Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalUndiscovered Gems in Switzerland for October 2024

The Swiss market has experienced a rollercoaster session, with the SMI index fluctuating before closing slightly down, reflecting broader uncertainties and mixed performances among key players like VAT Group and Tecan Group. In such an environment, identifying promising small-cap stocks requires a keen focus on resilience and growth potential amidst economic challenges.

Top 10 Undiscovered Gems With Strong Fundamentals In Switzerland

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| IVF Hartmann Holding | NA | 0.24% | 0.63% | ★★★★★★ |

| TX Group | 0.93% | -1.67% | 7.21% | ★★★★★★ |

| naturenergie holding | NA | 17.32% | 34.71% | ★★★★★★ |

| Datacolor | NA | 3.59% | 30.14% | ★★★★★★ |

| Elma Electronic | 36.60% | 3.13% | 3.10% | ★★★★★★ |

| Compagnie Financière Tradition | 47.15% | 1.91% | 11.44% | ★★★★★☆ |

| Vaudoise Assurances Holding | NA | 1.52% | 1.85% | ★★★★★☆ |

| Procimmo Group | 157.49% | 0.65% | 4.94% | ★★★★☆☆ |

| lastminute.com | 42.65% | 4.93% | 3.11% | ★★★★☆☆ |

| Bergbahnen Engelberg-Trübsee-Titlis | 3.00% | -10.81% | -16.31% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

Burkhalter Holding (SWX:BRKN)

Simply Wall St Value Rating: ★★★★☆☆

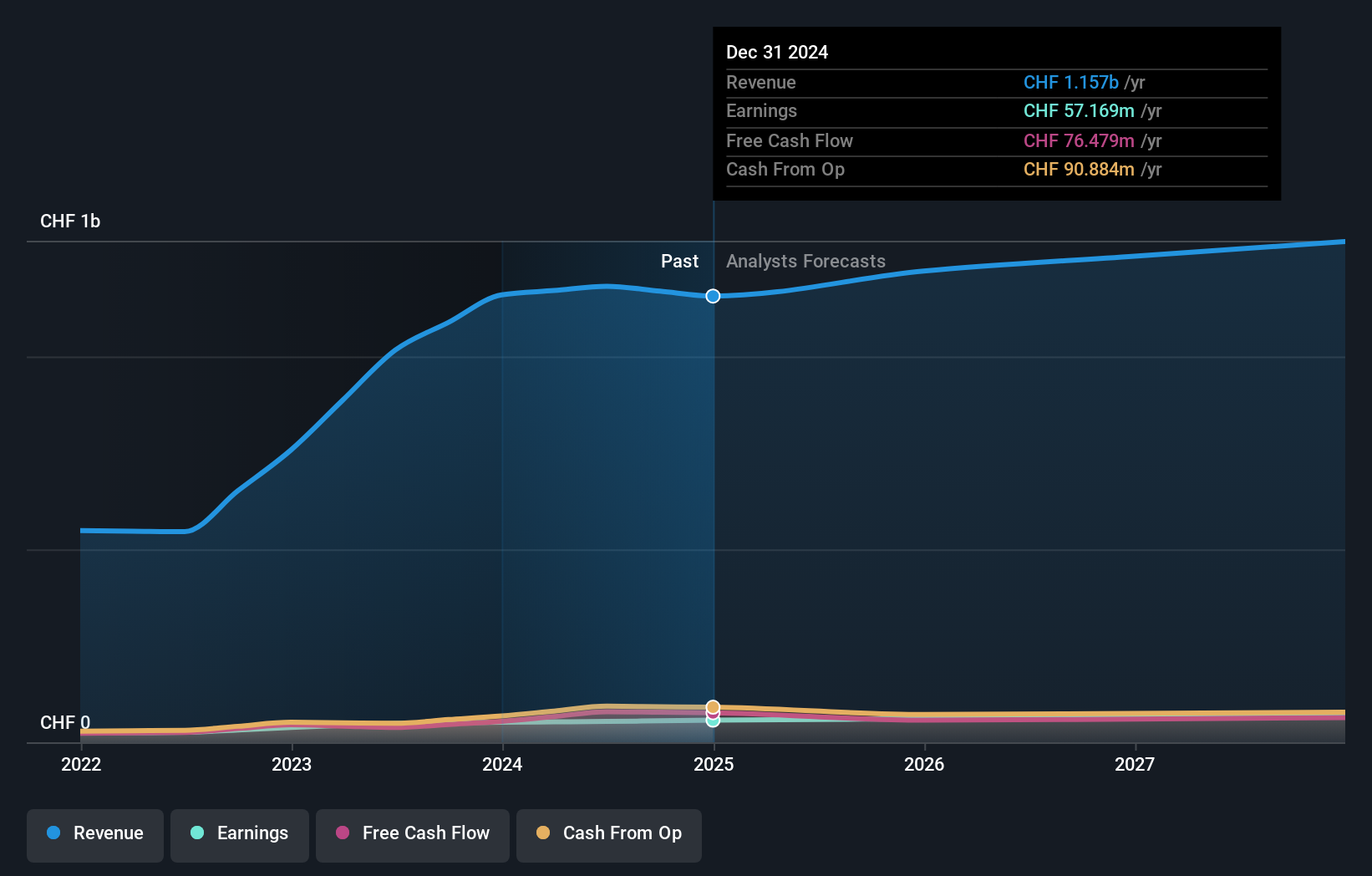

Overview: Burkhalter Holding AG, with a market cap of CHF974.44 million, operates through its subsidiaries to deliver electrical engineering services to the construction sector in Switzerland.

Operations: Burkhalter Holding AG generates revenue primarily from its electrical engineering services, amounting to CHF1.18 billion. The company's financial data highlights a focus on maintaining efficient operations, as reflected in its cost management strategies.

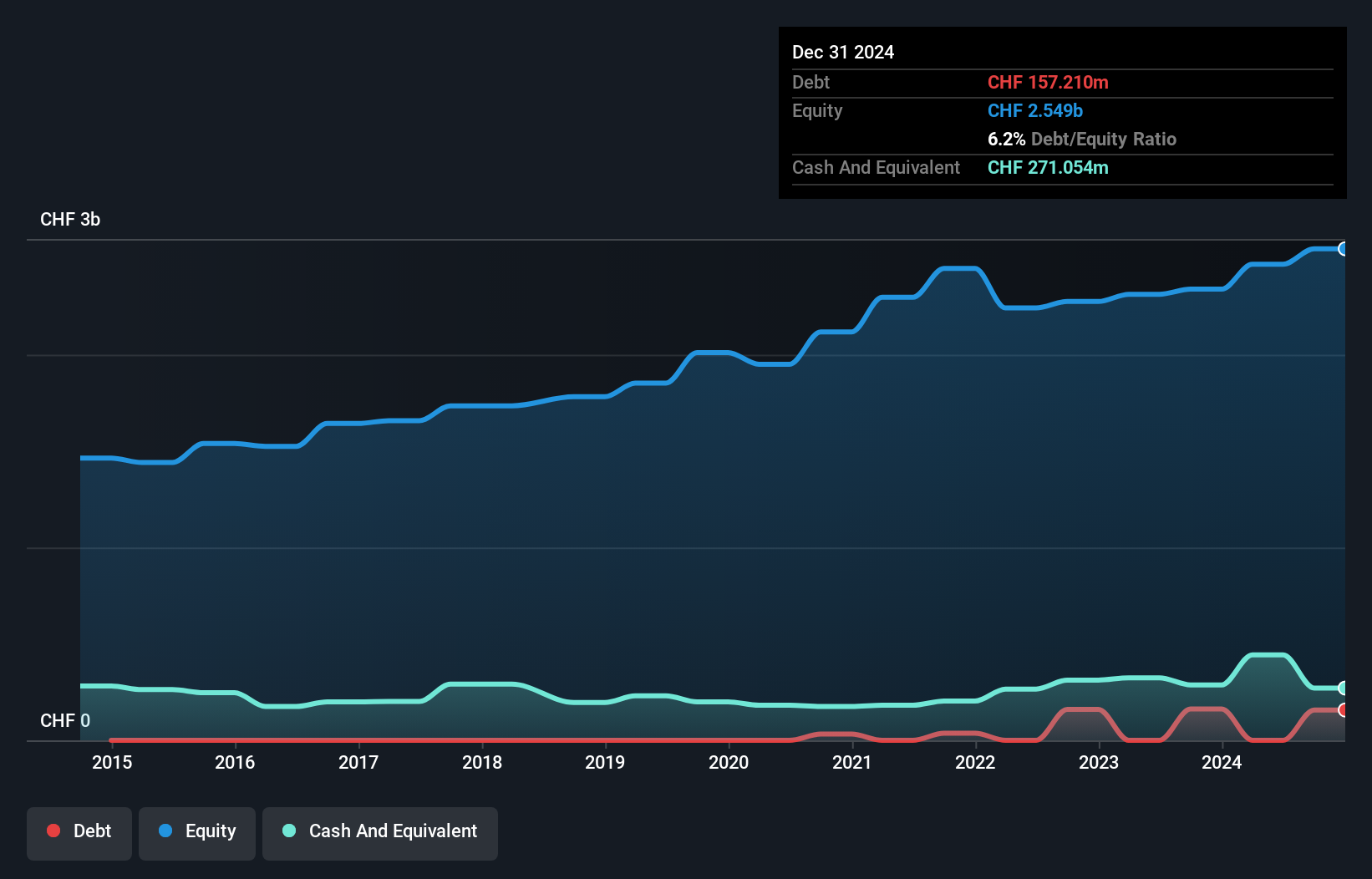

Burkhalter Holding, a Swiss construction player, reported half-year revenue of CHF 570.3 million, up from CHF 529.27 million last year, with net income rising to CHF 23.3 million. Basic earnings per share improved to CHF 2.19 from CHF 2.04. Despite a high net debt to equity ratio of 52.9%, the company enjoys robust interest coverage at 46 times EBIT and trades at a slight discount to its estimated fair value by about 4.7%.

- Get an in-depth perspective on Burkhalter Holding's performance by reading our health report here.

Assess Burkhalter Holding's past performance with our detailed historical performance reports.

Vaudoise Assurances Holding (SWX:VAHN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Vaudoise Assurances Holding SA is a Swiss company offering insurance products and services, with a market capitalization of CHF1.35 billion.

Operations: Vaudoise Assurances Holding generates revenue through its insurance products and services in Switzerland, with a market capitalization of CHF1.35 billion.

Vaudoise Assurances Holding, a Swiss insurer, is currently trading at 65% below its estimated fair value. With no debt on its balance sheet for the past five years, it has been able to focus on growth and quality earnings. The company's recent half-year earnings report shows net income of CHF 81 million, up from CHF 70 million last year. Its earnings growth of 7.1% surpassed the industry average of 6.7%, reflecting strong performance in a competitive market.

V-ZUG Holding (SWX:VZUG)

Simply Wall St Value Rating: ★★★★★★

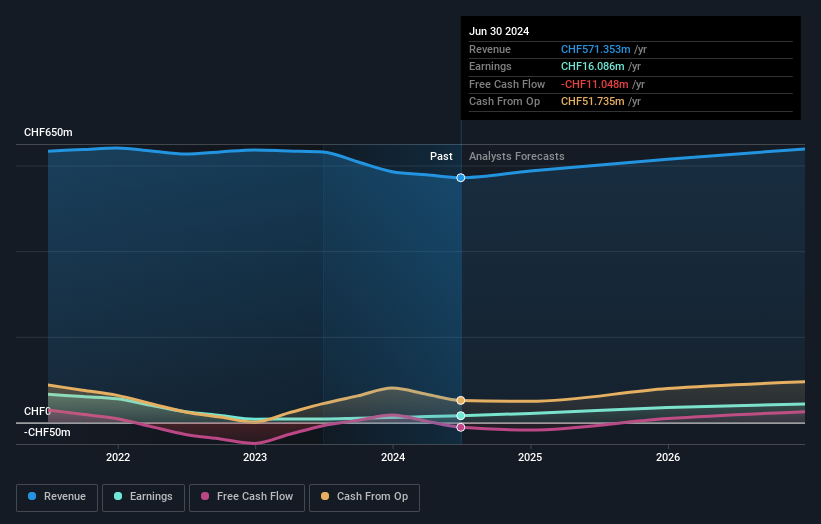

Overview: V-ZUG Holding AG is involved in the development, manufacture, marketing, sale, and servicing of kitchen and laundry appliances for private households both in Switzerland and internationally with a market capitalization of CHF366.43 million.

Operations: V-ZUG generates revenue primarily from its Household Appliances segment, amounting to CHF571.35 million. The company's financial performance is influenced by its net profit margin trends over time.

V-ZUG, a notable player in Switzerland's consumer durables sector, has shown impressive earnings growth of 89.2% over the past year, outpacing the industry average of 0.6%. Despite a volatile share price recently, it trades at 81.3% below its estimated fair value and remains debt-free compared to five years ago when its debt-to-equity ratio was 22.4%. Recent earnings announcements highlighted net income rising to CHF 8.73 million from CHF 4.33 million last year, with basic EPS doubling to CHF 1.36 from CHF 0.67.

- Take a closer look at V-ZUG Holding's potential here in our health report.

Evaluate V-ZUG Holding's historical performance by accessing our past performance report.

Where To Now?

- Click here to access our complete index of 18 SIX Swiss Exchange Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com