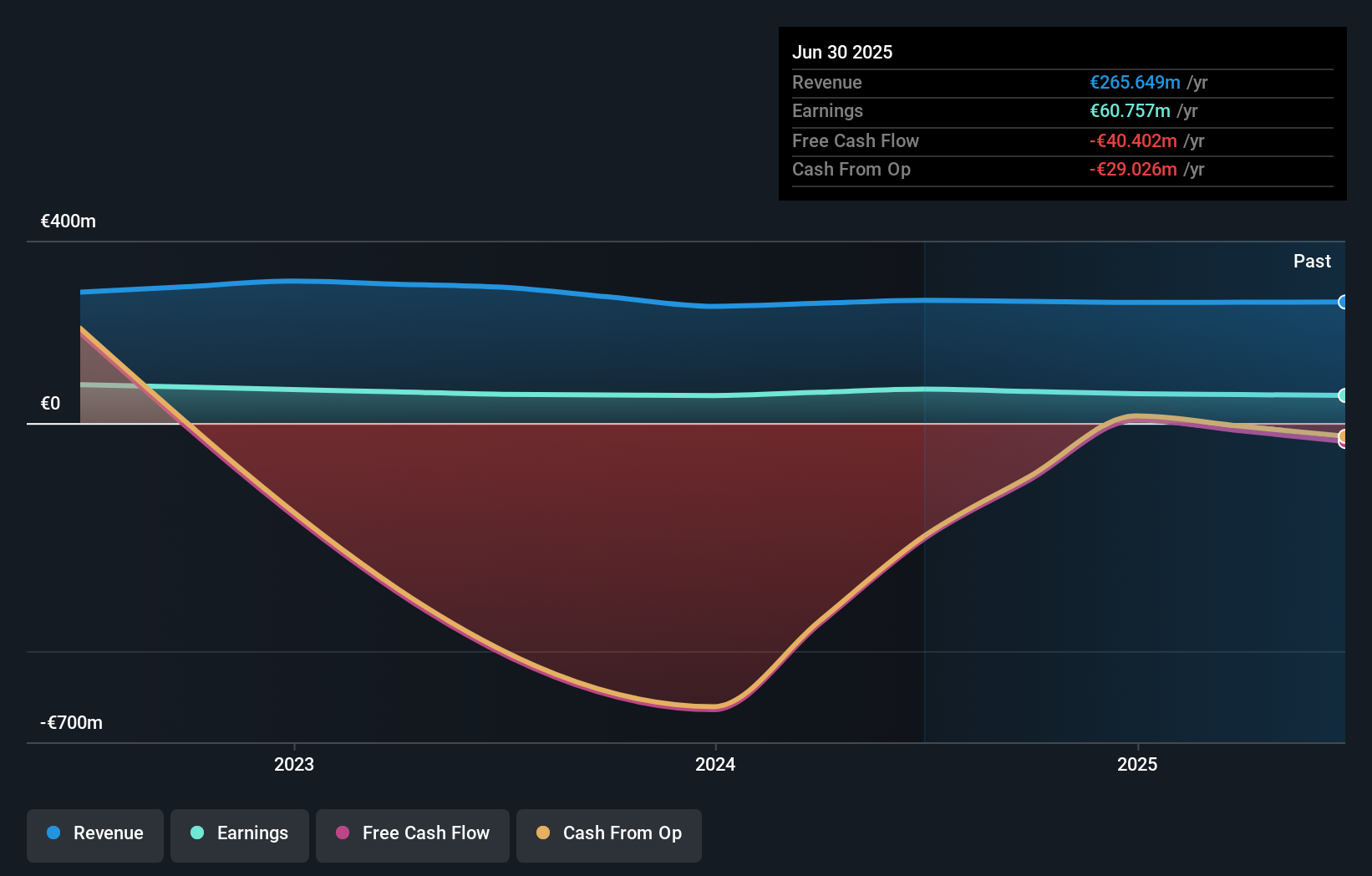

Caisse régionale de Crédit Agricole Mutuel d'Ille-et-Vilaine Société coopérative (ENXTPA:CIV)

Simply Wall St Value Rating: ★★★★★★

Overview: Caisse régionale de Crédit Agricole Mutuel d'Ille-et-Vilaine Société coopérative is a French cooperative bank offering a range of banking services, with a market capitalization of approximately €343.49 million.

Operations: The cooperative bank generates revenue primarily from its retail banking segment, amounting to €299.55 million.

Caisse régionale de Crédit Agricole Mutuel d'Ille-et-Vilaine, with total assets of €20.2 billion and equity of €2.3 billion, is a notable player in the French banking sector. Total deposits and loans both stand at €16.7 billion, reflecting balanced financial management. The bank's earnings grew by 17.9%, outpacing the industry average of 4%. Additionally, it has a sufficient allowance for bad loans at 123% and maintains low-risk funding with customer deposits accounting for 93% of liabilities.

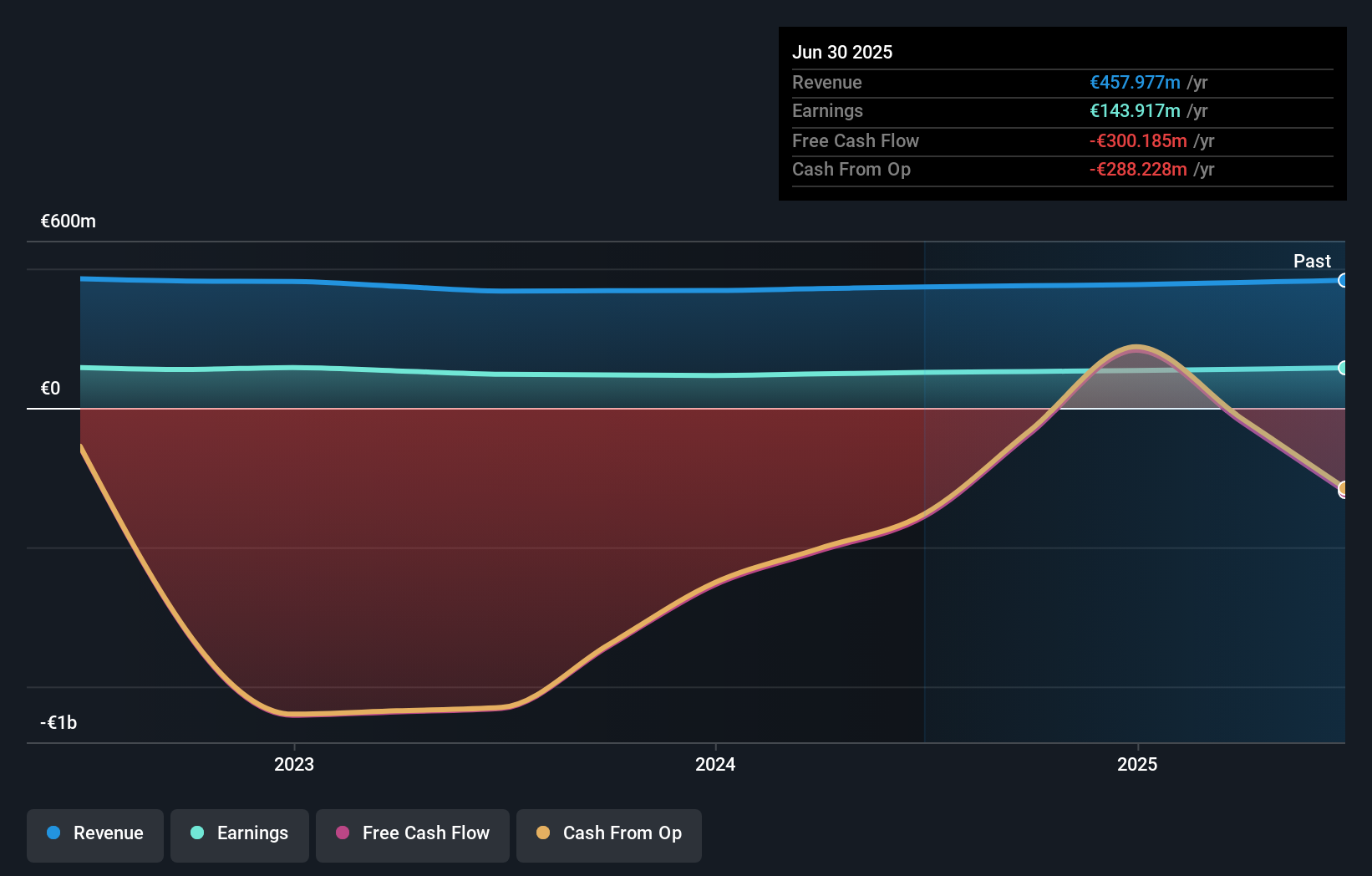

Caisse Régionale de Crédit Agricole Mutuel Alpes Provence Société coopérative (ENXTPA:CRAP)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Caisse Régionale de Crédit Agricole Mutuel Alpes Provence Société coopérative offers a range of banking products and services in France, with a market capitalization of €546.69 million.

Operations: The company generates revenue primarily from its retail banking segment, amounting to approximately €434.27 million.

Caisse Régionale de Crédit Agricole Mutuel Alpes Provence shows potential with total assets of €26.2 billion and equity at €3.3 billion, while trading 68.6% below its estimated fair value. Total loans stand at €18.8 billion, supported by a sufficient bad loan allowance of 109%. Despite having 61% of liabilities from higher-risk funding sources, earnings growth over the past year reached 5.3%, surpassing the industry average of 4%.

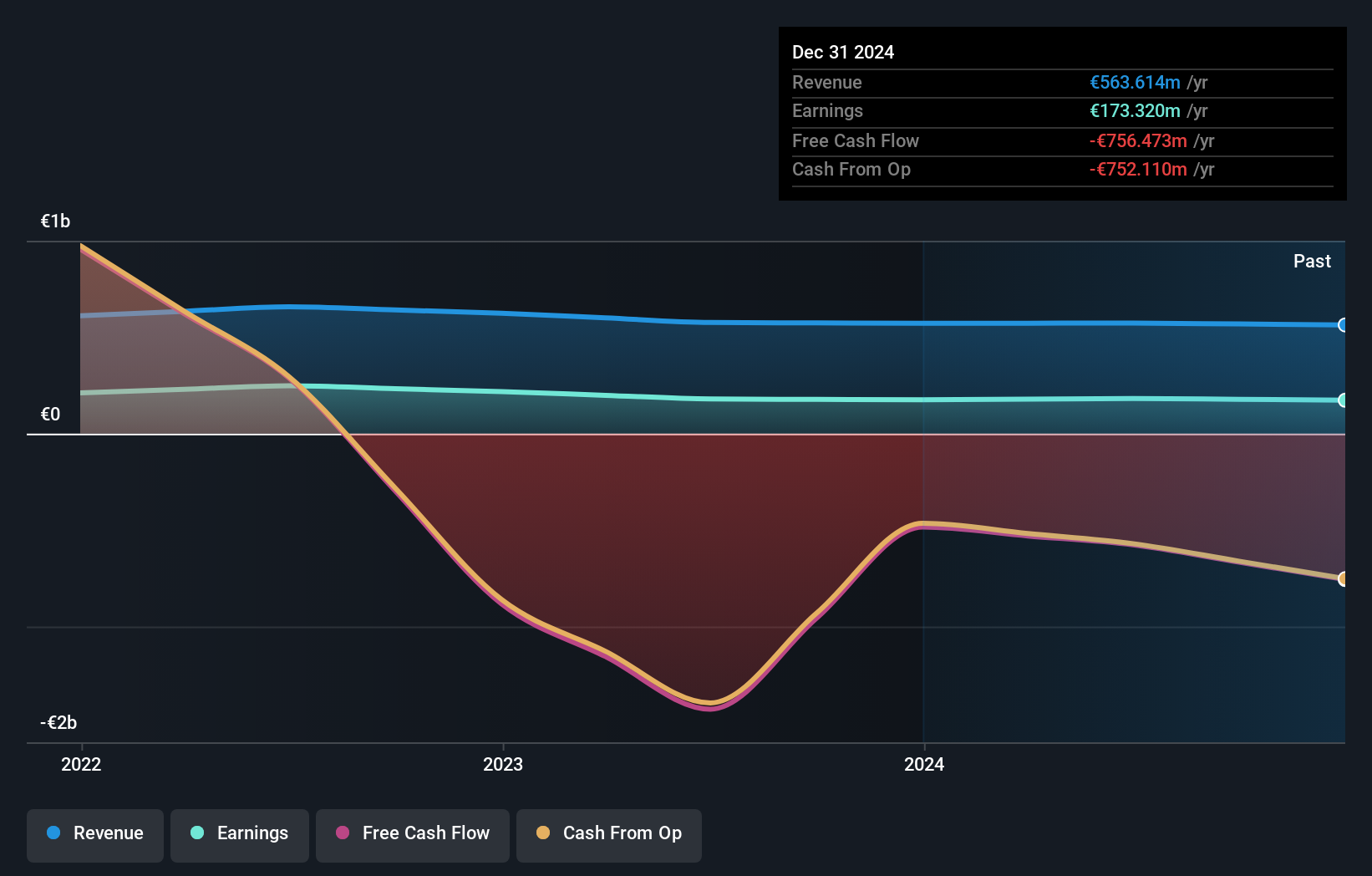

Caisse Régionale de Crédit Agricole Mutuel du Languedoc Société coopérative (ENXTPA:CRLA)

Simply Wall St Value Rating: ★★★★★★

Overview: Caisse Régionale de Crédit Agricole Mutuel du Languedoc Société coopérative offers a range of banking products and services to diverse client groups in France, with a market cap of €919.62 million.

Operations: The company generates revenue primarily through its diverse banking products and services aimed at individuals, professionals, farmers, businesses, and community clients in France. It operates with a market cap of €919.62 million.

CRLA, with total assets of €35.3 billion and equity of €5.2 billion, stands out for its prudent financial management. Total loans amount to €29 billion against deposits of €28.2 billion, showcasing a robust lending framework. The bank's allowance for bad loans is sufficient at 133%, and non-performing loans are low at 1.4%. Despite trading significantly below fair value estimates by 68.6%, earnings growth has been modest at 4.2% annually over five years, reflecting steady but cautious expansion in a competitive industry landscape.

Key Takeaways

- Discover the full array of 38 Euronext Paris Undiscovered Gems With Strong Fundamentals right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com