Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalEven With A 30% Surge, Cautious Investors Are Not Rewarding Best Pacific International Holdings Limited's (HKG:2111) Performance Completely

Best Pacific International Holdings Limited (HKG:2111) shareholders would be excited to see that the share price has had a great month, posting a 30% gain and recovering from prior weakness. The annual gain comes to 166% following the latest surge, making investors sit up and take notice.

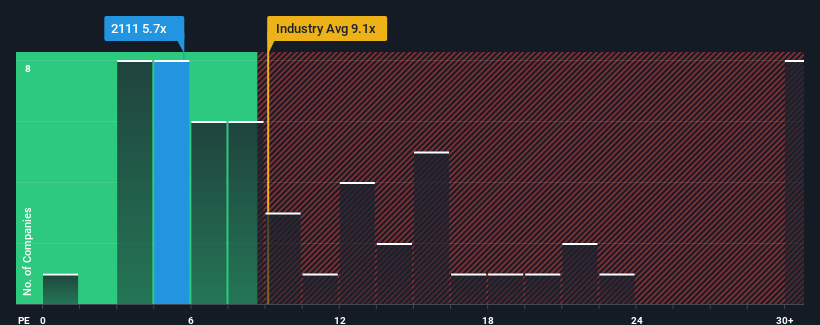

In spite of the firm bounce in price, given about half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") above 10x, you may still consider Best Pacific International Holdings as an attractive investment with its 5.8x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times have been advantageous for Best Pacific International Holdings as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Best Pacific International Holdings

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Best Pacific International Holdings' is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered an exceptional 80% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 40% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 17% each year as estimated by the dual analysts watching the company. With the market only predicted to deliver 13% per annum, the company is positioned for a stronger earnings result.

In light of this, it's peculiar that Best Pacific International Holdings' P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On Best Pacific International Holdings' P/E

Despite Best Pacific International Holdings' shares building up a head of steam, its P/E still lags most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Best Pacific International Holdings currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. There could be some major unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

And what about other risks? Every company has them, and we've spotted 1 warning sign for Best Pacific International Holdings you should know about.

If you're unsure about the strength of Best Pacific International Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.