Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 Growth Companies On SIX Swiss Exchange With 51% Return On Equity

The Swiss market has shown resilience, with a 1.4% increase over the past week and an impressive 11% rise in the last year, while earnings are projected to grow by 12% annually. In this favorable environment, stocks of growth companies with high insider ownership can be particularly appealing as they often indicate strong internal confidence and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In Switzerland

| Name | Insider Ownership | Earnings Growth |

| LEM Holding (SWX:LEHN) | 29.9% | 20.5% |

| Stadler Rail (SWX:SRAIL) | 14.5% | 24.1% |

| VAT Group (SWX:VACN) | 10.2% | 22.4% |

| Addex Therapeutics (SWX:ADXN) | 19% | 33.3% |

| Straumann Holding (SWX:STMN) | 32.7% | 21.7% |

| Swissquote Group Holding (SWX:SQN) | 11.4% | 12.6% |

| Temenos (SWX:TEMN) | 21.8% | 14.4% |

| Gurit Holding (SWX:GURN) | 30.2% | 76.1% |

| Hocn (SWX:HOCN) | 14.6% | 122.2% |

| Sensirion Holding (SWX:SENS) | 19.9% | 102.7% |

Let's explore several standout options from the results in the screener.

Partners Group Holding (SWX:PGHN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Partners Group Holding AG is a private equity firm that specializes in direct, secondary, and primary investments across private equity, real estate, infrastructure, and debt with a market cap of CHF33.72 billion.

Operations: The company's revenue segments include CHF1.19 billion from Private Equity, CHF254.90 million from Infrastructure, CHF218.90 million from Private Credit, and CHF190.90 million from Real Estate.

Insider Ownership: 17%

Return On Equity Forecast: 51% (2027 estimate)

Partners Group Holding AG, with high insider ownership, is poised for growth despite mixed financial signals. Forecasts indicate a 15.4% annual revenue increase and a 14.2% earnings rise, outpacing the Swiss market. However, its dividend yield of 3.06% isn't well-covered by earnings or free cash flow. Recent M&A activity highlights Partners Group's interest in strategic acquisitions like I-MED Radiology and Lighthouse Learnings, potentially enhancing its growth trajectory amidst high debt levels.

- Delve into the full analysis future growth report here for a deeper understanding of Partners Group Holding.

- Insights from our recent valuation report point to the potential overvaluation of Partners Group Holding shares in the market.

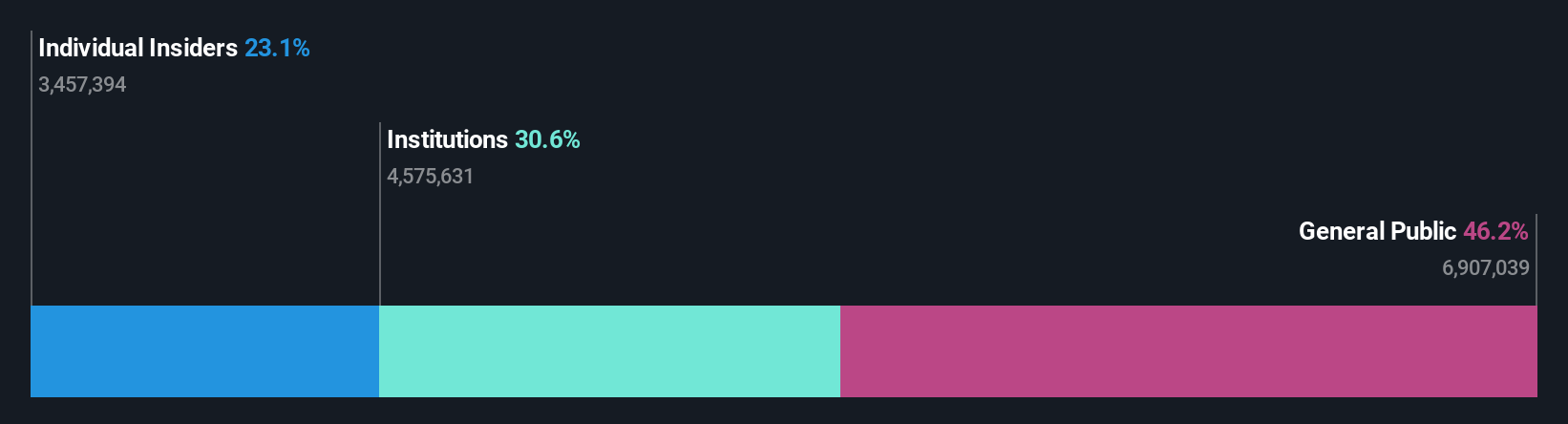

Swissquote Group Holding (SWX:SQN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Swissquote Group Holding Ltd offers a comprehensive range of online financial services to retail, affluent, and professional institutional investors globally, with a market cap of CHF4.56 billion.

Operations: The company generates revenue through leveraged forex, amounting to CHF93.28 million, and securities trading, which brings in CHF488.98 million.

Insider Ownership: 11.4%

Return On Equity Forecast: 26% (2027 estimate)

Swissquote Group Holding has demonstrated strong financial performance with a net income of CHF 144.56 million for the first half of 2024, up from CHF 106.53 million the previous year. Its earnings per share also increased significantly, indicating robust growth prospects. The company's revenue is forecast to grow at 11.1% annually, exceeding market expectations, while its earnings are projected to rise by 12.64% per year, reflecting solid growth potential despite being below significant levels.

- Navigate through the intricacies of Swissquote Group Holding with our comprehensive analyst estimates report here.

- Upon reviewing our latest valuation report, Swissquote Group Holding's share price might be too pessimistic.

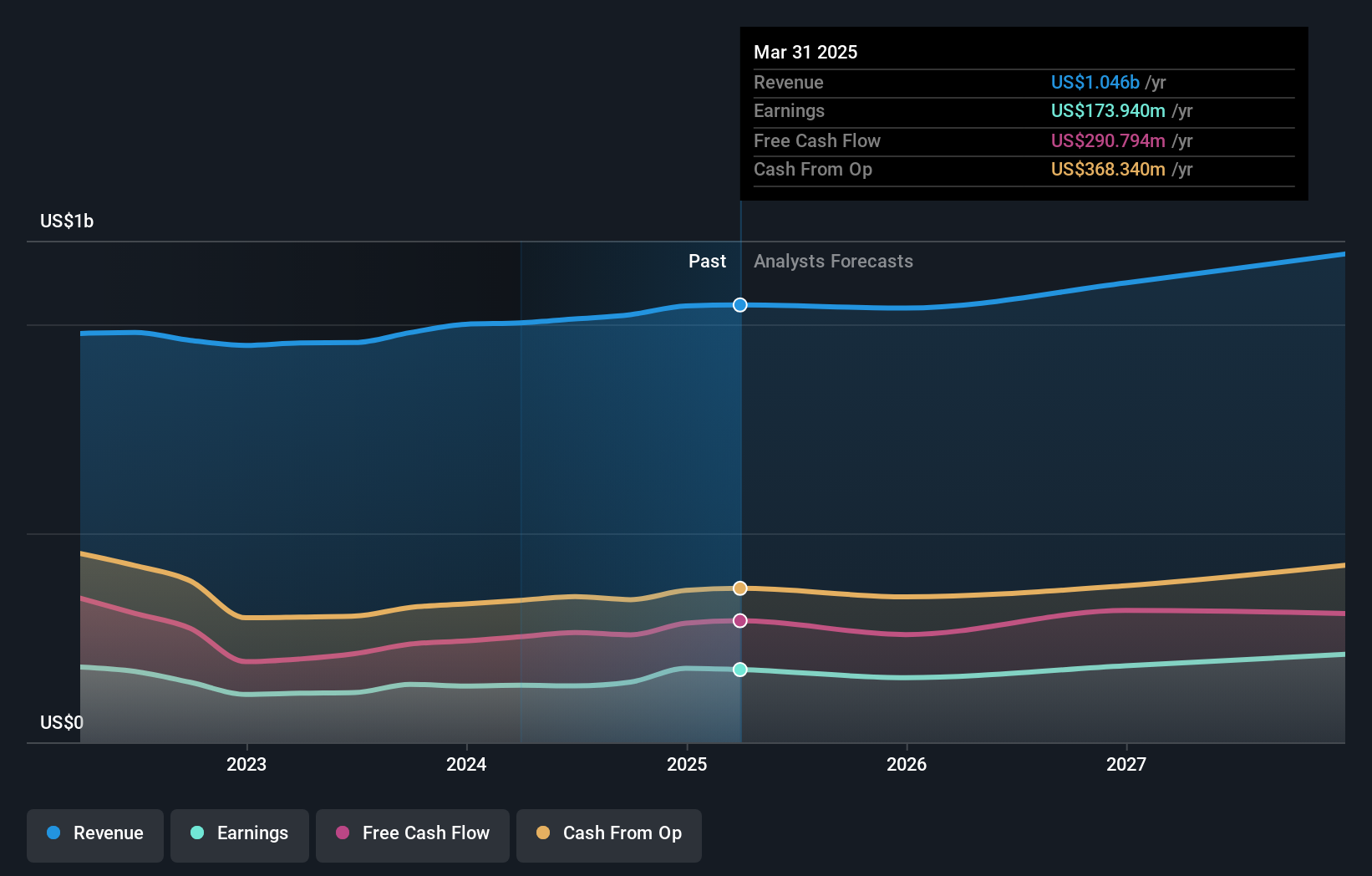

Temenos (SWX:TEMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Temenos AG develops, markets, and sells integrated banking software systems to banking and other financial institutions worldwide, with a market cap of CHF4.65 billion.

Operations: The company's revenue is derived from two main segments: Product, contributing $879.99 million, and Services, generating $132.98 million.

Insider Ownership: 21.8%

Return On Equity Forecast: 25% (2027 estimate)

Temenos has shown promising growth potential, with earnings forecast to rise by 14.4% annually, surpassing the Swiss market's average. Recent executive appointments aim to enhance its SaaS and US market presence, potentially driving further expansion. Despite a high level of debt, Temenos' return on equity is projected to reach 24.8% in three years. The company completed a CHF 200 million share buyback program and is considering selling its fund management unit for EUR 600 million.

- Click here to discover the nuances of Temenos with our detailed analytical future growth report.

- According our valuation report, there's an indication that Temenos' share price might be on the expensive side.

Make It Happen

- Navigate through the entire inventory of 14 Fast Growing SIX Swiss Exchange Companies With High Insider Ownership here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com