Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalDiscovering Hidden Gems in Germany This October 2024

As the German economy faces a forecasted contraction for the second consecutive year, with factory orders experiencing a significant decline, investor interest in small-cap stocks remains piqued by hopes of potential European Central Bank rate cuts. In this challenging environment, identifying promising stocks often involves looking beyond immediate economic indicators to find companies with robust fundamentals and innovative strategies poised to navigate and capitalize on market uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals In Germany

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Mineralbrunnen Überkingen-Teinach GmbH KGaA | 19.91% | 0.96% | -5.02% | ★★★★★★ |

| Westag | NA | -1.56% | -21.68% | ★★★★★★ |

| FRoSTA | 8.18% | 4.36% | 16.00% | ★★★★★★ |

| Mühlbauer Holding | NA | 10.49% | -12.73% | ★★★★★★ |

| Südwestdeutsche Salzwerke | 0.30% | 4.57% | 25.01% | ★★★★★☆ |

| EnviTec Biogas | 48.48% | 20.85% | 46.34% | ★★★★★☆ |

| HOMAG Group | NA | -31.14% | 23.43% | ★★★★★☆ |

| Baader Bank | 91.28% | 12.42% | -8.00% | ★★★★★☆ |

| DFV Deutsche Familienversicherung | NA | 19.63% | 62.92% | ★★★★★☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

Paul Hartmann (DB:PHH2)

Simply Wall St Value Rating: ★★★★★☆

Overview: Paul Hartmann AG is a global manufacturer and seller of medical and care products, operating across Germany, the rest of Europe, the Middle East, Africa, Asia-Pacific, and the Americas with a market cap of approximately €749.42 million.

Operations: Key revenue streams for Paul Hartmann AG include Incontinence Management (€769.70 million), Wound Care (€597.39 million), Infection Management (€516.66 million), and Complementary divisions of the group (€499.70 million).

With a robust earnings growth of 156.1% over the past year, Paul Hartmann outpaced its industry peers significantly. The company's net income for the half-year rose to €42.8 million from €11.69 million, while basic earnings per share jumped to €12.05 from €3.29 last year, underscoring strong operational performance. Despite an increased debt-to-equity ratio of 26.3% over five years, its interest payments are well covered by EBIT at 6.2x, reflecting sound financial health and potential for sustained profitability in the medical equipment sector.

MLP (XTRA:MLP)

Simply Wall St Value Rating: ★★★★★★

Overview: MLP SE, with a market cap of €686.39 million, offers financial services to private, corporate, and institutional clients in Germany through its various subsidiaries.

Operations: MLP SE generates revenue primarily from Financial Consulting (€429.61 million), FERI (€231.23 million), and Banking (€206.97 million) segments, among others. The company also incurs a consolidation adjustment of -€86.32 million in its financial reporting.

MLP, a nimble player in the financial sector, is debt-free and boasts high-quality earnings. Its recent performance reveals impressive growth, with earnings rising 28.4% over the past year, outpacing industry averages. Trading at 39.4% below estimated fair value suggests potential upside for investors. The company raised its EBIT forecast for 2024 to between €85 million and €95 million due to stronger-than-expected third-quarter results, highlighting robust operational momentum and strategic positioning within its market niche.

- Click here and access our complete health analysis report to understand the dynamics of MLP.

Evaluate MLP's historical performance by accessing our past performance report.

Friedrich Vorwerk Group (XTRA:VH2)

Simply Wall St Value Rating: ★★★★★☆

Overview: Friedrich Vorwerk Group SE offers solutions for the transformation and transportation of energy across Germany and Europe, with a market capitalization of €520 million.

Operations: The company generates revenue primarily through its segments in natural gas (€160.89 million), electricity (€95.30 million), clean hydrogen (€28.38 million), and adjacent opportunities (€117.28 million).

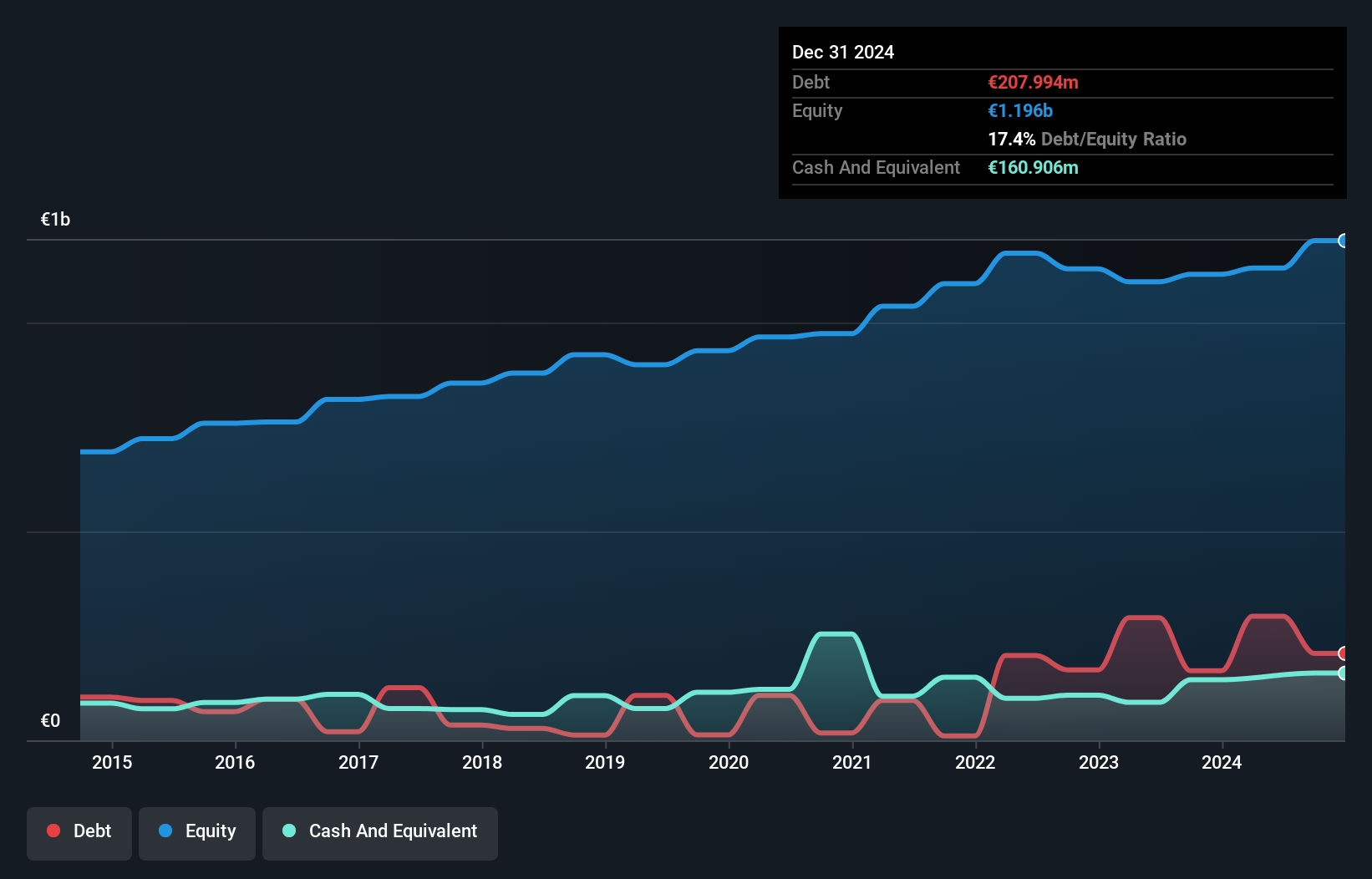

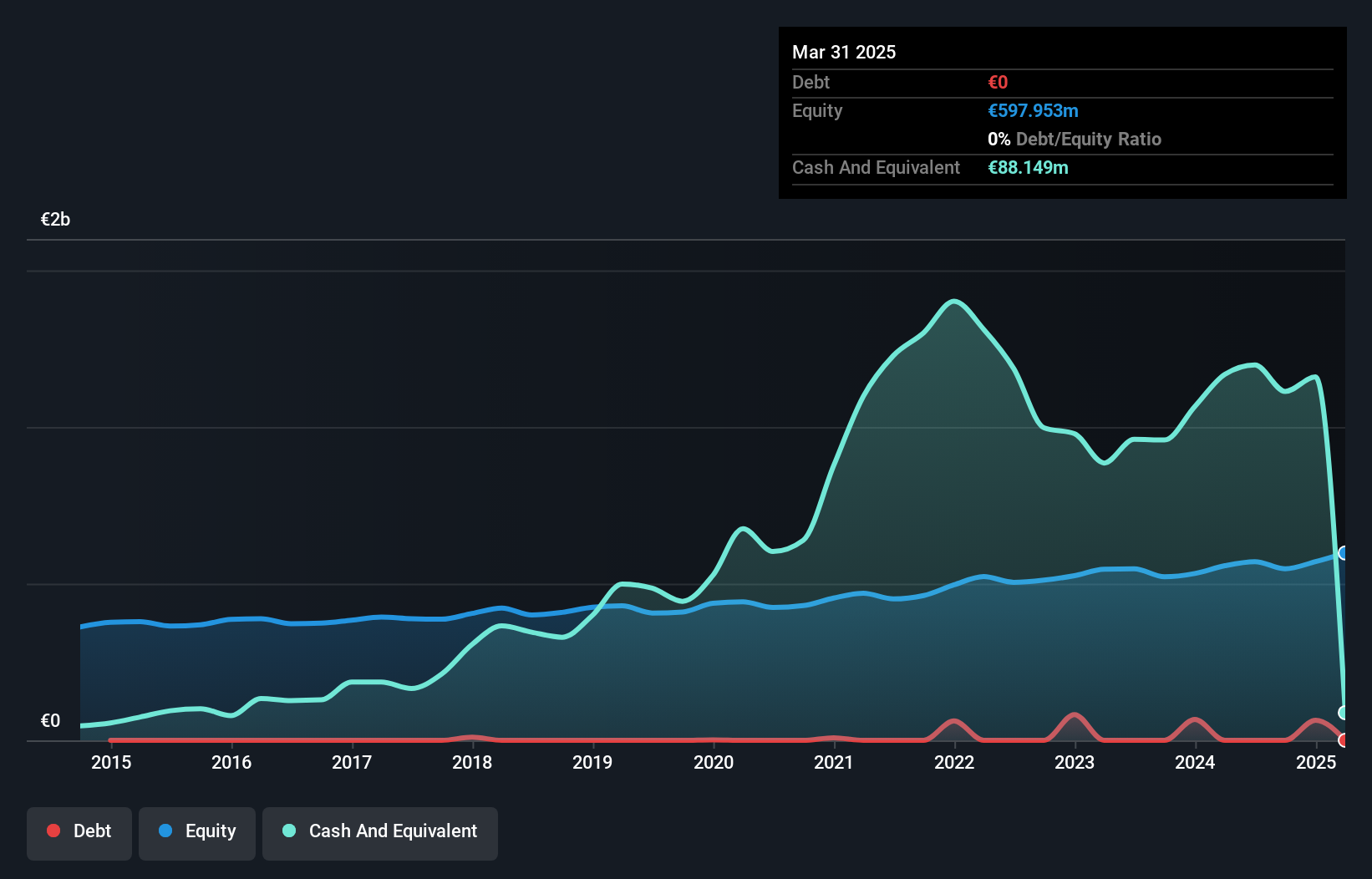

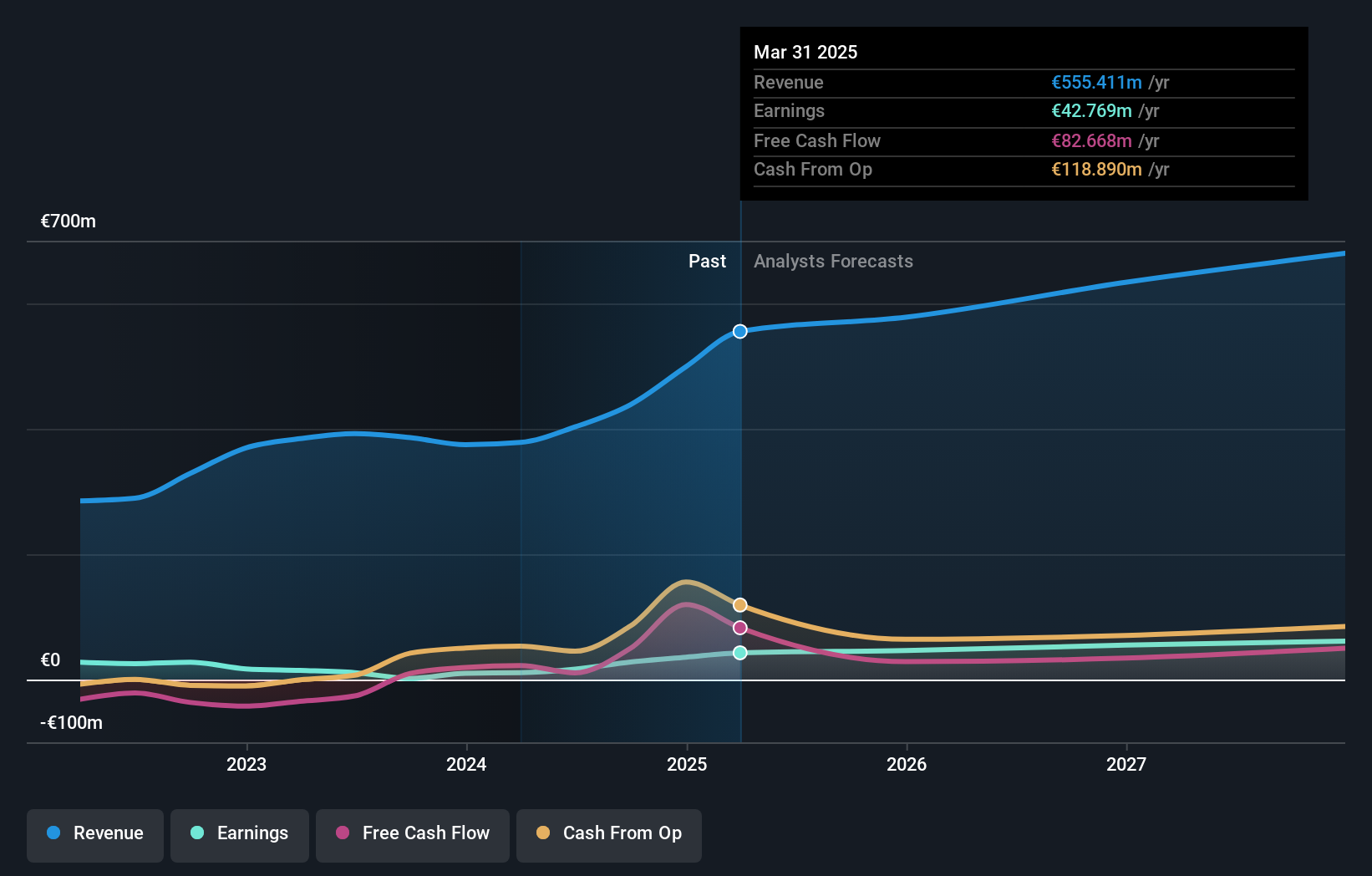

Friedrich Vorwerk Group, a promising player in Germany's market, saw significant growth with earnings jumping 48.6% over the past year, outpacing the Oil and Gas industry. The firm's net income for Q2 2024 was €7.96 million, up from €2.38 million the previous year, while revenue hit €121.04 million compared to last year's €96.41 million. With a satisfactory net debt to equity ratio of 12%, and earnings per share increasing to €0.4 from €0.12, Vorwerk seems well-positioned for future expansion with projected revenue growth of at least 10% in 2024.

- Unlock comprehensive insights into our analysis of Friedrich Vorwerk Group stock in this health report.

Gain insights into Friedrich Vorwerk Group's past trends and performance with our Past report.

Next Steps

- Click here to access our complete index of 55 German Undiscovered Gems With Strong Fundamentals.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com