Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalTop Chinese Dividend Stocks To Consider In October 2024

As Chinese equities faced a challenging week with declines in major indices like the Shanghai Composite and CSI 300, investor sentiment has been cautious amid waning optimism about Beijing's stimulus measures. Against this backdrop, dividend stocks can offer stability and income potential, making them an attractive option for those looking to navigate uncertain market conditions.

Top 10 Dividend Stocks In China

| Name | Dividend Yield | Dividend Rating |

| Midea Group (SZSE:000333) | 3.99% | ★★★★★★ |

| Kweichow Moutai (SHSE:600519) | 3.28% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 4.14% | ★★★★★★ |

| Changhong Meiling (SZSE:000521) | 3.33% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 3.30% | ★★★★★★ |

| Inner Mongolia Yili Industrial Group (SHSE:600887) | 4.59% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.50% | ★★★★★★ |

| Chacha Food Company (SZSE:002557) | 3.35% | ★★★★★★ |

| Huangshan NovelLtd (SZSE:002014) | 5.66% | ★★★★★★ |

| Zhejiang Jiaxin SilkLtd (SZSE:002404) | 5.11% | ★★★★★★ |

Click here to see the full list of 204 stocks from our Top Chinese Dividend Stocks screener.

We're going to check out a few of the best picks from our screener tool.

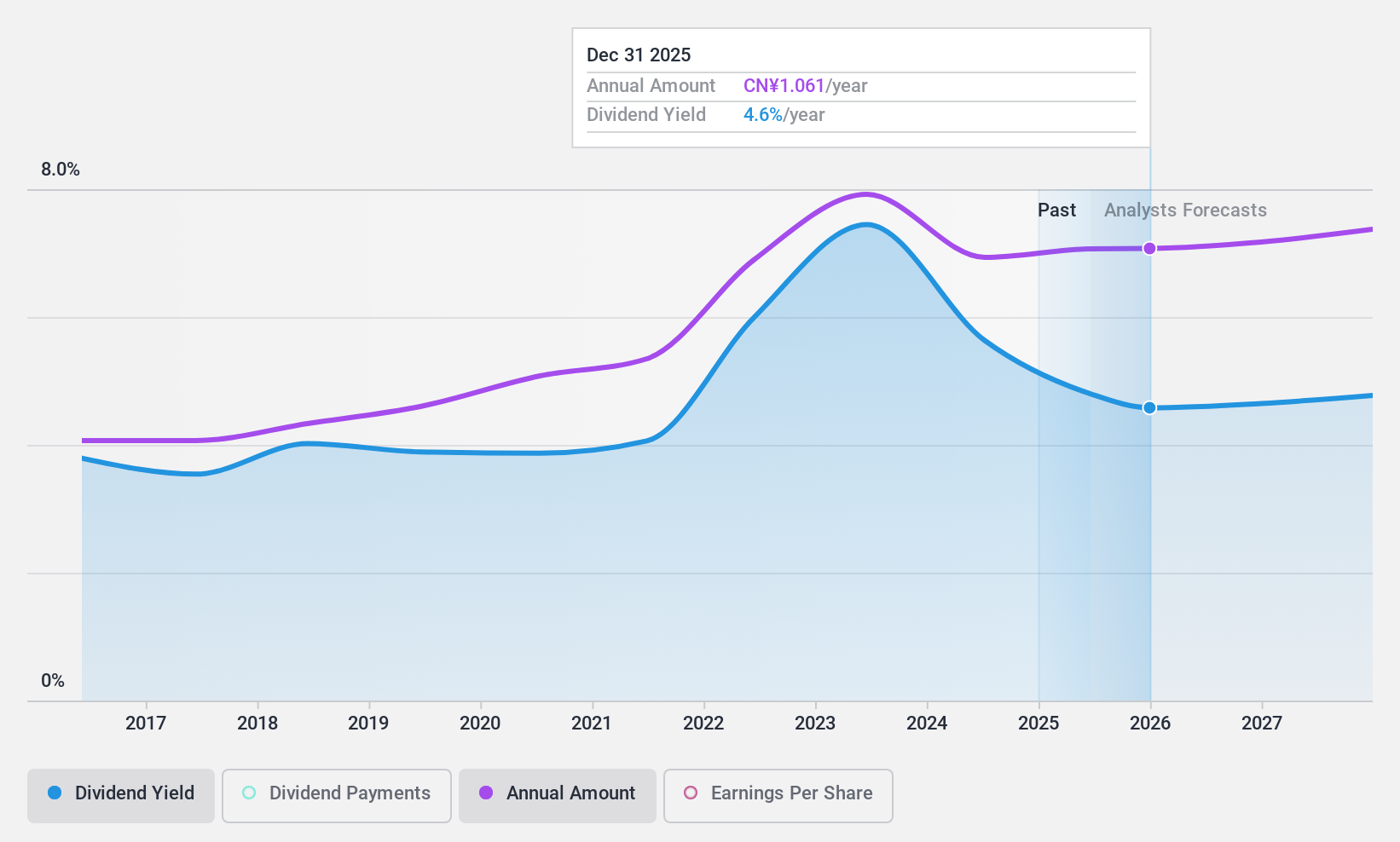

Industrial Bank (SHSE:601166)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Industrial Bank Co., Ltd. offers banking services in the People’s Republic of China with a market cap of CN¥414.66 billion.

Operations: Industrial Bank Co., Ltd. generates revenue from its Commercial Bank segment amounting to CN¥148 billion.

Dividend Yield: 5.2%

Industrial Bank's dividend payments have increased over the past decade, supported by a low payout ratio of 29.5%, indicating strong earnings coverage. Despite trading at 60.6% below estimated fair value, its dividends have been volatile and unreliable historically. The current yield of 5.21% ranks in the top quarter of Chinese dividend payers, though sustainability concerns persist due to an unstable track record despite consistent earnings growth forecasts and recent stable financial performance with net income at ¥43 billion for H1 2024.

- Click here and access our complete dividend analysis report to understand the dynamics of Industrial Bank.

- Our comprehensive valuation report raises the possibility that Industrial Bank is priced lower than what may be justified by its financials.

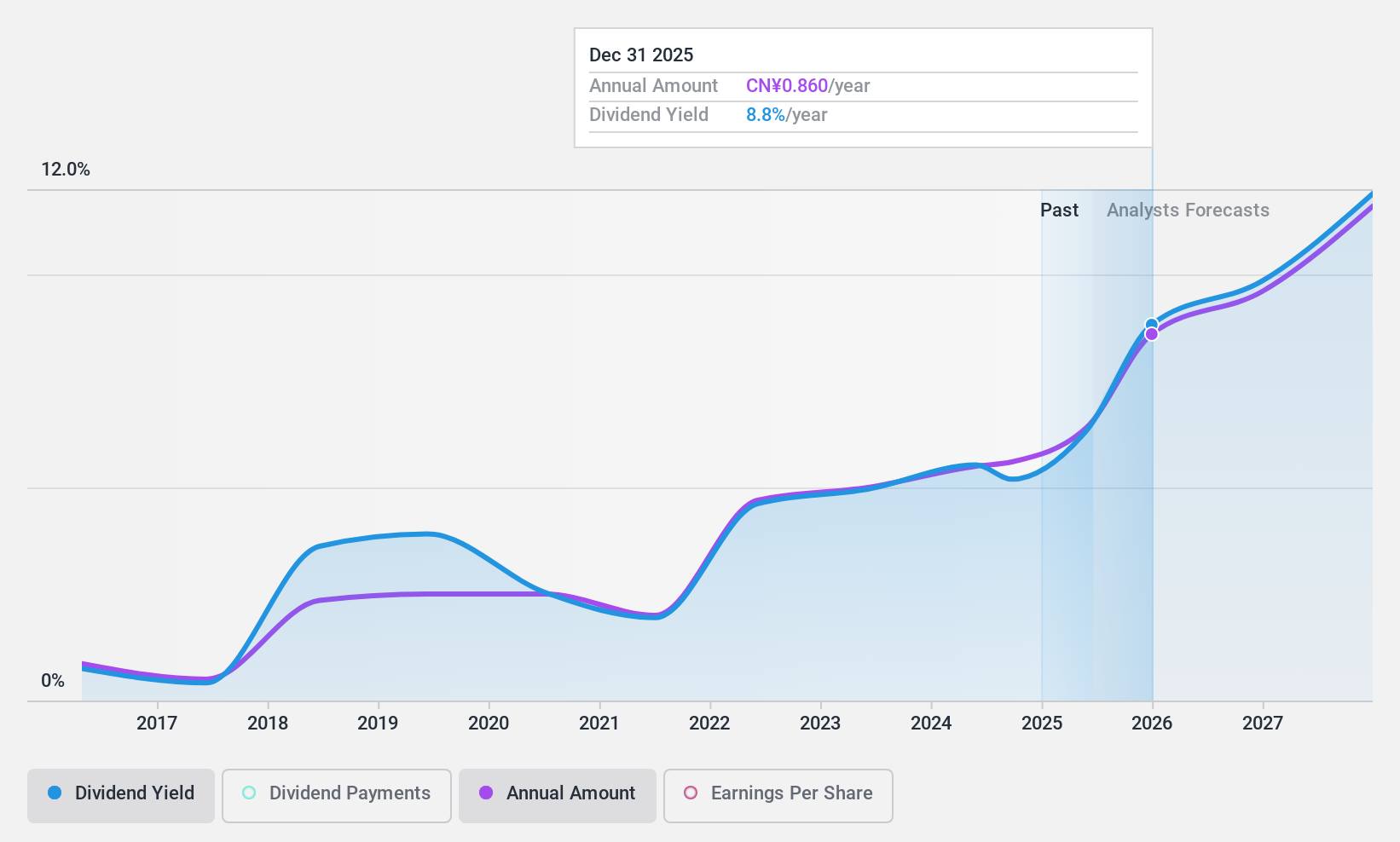

DeHua TB New Decoration MaterialLtd (SZSE:002043)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: DeHua TB New Decoration Material Co., Ltd specializes in the production and sale of environmentally friendly furniture panels both in China and internationally, with a market cap of CN¥9.76 billion.

Operations: DeHua TB New Decoration Material Co., Ltd's revenue is primarily derived from its Decorative Material Business, which accounts for CN¥7.59 billion, followed by the Custom Home Business at CN¥2.04 billion.

Dividend Yield: 4.7%

DeHua TB New Decoration Material Ltd's dividend yield of 4.71% is among the top 25% in China, but its sustainability is questionable due to a high payout ratio of 100.9%, indicating dividends are not well covered by earnings. Despite volatile and unreliable past dividend payments, they have increased over the last decade. Recent financials show revenue growth to ¥3.91 billion for H1 2024, although net income decreased to ¥244.13 million from the previous year.

- Dive into the specifics of DeHua TB New Decoration MaterialLtd here with our thorough dividend report.

- In light of our recent valuation report, it seems possible that DeHua TB New Decoration MaterialLtd is trading behind its estimated value.

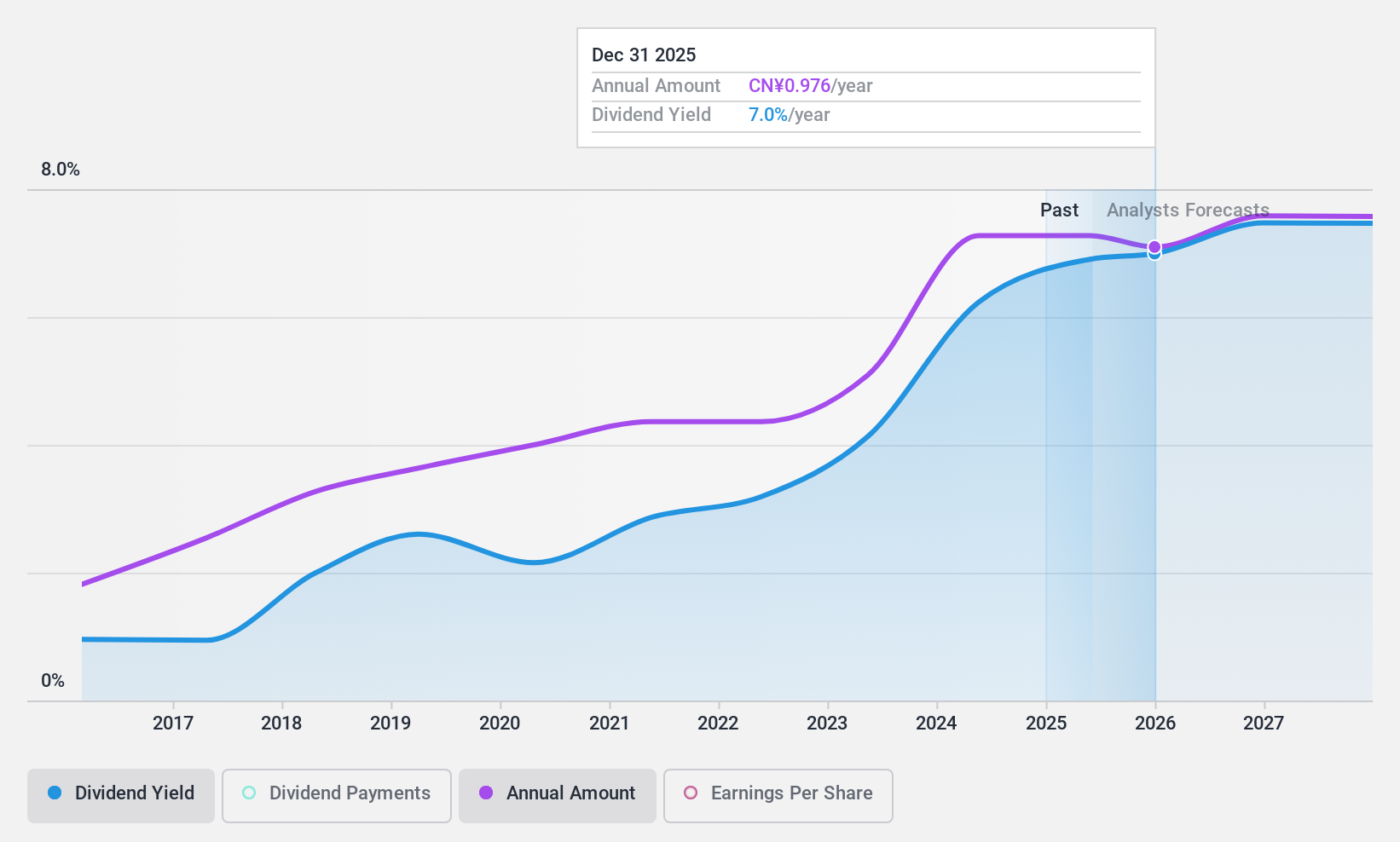

Suofeiya Home Collection (SZSE:002572)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Suofeiya Home Collection Co., Ltd. operates in the research, development, manufacturing, and sale of furniture products in China with a market cap of CN¥16.91 billion.

Operations: Suofeiya Home Collection Co., Ltd.'s revenue from furniture manufacturing is CN¥11.84 billion.

Dividend Yield: 5.7%

Suofeiya Home Collection offers a dividend yield of 5.69%, placing it in the top 25% of Chinese dividend payers, though sustainability is a concern as dividends are not well covered by free cash flow, with a high cash payout ratio of 416.9%. Despite this, dividends have been stable and growing over the past decade. Recent earnings show improved performance with net income rising to ¥564.6 million for H1 2024 from ¥499.62 million previously.

- Click to explore a detailed breakdown of our findings in Suofeiya Home Collection's dividend report.

- The valuation report we've compiled suggests that Suofeiya Home Collection's current price could be quite moderate.

Summing It All Up

- Get an in-depth perspective on all 204 Top Chinese Dividend Stocks by using our screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com