Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalA Piece Of The Puzzle Missing From Jiangxi Wannianqing Cement Co., Ltd.'s (SZSE:000789) 36% Share Price Climb

Jiangxi Wannianqing Cement Co., Ltd. (SZSE:000789) shares have had a really impressive month, gaining 36% after a shaky period beforehand. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 25% in the last twelve months.

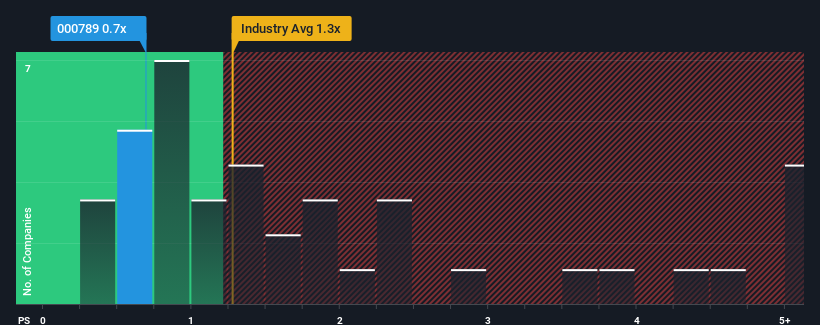

In spite of the firm bounce in price, given about half the companies operating in China's Basic Materials industry have price-to-sales ratios (or "P/S") above 1.3x, you may still consider Jiangxi Wannianqing Cement as an attractive investment with its 0.7x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

See our latest analysis for Jiangxi Wannianqing Cement

How Has Jiangxi Wannianqing Cement Performed Recently?

With revenue that's retreating more than the industry's average of late, Jiangxi Wannianqing Cement has been very sluggish. Perhaps the market isn't expecting future revenue performance to improve, which has kept the P/S suppressed. You'd much rather the company improve its revenue performance if you still believe in the business. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Jiangxi Wannianqing Cement will help you uncover what's on the horizon.How Is Jiangxi Wannianqing Cement's Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Jiangxi Wannianqing Cement's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 30% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 49% in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the three analysts covering the company suggest revenue should grow by 12% over the next year. That's shaping up to be materially higher than the 7.5% growth forecast for the broader industry.

With this information, we find it odd that Jiangxi Wannianqing Cement is trading at a P/S lower than the industry. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On Jiangxi Wannianqing Cement's P/S

Despite Jiangxi Wannianqing Cement's share price climbing recently, its P/S still lags most other companies. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Jiangxi Wannianqing Cement's analyst forecasts revealed that its superior revenue outlook isn't contributing to its P/S anywhere near as much as we would have predicted. When we see strong growth forecasts like this, we can only assume potential risks are what might be placing significant pressure on the P/S ratio. It appears the market could be anticipating revenue instability, because these conditions should normally provide a boost to the share price.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Jiangxi Wannianqing Cement you should know about.

If you're unsure about the strength of Jiangxi Wannianqing Cement's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.