Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalTop Growth Companies With High Insider Ownership On SIX Swiss Exchange October 2024

In the midst of a volatile period, the Swiss market experienced fluctuations with the SMI closing slightly down, reflecting broader uncertainties in investor sentiment. In such an environment, growth companies with high insider ownership can be appealing as they often signal strong confidence from those closest to the business and potential resilience amid market shifts.

Top 10 Growth Companies With High Insider Ownership In Switzerland

| Name | Insider Ownership | Earnings Growth |

| LEM Holding (SWX:LEHN) | 29.9% | 20.5% |

| Stadler Rail (SWX:SRAIL) | 14.5% | 24.1% |

| VAT Group (SWX:VACN) | 10.2% | 22.8% |

| Straumann Holding (SWX:STMN) | 32.7% | 21.7% |

| Addex Therapeutics (SWX:ADXN) | 19% | 33.3% |

| Swissquote Group Holding (SWX:SQN) | 11.4% | 12.6% |

| Temenos (SWX:TEMN) | 21.8% | 14.4% |

| Partners Group Holding (SWX:PGHN) | 17% | 14.2% |

| Hocn (SWX:HOCN) | 14.6% | 122.2% |

| Sensirion Holding (SWX:SENS) | 19.9% | 102.7% |

Below we spotlight a couple of our favorites from our exclusive screener.

Swissquote Group Holding (SWX:SQN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Swissquote Group Holding Ltd offers a range of online financial services to retail, affluent, and institutional investors globally, with a market cap of CHF4.54 billion.

Operations: The company's revenue is primarily derived from Securities Trading, which accounts for CHF488.98 million, and Leveraged Forex, contributing CHF93.28 million.

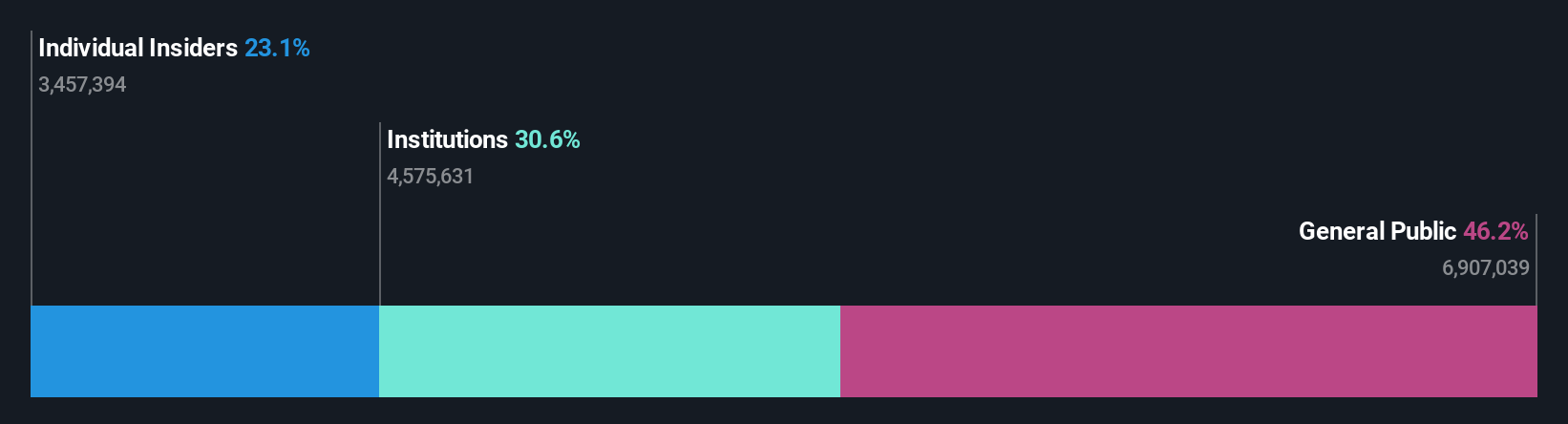

Insider Ownership: 11.4%

Earnings Growth Forecast: 12.6% p.a.

Swissquote Group Holding's recent earnings report shows a strong performance, with net income rising to CHF 144.56 million for the first half of 2024. Earnings per share also increased significantly. The company's forecasted earnings growth of 12.6% annually surpasses the Swiss market average, while revenue growth is expected at 11.1%, outpacing the market's 4.3%. Trading below estimated fair value, Swissquote presents potential value despite modest insider trading activity recently reported.

- Take a closer look at Swissquote Group Holding's potential here in our earnings growth report.

- According our valuation report, there's an indication that Swissquote Group Holding's share price might be on the cheaper side.

Temenos (SWX:TEMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Temenos AG develops, markets, and sells integrated banking software systems to financial institutions globally, with a market cap of CHF4.63 billion.

Operations: The company's revenue is divided into two segments: Product, generating $879.99 million, and Services, contributing $132.98 million.

Insider Ownership: 21.8%

Earnings Growth Forecast: 14.4% p.a.

Temenos is positioned for growth with earnings forecasted to rise 14.4% annually, surpassing the Swiss market's average. Despite trading 25.7% below its estimated fair value, it carries a high debt level. Recent executive changes aim to leverage AI and SaaS opportunities, potentially boosting operational efficiency and global reach. The company completed a CHF 200 million share buyback, enhancing shareholder value without substantial insider trading activity in the past three months.

- Unlock comprehensive insights into our analysis of Temenos stock in this growth report.

- The analysis detailed in our Temenos valuation report hints at an deflated share price compared to its estimated value.

V-ZUG Holding (SWX:VZUG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: V-ZUG Holding AG is involved in the development, manufacture, marketing, sale, and servicing of kitchen and laundry appliances for private households both in Switzerland and internationally, with a market cap of CHF366.43 million.

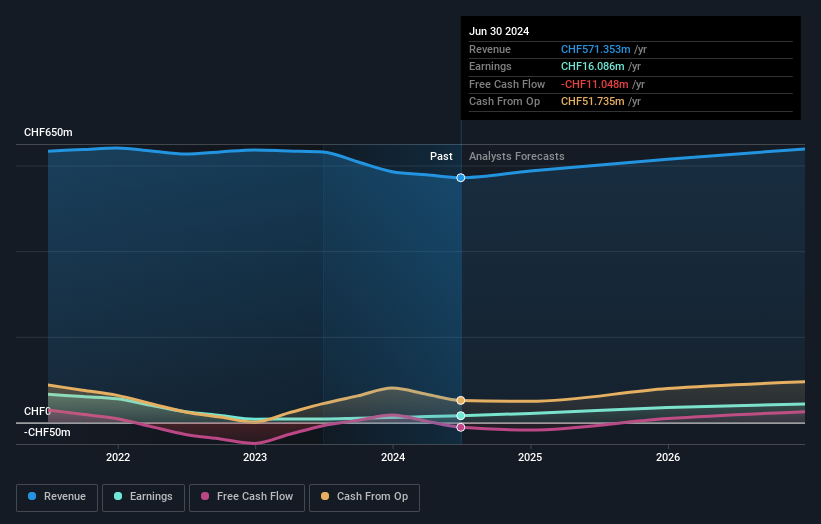

Operations: The company's revenue segment is primarily composed of Household Appliances, generating CHF571.35 million.

Insider Ownership: 20.9%

Earnings Growth Forecast: 38.7% p.a.

V-ZUG Holding is positioned for significant growth, with earnings projected to increase by 38.7% annually, outpacing the Swiss market's average. The stock trades at a substantial discount to its estimated fair value, although it has experienced high volatility recently. Despite no recent insider trading activity, V-ZUG reported improved net income of CHF 8.73 million for the first half of 2024 compared to CHF 4.33 million a year earlier, indicating robust financial performance amidst fluctuating sales figures.

- Delve into the full analysis future growth report here for a deeper understanding of V-ZUG Holding.

- Our valuation report here indicates V-ZUG Holding may be undervalued.

Seize The Opportunity

- Click this link to deep-dive into the 14 companies within our Fast Growing SIX Swiss Exchange Companies With High Insider Ownership screener.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com